What should you do with a life insurance 3a?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Recently, I have talked about life insurance 3a policies and how bad they were. We have established that they have almost only disadvantages compared to an invested 3a.

So, people should not take out new life insurance 3a. But what should you do if you already have one?

There are a few options about what to do with life insurance 3a. We will explore them all in this article and compare them. By the end of this article, you should know what to do about your life insurance 3a.

Life Insurance 3a

We have already established that life insurance 3a has significant disadvantages:

- Their returns are low.

- Their fees are high.

- They are very inflexible for deposits, locking you into this monthly expense.

- They are very inflexible for withdrawals, making you lose money in taxes.

- They are not transparent.

- They are heavily advertised.

The only advantage they have over an invested 3a (like finpension 3a) is that they have a guaranteed amount of money. However, life insurance 3a only guarantees a 0% interest rate, and the guaranteed amount is less than what you paid. If you want guaranteed 3a, you should take a bank 3a.

Life insurance 3a also has insurance in case of disability and death. This extra insurance may sound like a significant advantage. However, most people will not need insurance. Moreover, you can get pure risk life insurance for a fraction of the fees of life insurance 3a.

If you need more convincing, I have an entire article explaining why nobody should fall into the trap of life insurance 3a.

What to do with existing life insurance 3a?

It is essential to know that life insurance 3a is a terrible instrument. But what should you do if you already have one?

First, you should not feel bad about it. Many people in Switzerland are falling for life insurance 3a. I have a life insurance 3a. I am not proud of it, but I consider it a learning opportunity.

Why did I take out life insurance 3a? An insurance advisor convinced me, and I did not know any better. Most people in Switzerland do not have the necessary financial education to understand how bad these products are. And most people in Switzerland trust advisors, banks, and insurance companies.

Banks, advisors, and insurance companies push these products because life insurance 3a is very lucrative. But life insurance 3a is not lucrative for its users.

We now go to the main question: What should we do with life insurance 3a?

There are three main ways to deal with life insurance 3a:

- Do nothing

- Reduce or stop the payments

- Cease the contract

We will see these three ways in detail in this article.

1. Do nothing

The first and simplest option is to do nothing. You continue contributing your monthly premiums, which stay in your life insurance 3a until your retirement age.

While this option is the simplest, it is also the most costly. Indeed, we have seen that life insurance 3a has abysmal returns and is very expensive. These low returns and high fees result in low performance for life insurance 3a in the long term.

In the previous article, I ran a comparison and got these results after 30 years:

We can see that doing nothing can be extremely costly. Over 30 years, investing in a good 3a could easily yield twice as much money by the time you retire.

Overall, I would strongly advise against doing nothing!

2. Release the premiums

The second option is to stop paying the premiums either fully or partially. Most life insurance 3a allows you to be released from the premiums. Once you release the premiums, you will not have to contribute anymore, and the money will stay with the life insurance until the original policy termination date.

From what I know, all life insurance 3a policies include such a clause in their conditions. So, it is generally not a huge deal to do that.

Here is what would happen to the money by stopping paying the premiums, simulated for 30 years.

We can see that the earlier we stop, the better results we get. It is logical since we get better compounding in the invested 3a, with much better returns. The part invested in the life insurance 3a will continue growing slowly over the years, but you could see it as bonds in your portfolio since this money (minus the fees) is guaranteed.

If you stop the premiums very early, in the first few years of the life insurance 3a, you may incur a penalty. Indeed, in the first few years, the life insurance company takes more in premiums for the risk premiums than in the following years. However, the earlier you stop, the better you will end up in retirement.

This strategy always makes sense unless you are extremely close to retirement. Even a few years without fees could help.

You must remember that the stock market returns are great in the long term but not necessarily in the short term. So, if you are close to retirement, below five years, you could stop the premiums and switch to a bank 3a instead. Or, you could be more conservative, depending on your asset allocation.

It is probably worth mentioning that doing that may prevent you from taking on another life insurance 3a. But that is probably a good thing.

