Finpension Invest vs VIAC Invest 2026

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Both Finpension Invest and VIAC Invest are relatively new robo-advisors. Both services come from successful companies providing retirement accounts. They are both interesting services, but how do they compare?

In this highly requested article, we compare Finpension Invest vs VIAC Invest in depth, with their features and their fees. By the end of this comparison article, you will know which robo-advisor you should use.

|

Best Robo-advisor

|

|

|

5.0

|

4.0

|

Finpension Invest

Finpension is a great innovative company in Switzerland. They have started with a 1e product and from there developed other great products: a vested benefits account and a third pillar.

In May 2024, Finpension Invest launched their robo-advisor service, Finpension Invest. For this, they got approved as a securities firm by FINMA, so they hold the securities themselves.

You can use Finpension Invest on your computer or on your mobile phone. At this point, Finpension Invest is only offered to Swiss residents.

If you would like to learn more, you can read our Finpension Invest Review.

VIAC Invest

In 2018, VIAC started a new wave of changes for third pillars in Switzerland. Before them, the fees were high, the returns were low, and the customization was limited. VIAC changed all that when they introduced their third pillar. They then built on their success by launching a vested benefits account as well.

And then in late 2024, VIAC started their robo-advisor service, named VIAC Invest. This launch was only a few months after Finpension Invest was launched.

VIAC and all their services are available on mobile and web. VIAC Invest is only available to Swiss residents.

If you wish to learn more, you can read our VIAC Invest review.

With that out of the way, we can start our in-depth comparison of Finpension Invest vs VIAC Invest.

Investing Strategy

First, we should look at the investing strategy of Finpension Invest vs VIAC Invest.

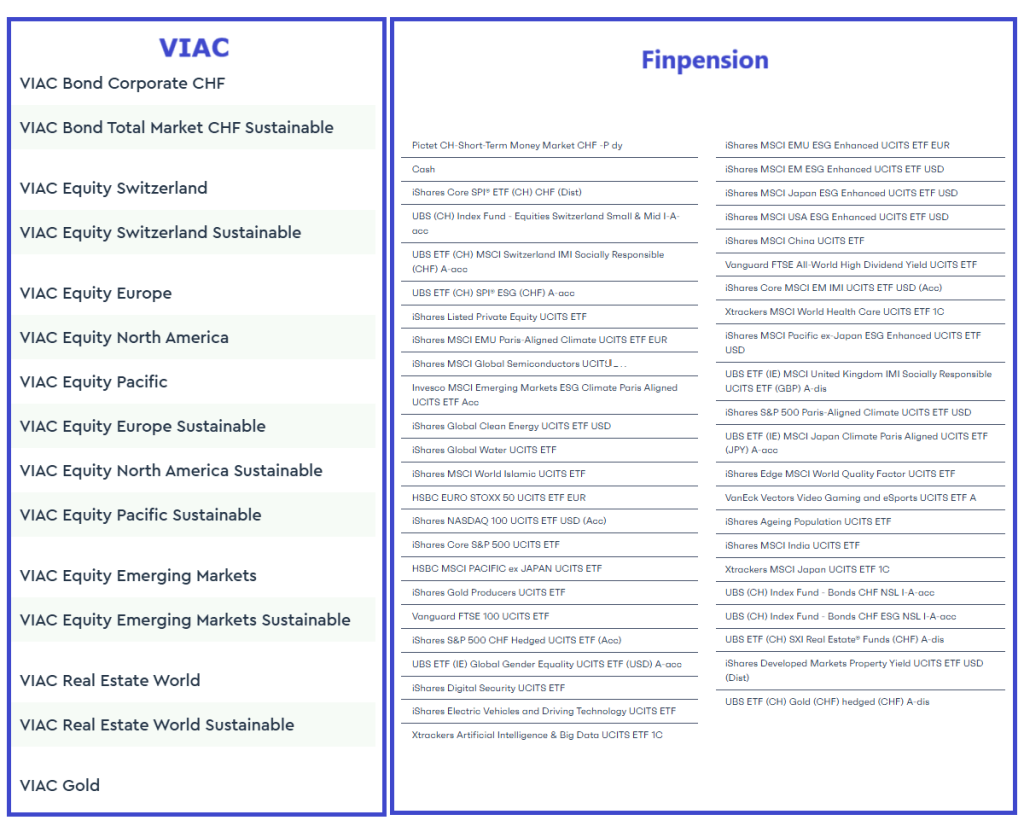

Finpension Invest uses Exchange Traded Funds (ETFs) for stocks and index funds for bonds. They only use index ETFs, which is great. You can invest up to 99% in stocks. On the other hand, you can also be very conservative and hold 99% in a money market fund.

Finpension Invest lets you choose between Global, Switzerland, and Sustainable universes, which is very common. You can also decide to invest in Europe or in a specific sustainable impact like Climate Impact. And you can do your own custom portfolio by picking directly among all the 45 available ETFs. You can hold up to 10 different portfolios, each with its own strategy. And finally, you can also invest in private markets through two institutional funds.

