The Trap of Life Insurance Third Pillar

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

For your third pillar, you can choose between an account at a third pillar provider or a life insurance policy. Many people (often advisors) recommend using a life insurance policy.

However, in practice, these life insurance third pillars have many disadvantages. There is no reason to use a life insurance 3a for your third pillar.

In this article, I detail the differences between a third pillar with a bank or an independent provider and a life insurance third pillar (life insurance 3a).

Life Insurance Third Pillar

The third pillar is open to workers who pay into the second and independent people who own companies. The idea of the third pillar is simple: save money while you work and get it back when you retire.

The main advantage of the third pillar is that you can deduct your contributions from your taxable income. The third pillar is an excellent way to reduce your taxes. However, employees are limited to 7258 CHF (in 2025) annually. Generally, I recommend most people contribute to their third pillar. I contribute the maximum every year.

For your third pillar, you have two choices:

- An account with a bank or an independent provider (Finpension 3a or VIAC, for instance). I call these standard 3a accounts.

- Life insurance third pillar with most insurance providers in Switzerland. I call this life insurance 3a.

Both options have the same basics:

- You can deduct the contributions from your taxable income

- The money is locked until retirement

- Or until some specific conditions, as seen later

Both standard 3a and life insurance 3a can be invested. In both cases, there are some special retirement funds available. So, your money can be invested in stocks, bonds, or other alternative investments. Since the third pillar is a long-term account, it is excellent to invest this money.

However, they have some significant differences. And as we will see in this article, most of these differences are disadvantages of the life insurance version.

Life Insurance 3a is not flexible

Lets’s start with the first difference: flexibility.

With a standard third-pillar account, you can deposit money whenever you want. But with life insurance 3a, you must pay your premium regularly. For most providers, you will pay for months. But, you may have to pay quarterly, semi-annually or even annually. This limitation leads to several disadvantages.

First, if you want to max out your third pillar in January and forget about it, you can do it with a third pillar in a bank. With life insurance, you have no choice but to pay when the insurance tells you to.

More importantly, if you are having a bad year and do not want to contribute to your third pillar, you cannot stop paying your life insurance (without penalty). On the other hand, you can stop paying your 3a account for several years if you want. This lack of flexibility is important because it means your life insurance 3a can put you in trouble.

Finally, the maximum amount for the 3a changes every few years. If you start your life insurance 3a with a full contribution, this contribution will not follow the increase over the year.

For instance, in 2019, the maximum contribution was 6826 CHF. But in 2021, the maximum increased to 6883 CHF. If you got your life insurance 3a in 2020, you already lose 57 CHF per year in potential tax deductions. And this will increase every few years.

Of course, you could take out a standard 3a on the side to reach the maximum contribution, but most people will simply not. Usually, this limit will increase every two years. Currently, the limit is 7258 CHF (in 2025).

With life insurance 3a, you are also not flexible on withdrawal. With a standard 3a account, you can withdraw money early or late. But with insurance, you can only withdraw it on the date set on the contract. So, you are stuck if you want to withdraw later or sooner than your retirement date. A standard 3a account allows you to withdraw up to 5 years in advance or up to 5 years late.

Life Insurance is not tax-efficient

While you contribute to them, both a standard 3a and a life insurance 3a are equally efficient. However, when it comes to withdrawing them, standard 3a has the potential to save you a very significant amount of money.

The reason is simple: you cannot stagger withdrawals of the life insurance 3a. Usually, you want five different third pillars. Then, you can withdraw a single third pillar account annually to save on taxes.

Indeed, the taxes in most cantons are progressive. You pay a fixed percentage on each bracket. For instance, you would pay a 5% fee on the first 30K, then a 10% fee on the next 30K, and so on.

So, if you can withdraw over several years, you can save significant money. We talk about up to 50% tax savings in the best cases. With staggered withdrawals, you could easily save more than 10’000 CHF!

And with a life insurance 3a, you are wasting money on taxes.

One may argue that you could have several insurance policies, and in theory, you could. However, most life insurance will run to your retirement date, not earlier or later. In practice, it will be tough to plan this properly. And you have to get it right the first time since you cannot change it afterward.

Life Insurance 3a fees are expensive

Many people do not realize that when you invest in life insurance 3a, a significant percentage of your contributions feed the risk premiums. Since this is life insurance, it can pay out in case of death or disability.