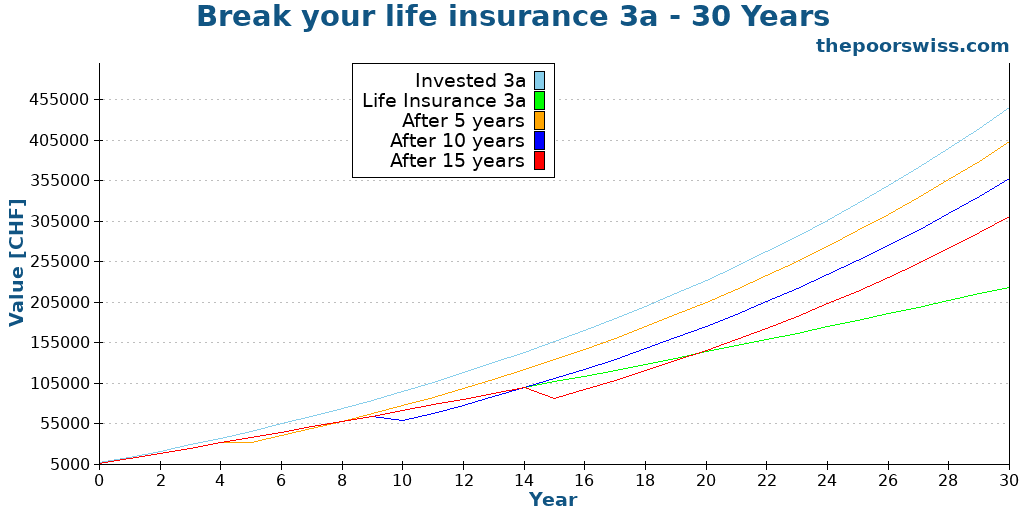

3. Break the contract

The third option is to go a little further and entirely break the contract. With that, you stop paying, and you get back the money from the insurance company.

With this option, you will get back the buyback value. This value is based on the current value minus some cancellation fees. Usually, this value is zero in the first few years of the contract. You have no choice but to transfer this value to another 3a account.

Once again, we can simulate this. I will assume that by canceling the contract, you will lose an extra 20% of the value compared to what you would have in life insurance 3a. This assumption is not precise since, in theory, you would lose more during the first few years and less during the following years. However, this allows us to make a simple simulation.

You may lose more than 20% or less than that based on your life insurance company. Unfortunately, they are not very transparent about these fees.

Here is what would happen if we were to break the contract after 5, 10, and 15 years.

We can see that the penalties can make a significant dent, but the returns of a good 3a easily recover this.

Again, the earlier you break the contract, the better the results will be in retirement. This effect is due to the compounding of the invested 3a.

I should repeat the disclaimer for the previous strategy: if you have only a few years, the stock market’s returns may not be great, depending on the timing. Therefore, breaking your contract a few years before retirement is not a great idea.

This is the strategy we used for our life insurance 3a. We broke the contract and got the money into a proper 3a.