Interestingly, VIAC Invest has a different strategy. They are using their index funds. These are VIAC funds that are only available through VIAC Invest. And these funds are funds of funds, meaning they do not hold stocks or bonds directly but instead hold funds from other providers (like UBS). You can invest up to 99% in stocks at most. And you can hold up to 99% in cash or bonds if you want to be conservative. For the part not invested in stocks, you can decide between bonds or cash.

You can pick within the standard Global, Switzerland, and Sustainable universes as well. You can also do a custom portfolio by selecting between the 15 VIAC funds. This is more limited than in some places because you cannot pick the sub-funds, only the VIAC funds.

When comparing Finpension Invest vs VIAC Invest, we conclude that both investing strategies are great. I would expect both strategies to yield the same results. If you want to invest in private markets, Finpension Invest has an advantage. But if you prefer to hold cash (and not money market funds), VIAC Invest has an advantage. And finally, if you would like to create custom portfolios, Finpension Invest is much more flexible.

Fees

If two services have comparable investing strategies, their fees are what will differentiate them in terms of total returns. Indeed, if they have about the same performance, the cheaper service will result in higher returns. So, we must now compare Finpension Invest vs VIAC Invest in terms of fees.

Finpension Invest has two components in its total fee. They have a 0.30% custody fee and a 0.09% wealth management fee. We also must pay the TER of the funds, with an average yearly fee of 0.10%. This gives us a total fee of 0.49% per year.

VIAC Invest has a 0.25% administration fee. Additionally, you must pay for the funds themselves. On average, the funds from VIAC Invest will cost 0.24%, giving us a total of 0.49%.

As far as recurring fees go, both services have the same fee of 0.49%. Recurring fees are essential because you will pay them every year on everything that has been invested.

However, we must also look at one-time fees. These are the fees that happen when some money is invested into the robo-advisor.

Finpension Invest is using ETFs, so they charge Swiss stamp duty on each transaction (buy and sell). The transaction costs themselves are included in the recurring fees. And since they are trading ETFs, there will be some market spread (premium we pay compared to the market price). On the other hand, there are no issuance or redemption fees with ETFs. And the currency conversion fee is already included.

VIAC Invest already includes stamp duty in its yearly fee, as well as the currency conversion fees and the transaction costs. Since they are using funds, there is no spread. However, these funds have issuance and redemption fees. These fees depend on your portfolio because they are different for each fund (and each sub-fund). For the default portfolio with 100% stocks, we get an average 0.07% purchase fee and a 0.14% sale fee.

Overall, the one-time fees of both services are very similar. If you use a portfolio with low issuance and redemption fees, VIAC Invest may be slightly cheaper. But if you use a portfolio with high fees, Finpension Invest may be slightly cheaper.

So, overall, we can say that Finpension Invest and VIAC Invest have the same fees.

Tax efficiency

Tax efficiency is often overlooked because it is not a direct fee. But when we deal with optimized robo-advisors, it is essential to look into this. Indeed, the returns lost to unreclaimable withheld dividends can be very significant. Therefore, we must compare Finpension Invest vs VIAC Invest on tax efficiency.

Finpension Invest uses ETFs from Ireland, and Ireland has a tax treaty with the United States. As a result, they apply a tax withholding of 15% (reduced from a default of 30%) to dividends from the United States (which are about 66% of the world’s stock exchange). This is equivalent to an annual fee of about 0.15% on your portfolio.

Additionally, Finpension is doing something unique. They have made a deal with BlackRock so that they can provide the necessary documentation to reclaim even this 15% on your tax declaration. Currently, this technique has only been approved by Lucerne, but other cantons may approve it. If you are in a canton that approves this, you can fill out a DA-1 and get back the withheld dividends (just like you would if you were using US ETFs). This optimization results in no fees lost to dividend withholding.

VIAC is quite different in this matter. They are using Swiss funds, meaning this will get a withholding rate of 30%. A small optimization is that this fund itself holds 20% of the assets in Ireland, resulting in 15% withholding. This results in an average of 27% withholding rate. And this rate is equivalent to a 0.26% annual fee.

As a result, Finpension Invest is much more tax efficient than VIAC Invest. By default, you would save 0.11% per year with Finpension Invest. And if you are in a canton where you can reclaim the DA-1 from Finpension Invest, you could even save 0.26% per year.

Security

It is essential to look at the security and safety of a robo-advisor before starting to invest. So, we will compare Finpension Invest vs VIAC Invest on these two subjects.

Both companies are now well-established. Finpension has been profitable since 2019. While we do not know the details, VIAC is expected to be in good financial shape and growing. Both of these companies are managing more than 3 billion CHF. It is currently unlikely that any of them will go bankrupt.