And this does not come from the principal but from the risk premiums. Each contribution is split into two parts. Some percentage goes into the capital and stays there until retirement. Another portion goes to the risk premium. This percentage is lost to you and goes to the insurance company.

There is nothing wrong with the principle. Insurances need risk premiums to cover the risks for their customers. However, there are a few things wrong when related to your 3a:

- The risk premium percentage is very significant

- A significant part of your retirement money is lost

- Advisors are not forthcoming with this

In practice, life insurance will take anything from 10% to 25% of your contributions. Every time you contribute to your life insurance 3a, you lose 10% to 25%!

For many people, it is already challenging to contribute a significant amount of money to their third pillar. And seeing such a large percentage disappear is not comfortable!

Not only that, but the fees of the funds available are also very high. I have looked into the funds from Generali, where I have my life insurance, and the fees of funds are all about 1%. And some insurance companies invest in funds with more than 2% yearly fees. And the advisors telling you that these active funds will outperform the market are either lying or delusional.

On top of that, many of these funds have load fees. You will lose even more of your money before it is invested. It is not uncommon to see 5% load fees. Again, whenever your money is invested into the funds, you lose 5% of the value!

So, these high fees will reduce your performance even more.

Life Insurance 3a returns are bad

The advisors will tell you you can get good returns on your life insurance 3a. But in practice, this is far from correct.

You can indeed invest your money from your life insurance 3a. However, the money is invested in expensive active funds that will significantly underperform the market in the long term.

On top of that, these investments are generally very conservative. It is rare to go higher than 35% in stocks. Since this money is locked away for several decades, a high stock allocation would make more sense.

We can take my Generali life insurance 3a as an example. I started to invest in August 2016. At the end of 2019, I asked them about the performance of my money. On average, I got 0.4% returns per year. During that same, the US stock market returned 45%, and the Swiss stock market returned 30%.

And the finpension Global 40 fund would have returned about 19%! Again, finpension 3a would have 45 times more returns during the same period!

The two funds for my life insurance invest 35% in stocks. So, having 0.4% returns yearly during a bull market is a joke!

We can compare one of the funds from Generali, GENERAL INVEST – Risk Control 5, with some other investment options from February 2015 to September 2022:

- Generali INVEST: -10%

- Swiss Stock Market (SPI) ETF: +29%

- US Stock Market (S&P 500) ETF: +87%

- finpension global 40: +23%

- finpension global 100: +69%

With a conservative portfolio at finpension, you would have gained 29% of your money. But with a conservative fund at Generali, you would have lost 10% of your money!

Before making that comparison, I knew that Generali funds were bad, but I had no idea how bad they were. This performance is atrocious.

You likely do not need the insurance

One advantage of life insurance 3a is that you get some insurance benefits.

If you die before retirement, your spouse will get the capital you would have gotten at retirement. And if you are incapacitated and unable to pay your premiums, the insurance will pay for you.

Insurance is all good, but do you need insurance coverage? Advisors will tell you everybody needs this insurance coverage, which is dumb. Insurance that is always worthwhile has not been invented.

First, you do not need death life insurance without dependents or heirs. If nobody depends on you and you die, the capital will go through standard inheritance order or return to the insurance company if you have no heirs.

Indeed, this could still go to your heirs even if you have no dependents. But you must ask yourself whether they need that insurance if they are not depending on you. People should generally take out life insurance only if they have people who depend on them financially. But if they do not, life insurance is likely useless.

Then, we have good insurance coverage already in Switzerland in numerous instances.

And if you are a double-income earner household, chances are that your spouse could handle the financial side without you. On top of that, the first and second pillars have benefits for your spouse if you die.

If you lose your job, you will get up to 80% of your income for up to 3 years. You would still be able to pay your life insurance premiums and are unlikely to be in financial trouble.

If you are disabled, you will get disability insurance and receive assistance to return to work if possible.

The need for life insurance is reserved for very few cases. In which cases, better options exist, like pure risk term life insurance.

Life insurance 3a has guaranteed value

We now go over the last difference. A life insurance 3a has some guaranteed value. On the other hand, a standard invested 3a account has no guaranteed value.

Now, we need to relativize that guarantee. First, no interest is guaranteed. So what is guaranteed is the amount without any performance. The performance cannot be negative.

However, you should know that the guaranteed value differs from what you contributed. We have seen that fees are expensive before. These overall fees include the risk premiums. At least 10% of your contributions will be lost to the risk premiums and direct fees.