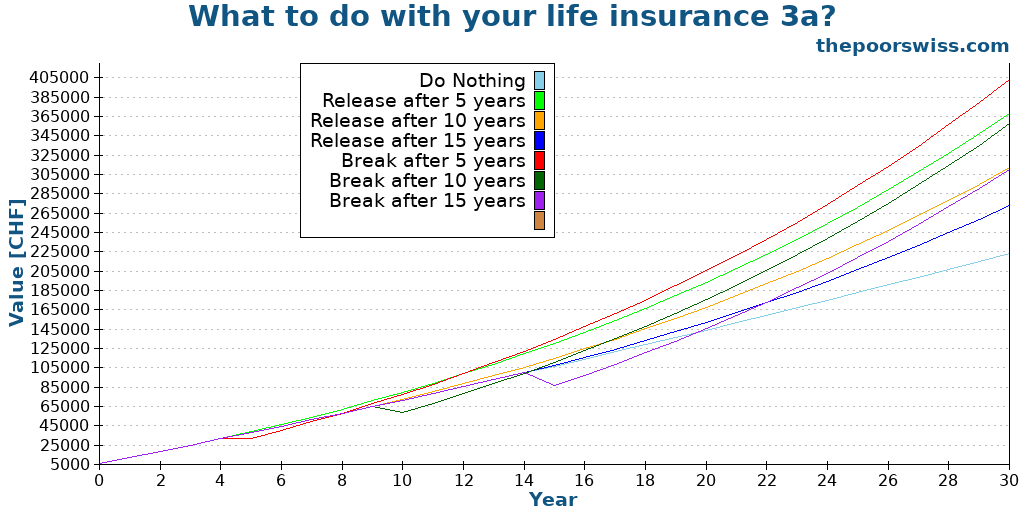

Comparing the three strategy

Here are all three strategies together on our graph to summarize them.

The difference between the worst and best strategies is almost 200’000 CHF! Such an amount of money can make a very significant difference in your life in retirement.

Unless you are very close to retirement, you should do something about your life insurance 3a. And doing something means either releasing your premiums or entirely breaking the contract.

The earlier you can do something, the better your returns will be in the long term. And generally, it should only take a few years to recover the loss from breaking the contract.

So, what makes the most sense is to break the contract and move the little money you get back into a good 3a and then invest regularly into that 3a. Releasing the premiums is also an excellent strategy that can make a lot of difference.

Life insurance 3a and mortgage

If you have tied your life insurance 3a with a mortgage for indirect optimization, you may be unable to change your life insurance.

Indeed, if you are using it for indirect amortization, your life insurance 3a policy belongs to the bank. Therefore, you will not be able to make any changes to the contract without changing the mortgage contract.

In these cases, the best option is to wait until the next contractual deadline for your mortgage. Then, you can either switch to direct amortization or use another third pillar for indirect amortization.

Of course, you can also ask your bank to see if there is a quicker way out.

What we did with our life insurance 3a

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

By now, you may know that I also had a life insurance 3a. And if you have read my previous article on life insurance third pillar, you will know that my life insurance policy was really bad.

Early on, I thought I would keep it as a reminder of my error. Then, I was thinking of lowering the premium from 300 CHF per month to 100 CHF since it seemed possible. Since I had to wait a few more years because of my mortgage, I wrote these articles to support my evidence.

At this point, I have realized that my life insurance 3a needs to stop. Before, I did not know it was possible to stop paying the premiums completely.

In December 2025, we told the insurance company (with a letter) that we wanted to break the contract. The letter also included details on where to move the money (Finpension 3a). About a month later, we got the money into our regular 3a. Meanwhile, we also got a call from the advisor asking us if we were sure. It did not take him long to understand I was serious about this.

We have lost a significant amount of money (about 12,000 CHF) by breaking the contract. However, I have no doubt that breaking it now and moving the money to a much better 3a will pay off in the long term. If we had kept it, we would have lost money every year.

Conclusion

If you are trapped with a bad life insurance 3a, I strongly encourage you to do something about it. At least you should learn more about how they deliver very poor returns, have high fees, and are not transparent.

The results of this article show that doing nothing may cost you a lot of money in retirement. Before doing this analysis, I considered doing nothing. However, I have realized I need to break my contract, and as of 2026, we now have no more life insurance 3a.

If you need to find a good 3a after reading this article, you should read about the best third pillars in Switzerland.

What about you? What will you do with your life insurance 3a?

More reading

Early retiree in Switzerland – Dror’s Story

Real FIRE stories. Meet a reader who retired early in Switzerland. Learn from their journey, their asset allocation, and their daily life.

The Three Pillars of Retirement in Switzerland

Master the Swiss pension system. Learn how the Three Pillars work together and what you need to do to secure a comfortable retirement in Switzerland.

Disaster File – A Simple Way to Prepare for Your Death

Secure your family's future. Learn how to create a "Disaster File" with essential documents and passwords to help your loved ones if you pass away.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Thank you, I had precisely this question! I have asked for a bunch of info (valuation, etc) from my insurance and will then calculate and see what to do (I have only 15 years left but it’s still 15 years!)