If Finpension were to go bankrupt, the shares would be safe since they are segregated from Finpension’s assets. Regulators would have to find another manager for these shares, and we would get them back. The same would happen for VIAC where segregation also happens. It could be slightly more complicated for VIAC since they use VIAC funds. But I expect no shares to be lost in either case. If the custody bank of VIAC (Regiobank) were to go bankrupt, VIAC itself would have to find another custody bank and would take care of transferring the assets. In all events, if we are to learn from the recent FlowBank bankruptcy, it could take a while to get back our shares.

From a technical security standpoint, neither of these companies has had any known security issues since their creation. They both offer a second factor of authentication. VIAC offers SMS 2FA while Finpension offers a superior TOTP 2FA. This is a small advantage for Finpension Invest.

Overall, I would say that both companies are quite safe. The only difference remains in how they handle 2FA.

Reputation

Finally, we can also look at the reputation of Finpension Invest vs VIAC Invest.

Both companies are very well established. Both are offering excellent services, and users are generally thrilled about what they are doing. From what I hear among my readers, I would say that both companies have an excellent reputation. It is interesting, though, that they are not viewed in the same way:

- VIAC is generally viewed as a friendly and young company with good results.

- Finpension is usually regarded as a more professional entity that deals with serious business.

Unfortunately, there are not many objective reviews online. From what we can find on the Play Store and on the Apple Store, both apps have excellent reviews. There are not enough reviews on Trustpilot to draw conclusions. And most VIAC reviews on Google are only there to share referral codes.

Overall, I would say that both companies have an excellent reputation. They are perceived slightly differently by the public but are trusted by their customers.

Summary

We can draw a table summary of our findings:

|

Best Robo-advisor

|

Good Robo-advisor

|

|

Primary Rating:

5.0

|

Primary Rating:

4.0

|

|

Pros:

|

Pros:

|

|

Cons:

|

Cons:

|

|

0.49% per year

|

0.49% per year

|

- Great investing strategy

- Great fees

- Good reputation

- Excellent dividend tax efficiency

- Access to private markets

- Very good customization

- Cannot invest in cash

- Great investing strategy

- Great fees

- Good reputation

- Not very efficient for dividend withholding

- Limited customization

We can draw a few conclusions regarding Finpension Invest vs VIAC Invest from this summary:

- Both services let you invest up to 99% in stocks

- Both services have the same general fees

- Finpension 3a is more optimized for dividend withholding

- VIAC lets you invest in cash or bonds, while Finpension Invest only has bonds and money market funds

- Finpension has much greater customization ability

Conclusion – Finpension Invest vs VIAC Invest

An excellent and innovative Robo-advisor by Finpension.

- Most tax-efficient Robo-advisor

- Access to private markets

Finpension Invest and VIAC Invest have a lot in common and appear to be two great robo-advisors. They both have a great investing strategy (although quite different), and they have similar fees. However, when we dig deeper, we can see that Finpension Invest has a very significant advantage over VIAC Invest. Finpension Invest is more optimized for US dividends, resulting in at least a 0.11% lower annual total fee (and possibly higher).

For me, this extra efficiency is enough to tip the balance in favor of Finpension Invest. This advantage makes Finpension Invest the best robo-advisor available in Switzerland.

For transparency, I must say that I invest with neither of these two services (although Finpension manages my third pillar). Instead, I invest directly in ETFs through a broker (DIY Investing). If you are ready to learn how to do it yourself, you can optimize your investing further. But if you are not, robo-advisors are the next best thing. And if I were to use a robo-advisor myself, I would use Finpension Invest.

What about you? What is your choice between Finpension Invest vs VIAC Invest?

More reading

Selma vs Inyova 2026 – Best robo-Advisor for Sustainable Investing?

Impact or Simplicity? We compare Selma and Inyova, two popular Swiss Robo-Advisors, to help you choose between ease of use and sustainable investing.

Swissquote Invest Easy Review 2026 – Pros & Cons

Swissquote started a new Robo-advisor: Invest Easy. Should we use? We find out in this in-depth review, with its fees, strategy and pros and cons.

Selma Review 2026 – Pros & Cons

Invest on autopilot. Read our review of Selma Finance, a beginner-friendly Swiss Robo-Advisor, and decide if it is the right tool to grow your wealth.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

For a long-term holder (buy and hold), I think it’s crucial to buy ETFs with a low TER and to minimize custody fees.

I don’t get it why someone with a significant amount of money should use a robo-advisor instead of going with for example IBKR or even Postfinance (flat, low yearly fee)?

Even if the robo-advisor were so good, one could just create a portfolio there and copy-pasta it to a self-managed broker?

Hi Marco

The reason is simple: People don’t want to deal with ETFs themselves and they don’t want to learn about this.

I completely agree that it’s most optimal to use IBKR and an ETF. But the truth is: some people will never learn to do it or would not trust themselves to do it. For these people, a Robo-advisor is the next best thing.

OK I understand, thanks!