Since we have seen that returns are very low for life insurance and that you will lose at least 10% to risk, the guaranteed value is not that interesting anymore.

If you invest that money long-term, you can expect significantly more money. While there have been some 20-year bad periods in the stock market, they are very rare. And over 30 years, the stock market has historically been great.

Life Insurance 3a vs invested 3a

Finally, we can make a small comparison of some products. We will have to assume a few things:

- The bank 3a account will return 0.1% per year, and there are no fees

- The life insurance 3a will return 1% per year after fees, and 10% of the investments will go to the risk premiums

- The invested 3a will return 4.5% per year after fees, and there are no extra fees

Each year of the simulation, 6883 gets invested into the product. There are no adjustments for this amount over time. In practice, this amount would rise for the bank 3a and the invested 3a.

You may think the invested 3a has an advantage in my assumptions. But my numbers are pretty conservative in both senses. A 3a invested 99% in stocks could return significantly more than 4.5% per year. And on the other hand, many life insurance 3a will return less than 1% per year (mine returned 0.4% on average during a bull market for three years).

And on top of that, some insurance will charge more than 20% for the risk premiums. So, these assumptions are being nice to life insurance 3a.

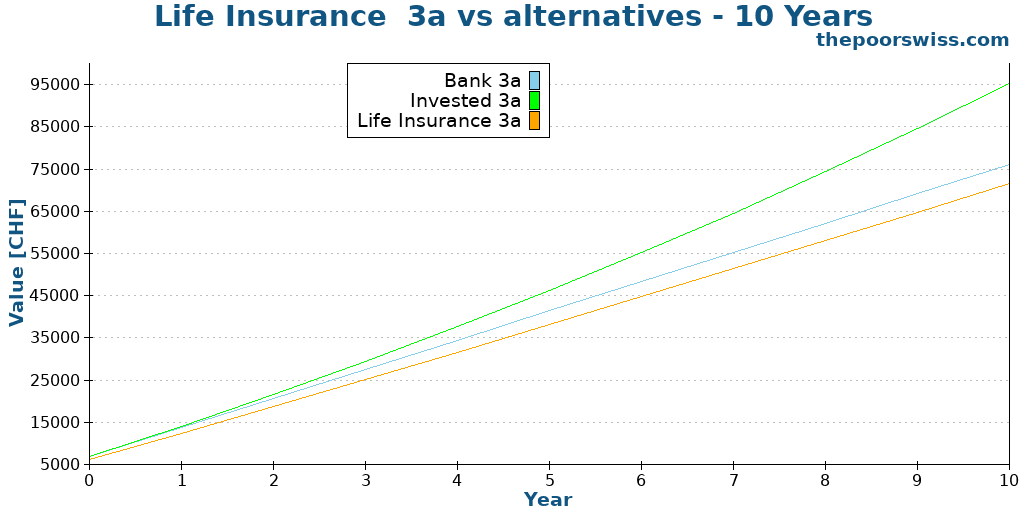

So, here is how these three products would result after ten years:

The result is quite surprising. After ten years, you would be better off with a bank 3a with a 0.1% interest rate than a life insurance 3a. Losing 10% of the premiums makes a huge difference, and poor returns make compensating difficult. Even over ten years, a bank 3a would leave you with 5000 CHF more than the life insurance 3a. With a good 3a, you would have about 23K CHF. Such an amount of money can make a very significant difference in your retirement.