Well done for asking your insurance information and taking matter in your own hands!

Dear Baptiste,

Thank you for the insightful research you have shared. I am indeed also a victim of this scam and have my 3a pillar with an insurance provider since 2021 and my 3b with them since last year. I have no intention to leave Switzerland my policies are not linked to a mortgage so my intention would be to release the payments and then move the money to another provider. Do I understand the information correctly that I should contact Axa and confirm the penalty I will incur to stop the premiums and transfer the money to another provider. I don’t feel very knowledgeable on this topic, and I want to be prepared for when I contact Axa. I am struggling to find any information on cancellation fees /minimum holding period so as not to incur fees etc. Many thanks for your advice.

Hi Kelly

Sorry to hear about your experience!

Releasing the premiums and canceling are two different things. If you want to transfer the money out, you will have to cancel the contract. It is the same kind of letter that you would write to your health insurance to cancel a policy. You tell them you want to cancel the policy (with the policy number and details) and you want them to transfer the proceedings to another 3a foundation. In the case of the 3b, it’s the same but you can disburse the funds into your own bank account.

Hi Baptiste,

Could you share a bit more on how you can release the premiums? If I contact Swiss Life to request this will they know what I’m talking about?

I have a SwissLife 3a life insurance, I started in December 21, so I’ve paid in three years in total. I read my contract and it doesn’t say anything about reducing the premium, only surrendering the value (I paid 21k so far and the surrender value would be 14k).

Thank you!

Hi RH

You would have to send them a letter (with signature, it’s better) in which you state that you want to release the premiums. You probably should write this in one of the national languages, include the date at which you would like to stop, sign and date and it should be good. They know what it is because it’s a common thing in insurance contracts.

Surrendering is different because it means breaking the contract entirely.

Thank you Baptiste!

I called them today to discuss and ask for the address to send the letter to. They said I did not pay enough into the policy to do this yet :( They will send me a letter stating how much needs to be paid into the policy before I can request this in future. I hope it’s not too much! She said in the meantime if I don’t want to pay (since I am not working at the moment) I can request a premium break of one year. Do you have and insights into premium breaks?

Also something interesting I noted, the lady on the phone was unsure of what ‘release the premium’ was and kept referring to it as the ‘paid up option’ instead.

Thank you for your advice, I am very grateful!

Be careful that they are often some scare tactics and they are not opposed to lying. I am not saying it’s the case here, but I have heard multiple cases where they were trying people to keep their policies.

Normally, you can always release the premiums because it’s part of the third pillar. And there should be no limit to when you can do it.

Maybe she was referring to breaking the contract. And in this case, it’s indeed possible that you have no value if you cancel it now.

Hello Baptiste,

I was wondering if you can provide more details on 3a bound to the mortgage, I am still quite confused about what to do in these cases, and after learning about these scams I am literally losing sleep.

my wife and I have a mortgage with Helvetia with fixed interest rate until 2029. Per contract, we are doing indirect amortement maxing out the contributions to our resepctive insurance 3a

It is not clear what exaclty we should do. I understood from the article you were in a similar situation, and planned to break the contract at the end of the period. (To clarify, that means you will seek a new mortgage with another provider is that correct?)

but until 2029, it is not clear what should we do exaclty? it seems per contract we are bound to keep maxing the respective 3a. On the top of that, we also have a “gage immobilier” and it is not clear if this is preventing us to release the premiums.

any help or suggestion really appreciated

thanks!

Hi Andrea

In 2029, you will renegotiate your mortgage. In this case, you can also renegotiate the amortization. So, you can ask to stop doing indirect amortization and switch to direct amortization. They may ask you to amortize more at this point. And then, they will give you back your insurance policy. And you will be free to cancel that policy.

Until 2029, the contract does not belong to you but the bank. So, there is not much you can do. You cannot release the premiums because then you would be breaking the mortgage as wel. You could break the mortgage contract but that it very expensive. If you stuck a very good deal with another bank, you could transfer the mortgage to a new bank, but again, this is unlikely to be worth it.