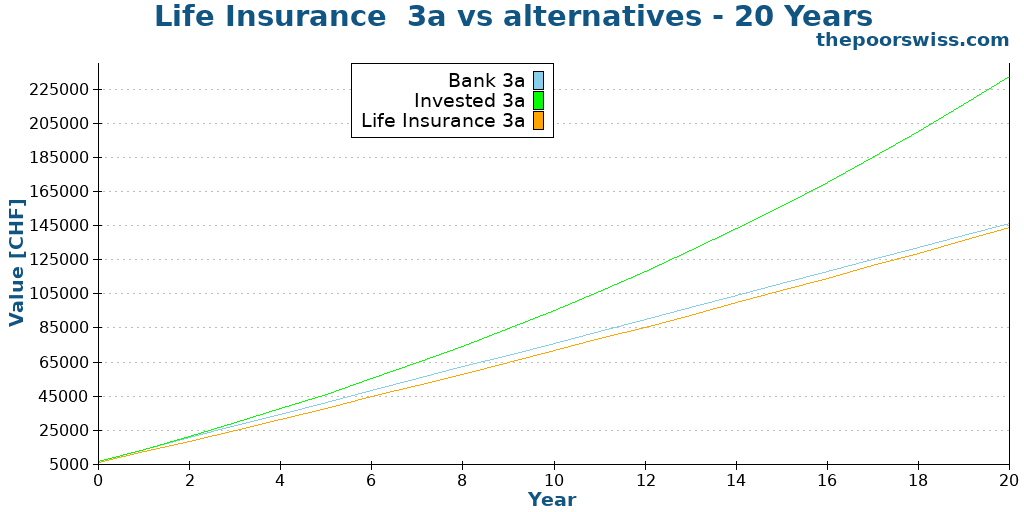

Here is what happens after twenty years.

After twenty years, life insurance 3a still is worse than bank 3a. This result is bad. The difference is only 2000 CHF, but it still shows the extremely poor returns of life insurance 3a.

After twenty years, the difference with a good 3a becomes extremely impressive. Indeed, in that simulation, the invested 3a has 88K CHF more than the life insurance 3a. Put another way, the person with an invested 3a has 61% more money in retirement than the person with a life insurance 3a.

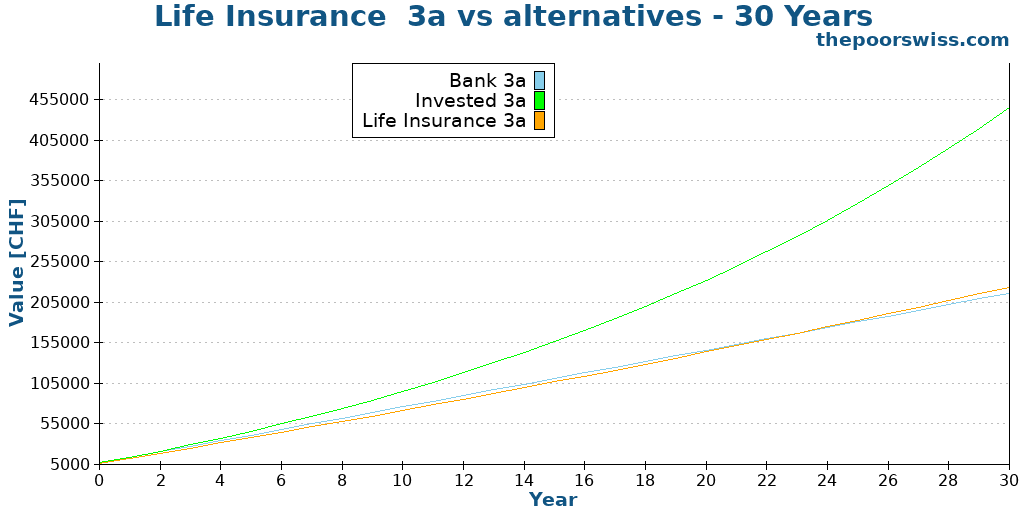

Finally, we look at thirty years.

Finally, life insurance 3a is at the same level as bank 3a. However, the difference is only 7000 CHF.

After thirty years, the invested 3a now has twice more money as the life insurance 3a. We are talking about a difference of more than 220’000 CHF after thirty years. Such an amount of money could change your life in retirement.

This result comes from only a single simulation. In practice, there are some cases where life insurance would do better than this one. But there are also cases where the invested 3a does much better. And there are some much worse insurance policies out there. I strongly doubt any insurance 3a comes close to a good invested 3a.

Why does life insurance 3a exist?

With all these disadvantages, we may wonder why these products exist. And it is a fair question.

After doing all this research, I believe life insurance 3a should not exist! They are horrible investments and will likely result in much lower retirement money than if you had used a proper third pillar account.

The reason life insurance 3a exists is simple: they are highly profitable to insurance companies and insurance advisors. I think there is no good reason for their existence.

Advisors make large commissions on these products. So, they push these products quite hard. Unfortunately, most Swiss people are not educated enough about investment and retirement to understand these products. And most people trust advisors.

What to do instead?

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

The third pillar in Switzerland is great for investing money and saving taxes. Life insurance 3a being bad should not stop you from investing in the third pillar.

If we eliminate life insurance 3a, there are two options for your third pillar. Either you invest with a bank, or you invest with an independent provider. In practice, I highly recommend using an independent provider like Finpension 3a.

Finpension (and other independent providers) has many advantages over a life insurance 3a:

- You will get more returns on average

- All your contributions will go to the capital

- You will pay lower fees on the invested capital

- You will get a more transparent third pillar

- You are flexible as to when you contribute

- You can save taxes with staggered withdrawals

And if you are afraid of investing and want guaranteed capital, you can invest in a bank and get a tiny interest rate. In my opinion, a bank 3a is already better than a life insurance 3a.

If you need help choosing the third pillar, read my articles about the best third pillar in Switzerland.

In 2026, we broke our life insurance 3a contract and transferred the money to Finpension 3a.

And if you need life insurance, you should get a pure-risk term life insurance policy. There are many of them. I have never delved into them, so I do not know which is best, but I am sure there are some good ones.

For a simple example, I have looked at rates for Allianz for 30 years and 120,000 CHF coverage, comparable to my insurance policy. This pure risk life insurance includes paying your premiums if you are incapacitated. So, this is very close to a life insurance 3a.

Such insurance would cost me 379 CHF per year. Over 30 years, this pure risk life insurance would cost 11,370 CHF. If you remember the results two sections before, the life insurance 3a will result in 220,000 CHF less money than the invested 3a. For the cost of 11,370 CHF, you can get a great 3a and separate life insurance.

Note that I do not particularly endorse Allianz. Their calculator is the simplest I found.

This simple comparison shows how bad life insurance 3a is. You can get good life insurance for cheap and good 3a with much higher returns and transparency.

Conclusion

When I started this article, I knew life insurance 3a was a bad investment. But after going through the research, I now realize life insurance 3a is a horrible investment!

There are much better alternatives out there. I would not recommend life insurance 3a to anyone. Instead, use a great third pillar like finpension (my review here). And if you need life insurance, take pure risk insurance instead and continue investing in a good 3a.

Now, there is one question I have not answered in this article: What should you do if you already have a bad life insurance 3a? First, do not be ashamed. Many people fell into the life insurance 3a trap, including me. That is right! I fell into this trap! And unfortunately, many expats fall into this trap.

There are a few options to get out of a life insurance 3a. I encourage you to at least look at them if you have life insurance 3a. In 2026, we broke our contract and got our money out of the trap.

To start investing with an excellent third pillar, you should read about the best third pillar from Switzerland or my review of Finpension 3a.

What about you? What do you think of life insurance 3a? Did you fall into this trap?

More reading

3a buybacks are now possible: All you need to know

Missed a year? Learn about the new 3a Buyback rules. Discover who is eligible to make retroactive contributions and save taxes on past years.

Can you retire early with Swiss Stocks and Bonds?

Can we retire early with only Swiss stocks and bonds? We find out with Trinity Study simulations with historical Swiss stocks and bonds data.

Old-age care costs in Switzerland

Is Swiss old-age care affordable? From at-home support to residential homes, find out the costs of aging in Switzerland and who is paying for the bill.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello Baptiste,

Thanks a lot about the useful article and giving a lot more clarity on the problematic of 3a Insurance. Unfortunately, me and my partner are both 2 years in the SwissLife pillar. We will be losing 5k between surrender value and current value. I understand that anyway the best way to proceed would be to take out the money but I wanted to understand a little bit better on this point. Where does this money go? Can I cash it out or it just move to another account. We are very frustrated from this situation and we just want to move ahead and see how we can improve our situation.

Thanks a lot in advance and congrats on your contributions

Being it 3A money, it is bound: you will have to move it to another 3A. I can warmly suggest finpension.

If you ask my friend OxygeN on the forum, he’ll be happy to share his invitation code, by means of which you and him will get a little “bonus” from finpension ;-)

Hi,

Sorry to hear you are also stuck with these contracts.

The money can only go to a 3a, you cannot cash it out. It sucks losing the money now but if you are young, you should be much better off losing some money now than losing money over the next decades.

Next year, we will finally be able to cancel our 3a life insurance. We will have lost 15k overall, but I am quite happy about finally getting rid of it.

Hello Baptiste,

What do you mean that next year you can finally cancel? Is that last that you are referring to a difference to the save amount?