So, just like us, the best course of action is to wait until renegotiation.

Hi Baptiste!

My wife and I, we both have a third pillar 3a with Swiss Life (my contract started in 2019 and my wife started in 2020. Things changed in our life and now my wife left Switzerland. Since she moved abroad, she can cash out the money but we realized that we will loose 1/3 of the invested money. I was thinking to move her third pillar to a 3b and continue investing but after reading your article I don’t feel that’s a good idea. Do you think we should cash out the money and assume that we are going to loose part of the money or there are some other strategy to avoid loosing these amount of money. Another question I have is regarding my third pillar. I will continue leaving in Switzerland for more 2 years and for this reason what do you recommend? Break the contract and go with Finpension for these 2 years to come or simple release the premiums and continue to put the money in the Swiss Life 3a pillar. Thanks in advance.

Hi Marcelo

If you can, I would recommend breaking both contracts. The worst you can do is continue putting money in the contract. So, at least, you should release the premiums, and then you will have more time to think about breaking the contract.

Of course, losing the money sucks. But when you consider the long-term gains, it makes a lot of sense.

So in the case of my wife I should cash out the money immediately since she’s moving abroad and in my case I should break the contract. But since I will continue living in Switzerland do you think I should move my 3a pillar to another institution like a bank? Do you think it make sense to do this?

That’s what I would do. But you have to weigh everything for your own situation.

You have no choice in your case but to move to another 3a. Since you only have a few years, this money is likely best uninvested. You could move it to any free 3a account with some interest rate and then keep it there until you leave Switzerland for good.

Bloody scammers! They do this with everyone without suffering any legal consequences for absolutely unfair conditions when it comes to transparency and costs. People should unite and file a huge lawsuit against them! I also lost 10k and had no service whatsoever.

Hi Baptiste,

This article is just great. It should be part of the onboarding kit when you arrive to Switzerland :)

On my side, I’ve been paying a life insurance 3a for the last 6 years (PAX, max amount / year) and I’m trying to figure out the best alternative, taking into account that I may leave Switzerland in 2027:

a) Reduce the payments to the minimum

b) Release the contract

c) Break the contract

In any case, I would probably go with VIAC or Finpension 3a with the remaining amount up to 7056 CHF / year.

Because I may need to leave CH in 3 years, I think a) or b) may make more sense to minimize the penalties. Would you agree? Would VIAC has more advantages than Finpension 3a when it comes to leave Switzerland? Many thanks!

Hi Rod,

Thanks! I wish there was such an onboarding kit!

In any case, don’t reduce the premiums to a minimum they advocate, release the premiums fully to 0. You want to stop pouring more money into it.

Whether you break the contract or not is up to you. There will be penalties, but putting this money in a good 3a (if you are young) will compensate for it.

As for leaving Switzerland, it depends on where you leave to. In most countries, you will keep your 3a until retirement age. In some countries, you can withdraw the 3a upon leaving. Finpension has fees for withdrawing abroad indeed but it has a better tax domicile, so it will depend on the sum inside the account at withdrawal.

Hello, I have a question.

I’ve made several contracts with AXA SmartFlex ( one 3a and two 3b) I’ve been paying 300.- per month since I made them and today I have around 500.- on my 3a and my 3b and 1500 in my other 3b account.

I want to quit AXA because I want to invest my money better into finpension, and also because they’ve been making a lot of mistakes and not assuming their responsibility.

For example, I lost my job last year and instead of pausing my 3b monthly payments as I asked them, they stopped my 3a, and I just discovered that when I was filling my taxes. Ont of my 3b was made for my nephew, and I wanted it to be able to cash out at his 20’s but the contract goes until 2060 etc…

I already sent them the form to transfer my 3a money into Finpension, but concerning the 3b’s if I try to “buy them back” 3b the total goes to 0. So I’m loosing 2000.- what should I do in this case ?

Hi Jorge

Good decision!