No, the policy is currently stuck in a mortgage that gets canceled at the end of the year, so I can do the necessary changes to cancel it early next year.

Hi Baptiste,

thank you very much for your useful content!

Being an expat, I fell to Swisslife myself but I started paying the premiums only in June 2025, which means I can still cease the contract with limited bad outcomes. I have opened a FP 3a account to invest the remaining portion of the third pillar before the end of the year, and now my question is: being already mid november, do you think it’s better to let the year end to cumulate the 7258 CHF and then cease the contract in January 2026? what’s the best strategy in this case in this specific time of the year in your opinion? thanks a lot!

Quit ASAP! the more you wait the more they will steal from you! personally I lost 12k in 10 years and they kept on advising me to wait as the contract gets better with time. All a pile of rubbish! they just tell you to wait until the compound effect starts recouping the losses of their hidden costs….. I can’t stop calling them a bunch of crooks.

Thank you Alfonso for bringin your inputs! I’m preparing everything is needed to cancel it.

Hi JV

Sorry to hear you were sold one of these contracts :(

If you want to cancel, cancel ASAP. There is no reason to wait more. As you said, you will have limited bad outcome. But anything more you put in now is likely lost, so don’t wait.

Thanks Baptiste for the feedback, I stopped the LSV from the bank so that I know no more funds will be going there – sending the transfer request tomorrow! let’s see if I can recover something from the total I invested there in these months.

I hope you can get something back, but after such a short time, I would be surprised :(

Dear Baptiste,

My partner and I are in a bind; our mortgage is structured with indirect amortisation via SwissLife policies (one 3a – my husband and two 3b – mine and my husband’s), and the surrender values look shockingly low compared to what we’ve paid. We’re trying to figure out the best path forward. I’d love to hear what you would suggest doing and others have done in similar situations and any advice you’d share.

Thank you in advance!

Hi Sara

Sorry to hear that.

As far as I know, the only way to get a 3a insurance out of a mortgage is when you renew it. So, on your next renewal date, you will be able to get out the indirect amortization and switch to something else. This is what my bank told me.

I would suggest asking your bank what your options are for changing amortization.

Hi Batiste,

Maybe you can help with these 2 options. I have a VIAC 3a and (unfortunatelly) a SwissLife insurance 3a since 2022. I want to stop this one and return to the 3a investment on VIAC.

I can (correct me if I am wrong):

1) Break the swisslife contract, with the associated penalties and request the money transfer to another 3a.

2) Request the suspension of Swisslife payments, having I believe also some penalties.

As the future withdrawals after retirement should be staggered for tax efficiency, would you recommend (since i made only 3 anual payments for the 3a from Swisslife) the option 2 and start another portfolio elsewhere. Then I just leave this portfolio there.

This would make sense for me in case the difference on penalties of option 1 and 2 is significative.

If the penalties are the same for break the contract and withdraw the money or suspend the payments, I would remove it anyway.

Thank you and KR,

Hugo

Hi Hugo

The penalties are much less in option 2, but the problem with option 2 is that you are going to leave some money in a bad fund for a while. The good thing is that you can do 2) directly and then think about 1) later.

You can transfer the current portfolio into a new account at VIAC for instance, to keep it separate for staggering.

Thank you for the reply.

I will do the 2nd option immediately (I have 1 annual payment for Swisslife in Dec), and compare the last 3-5 years ROI on the funds from Swisslife (good thing I can see on my customer account where the money is invested, which ETF’s and how much in each, the % in cash, the collateral, etc). Then I will compare for the next 20 years this return vs a VOO average return, and probably will reach the conclusion you mentioned :), the ROI is far from good on the life insurance 3a.

Again, many thanks for your help clarifying these topics, trully appreciate it.

KR,

Hugo

Sounds like a good strategy! Please let us know what you find, Hugo!

Hi Baptiste,

a year ago I have decided ro sign a 3a pillar contract with SwissLife (with a SwissLife select advisor), but after reading your analysis and negative reviews online I’d like to quit it.

I know it could be complicated and I would likely face a huge loss. Better sooner than later!

How to do it? I was thinking to send them a letter, but what would happen to the money I have already deposited? Locked until retirement or can I move to another 3a pillar I’m already using?

Any other advice to avoid problems?

Thank you for your time and your help.

You will move all the money to another 3A – that’s how it works.

Hi Nicola,

It’s not really complicated. You should indeed send them a letter to break the contract and tell them to release any of the available funds.

You can move the money available (if any) to another 3a, no locking.

Thank you so much, Baptiste!

If you have been paying the 3a life insurance for over 15 years, what is the best way to get out of it? (It is not backing up any mortgage or anything.)

I would need to look for a 3a bank account to change to?

Kind regards,

Susy

Hi Susy,

If you want out, you would need to open another 3a first indeed to be ready for the transfer. Then, you must break the contract with the life insurance and tell them to transfer the proceedings to your new 3a.

Dear Baptiste,

Thank you creating this amazing website. I have a Viac 3a (2017-2022) but in a moment of “Madness” I was convinced of the benefits of a Life insurance “Swisslife” since 2 years. Do you have an idea of the amount I would have to pay to cancel the contract and return to my deposits on the Viac?

Many thanks and wish you a good weekend,

KR,

Hugo

Hi Hugo

You will not pay anything in general. However, you will lose a significant portion of what you have invested. What matters now is to stop paying (release the premiums) as soon as possible. And then you can take the decision of whether you want to break the contract or not. It’s possible you will lose almost everything you invested for two years. At least, you will likely lose 50% because the first year is often always used for insurance premiums.

@Dostinja – you still haven’t told us if you’re working for AXA, which is a legitimate question after reading your comments (you’re the only one “defending” the 3A life insurance). Of course the 3A as such (WITHOUT the life insurance part) is thought as a long-term investment and for retirement planning. Nobody is discussing this! You’re just skipping/avoiding the part where we all say and confirm (with proof!) that 3A WITH life insurance is a legalised scam.

You don’t need to teach us about “early termination leads to losses” and neither “the consultant should’ve told you” because the insurance companies were not obliged to explain these details in relation to 3A WITH life insurance products. This has now changed since 1.1.2025

So, YES: the 3A life insurance system IS A SCAM! You’re trying to convince us that it is not, and you’re only right if you apply this to the 3A as such. But please, stop trying to fool us.

And finally, you can tell us which insurance company you’re working for – it is quite clear to everyone reading your posts that you’re one of them. If not, you’re simply very unsavvy and unliterate regarding 3A (and maybe you just want to convince yourself that your 3A WITH life insurance is a good move for you, even if you see/understand that it is not).

In contrast to hiding behind a fake nickname, I’ve openly shared my real name, which can easily be found on LinkedIn and Google. Yes, I work for AXA, and I’ve never tried to hide that. However, my participation in this discussion isn’t about convincing anyone or “fooling” people – it’s about sharing a different perspective based on facts and experience.

It’s clear you’ve had negative experiences, and I don’t dismiss that. But labeling the entire 3a life insurance system as a “legalized scam” disregards the value it can offer in the right circumstances, especially for people who benefit from risk coverage and premium waivers in case of disability.

I also acknowledge that new regulations have improved transparency in the industry, which is a great step forward. That said, I stand by my point: there are advantages and disadvantages to both bank and insurance-based 3a solutions, and their suitability depends entirely on individual priorities and circumstances.

While I’m open to engaging in healthy debates and sharing insights, I’m not going to continue responding to accusations. Let’s keep this discussion respectful and constructive.

I totally agree with her, she is telling facts and Axa is one of the few companies who offer 3rd pillar with no insurances, which is great! Because their Global fund performance and cost is better than those with the banks!

Remember we talk about a PENSION (long term) investment and not an ordinary investment or something of 2 or 3 years!

What about the fees (issue and redemption) in the funds of the banks? They are crazy high! People dont even know of these!

@Dostinja: you seem even more a financial guy who is trying to get some people here follow your thoughts so you can sell them something. 3A as such is good, however you’re not focused on what everybody is saying: 3A with life insurance is a LEGALISED SCAM! So, yes: we should make everyone aware that this is a SCAM, so that nobody suffers huge money losses.

Firstly, I’m a girl 😉—and secondly, I’m just here to share facts, not sell dreams! Let’s keep the debate fun and informative. 🌟

OK, sorry for assuming you were a guy. ;-)

You do work in insurance/finance, do you?

And if you want to keep the debate informative, then please do not share false information/hopes: 3A bound to life insurance is a NO-GO and only a LOSS for anyone. So please, do not tell people otherwise.

My SO lost 41% withdrawing the 3A insurance after having paid into it for 18 months. You DO realise what 41% means, right?