Sorry to hear about your troubles, seems very unprofessional of them.

The only other thing you can do is release the premiums (stop paying, by sending them a letter). This will keep the money in the 3b and you won’t have to pay more.

Thank you, Baptiste, for such an “eye-opener” article. I’m also one who has fallen into the trap of life insurance 3a!

I’m an employee and have a 3a insurance policy with Zurich with a high “capital guarantee”. I have paid CHF 588 per month from Jan 2023 until now.

On top, in March 2023 I transferred CHF 13776 from my bank 3a account into this life insurance…all with the support of my “independent” financial advisor!!!

All in all, I have paid CHF 22k up to now.

Zurich sucks when it comes to reporting as they don’t have any online service. However, based on a document I received from them, it seems that before 31-Dec-2024 the surrender value is CHF 0. By that time the surrender will be CFH 20k.

In this case, it would be better to stop paying premiums (i.e. releasing the premiums or reducing them to the minimum) now?

Or should I continue paying premiums until December 2024 to get back CHF 20k in surrender value?

The other question I have is if releasing the premiums is the same as converting this to a “paid-up policy”?

Hi Juan

Sorry to hear about that!

Normally, whether you release the premiums or not, you should be able to get back some money since th surrender value is set to increase soon. Ideally, you should ask them what is the surrender value in January 2025 if you release the premiums now, but they will resist and try to trick you…

If you are sure that the surrender value will be 20k in January 2025, then paying the premiums until the end of the year and then breaking the contract would be a good way to get a significant part of what you put into.

I do not know what is a “paid-up policy”.

Thank you, Baptiste,

I’ve extracted this from a document containing the general conditions of my life insurance:

“Can this insurance be converted to paid-up insurance or

surrendered?

Conversion into a paid-up policy

The policyholder is entitled to request that the insurance be converted

to a paid-up policy at any time with correspondingly reduced benefits.

All supplementary insurance policies will lapse. The effective date for

conversion is the end of the period for which a premium was last paid.

The future administration costs and any risk premiums will be financed

from the contractual capital.”

It seems that converting to a “paid-up” policy is the same as releasing the premiums…

I have requested Zurich to confirm what would be the surrender values in both cases: releasing or reducing the premiums. I’ll keep you posted!

Interesting way to put it, it’s not very clear.

I think it’s indeed the same as releasing the premiums. And surrendered policy would mean breaking the contract.

Hello everyone,

It seems I felt in the same trap with life 3a life insurance.

Did anyone experienced issues getting a separate pure life insurance not tied to 3a or 3b from a different company? (after canceling the 3a contract)

By issues I mean price increase for new life insurance or refusal for the new life insurance?

Thanks for the blog post Baptiste,

Cheers

Hi Vladimir,

Sorry to hear that!

I have never heard that, but I know it’s possible because they consider that a client that canceled once can cancel multiple times in the future.

What you could do is take pure life insurance before canceling your tied life insurance.

Hi All,

I believe this article is missing a 4th option to reduce the scam value of a 3a with life insurance: buy an apartment using the surrender value and then wait until the end of contract to recover the last portion of the “costs” (20%). This way one would utilise immediately 80% (surrender value) and then get the rest at the end. What does PS think about it?

Cheers

Hi Al,

Keep in mind that you can’t recovered everything. It’s true that the last few years is where a lot of the money is “vesting”, but the risks costs are lost.

You could take out some money early for a house or pledge it and then run the insurance to the end.

I am not sure this would be much better but this would avoid breaking the contract. The most important is to release the premiums as to stop paying more into the scam.

Thus option does not exist. Once the capital is reduced there won’t be any recovery of the 20% since the interests money simply won’t be there. Basically they stole 20% of your money, full stop. That’s the ugly truth. What is unacceptable is that the government backs those scams without intervening supporting consumers and legally blocking the scams. Peiple like us trust our brokers and the fact those are known options labeled 3a so one wouldn’t think of a scam. The other crazy stuff is those big companies are still able to hide contractual terms and costs without giving and indications, this is all legal!