What should you do with a life insurance 3a?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Recently, I have talked about life insurance 3a policies and how bad they were. We have established that they have almost only disadvantages compared to an invested 3a.

So, people should not take out new life insurance 3a. But what should you do if you already have one?

There are a few options about what to do with life insurance 3a. We will explore them all in this article and compare them. By the end of this article, you should know what to do about your life insurance 3a.

Life Insurance 3a

We have already established that life insurance 3a has significant disadvantages:

- Their returns are low.

- Their fees are high.

- They are very inflexible for deposits, locking you into this monthly expense.

- They are very inflexible for withdrawals, making you lose money in taxes.

- They are not transparent.

- They are heavily advertised.

The only advantage they have over an invested 3a (like finpension 3a) is that they have a guaranteed amount of money. However, life insurance 3a only guarantees a 0% interest rate, and the guaranteed amount is less than what you paid. If you want guaranteed 3a, you should take a bank 3a.

Life insurance 3a also has insurance in case of disability and death. This extra insurance may sound like a significant advantage. However, most people will not need insurance. Moreover, you can get pure risk life insurance for a fraction of the fees of life insurance 3a.

If you need more convincing, I have an entire article explaining why nobody should fall into the trap of life insurance 3a.

What to do with existing life insurance 3a?

It is essential to know that life insurance 3a is a terrible instrument. But what should you do if you already have one?

First, you should not feel bad about it. Many people in Switzerland are falling for life insurance 3a. I have a life insurance 3a. I am not proud of it, but I consider it a learning opportunity.

Why did I take out life insurance 3a? An insurance advisor convinced me, and I did not know any better. Most people in Switzerland do not have the necessary financial education to understand how bad these products are. And most people in Switzerland trust advisors, banks, and insurance companies.

Banks, advisors, and insurance companies push these products because life insurance 3a is very lucrative. But life insurance 3a is not lucrative for its users.

We now go to the main question: What should we do with life insurance 3a?

There are three main ways to deal with life insurance 3a:

- Do nothing

- Reduce or stop the payments

- Cease the contract

We will see these three ways in detail in this article.

1. Do nothing

The first and simplest option is to do nothing. You continue contributing your monthly premiums, which stay in your life insurance 3a until your retirement age.

While this option is the simplest, it is also the most costly. Indeed, we have seen that life insurance 3a has abysmal returns and is very expensive. These low returns and high fees result in low performance for life insurance 3a in the long term.

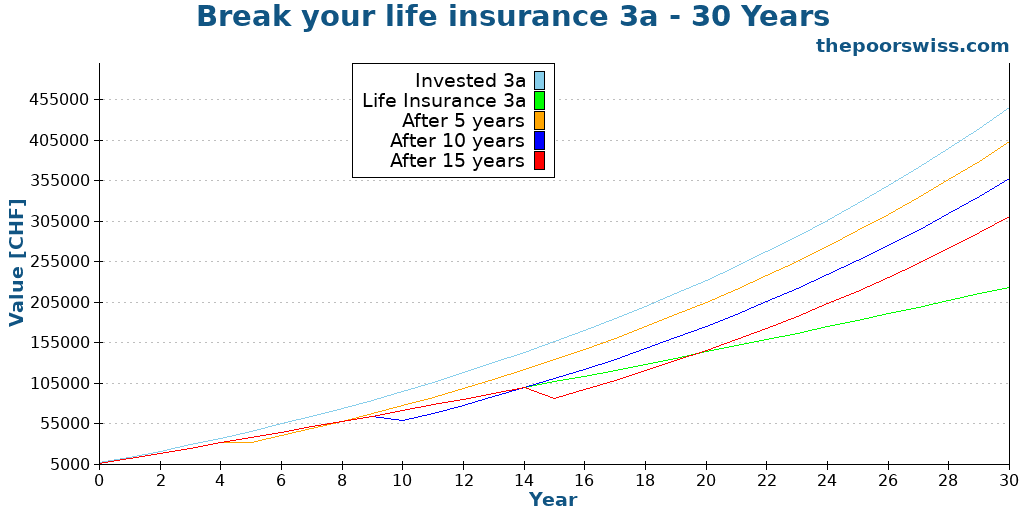

In the previous article, I ran a comparison and got these results after 30 years:

We can see that doing nothing can be extremely costly. Over 30 years, investing in a good 3a could easily yield twice as much money by the time you retire.

Overall, I would strongly advise against doing nothing!

2. Release the premiums

The second option is to stop paying the premiums either fully or partially. Most life insurance 3a allows you to be released from the premiums. Once you release the premiums, you will not have to contribute anymore, and the money will stay with the life insurance until the original policy termination date.

From what I know, all life insurance 3a policies include such a clause in their conditions. So, it is generally not a huge deal to do that.

Here is what would happen to the money by stopping paying the premiums, simulated for 30 years.

We can see that the earlier we stop, the better results we get. It is logical since we get better compounding in the invested 3a, with much better returns. The part invested in the life insurance 3a will continue growing slowly over the years, but you could see it as bonds in your portfolio since this money (minus the fees) is guaranteed.

If you stop the premiums very early, in the first few years of the life insurance 3a, you may incur a penalty. Indeed, in the first few years, the life insurance company takes more in premiums for the risk premiums than in the following years. However, the earlier you stop, the better you will end up in retirement.

This strategy always makes sense unless you are extremely close to retirement. Even a few years without fees could help.

You must remember that the stock market returns are great in the long term but not necessarily in the short term. So, if you are close to retirement, below five years, you could stop the premiums and switch to a bank 3a instead. Or, you could be more conservative, depending on your asset allocation.

It is probably worth mentioning that doing that may prevent you from taking on another life insurance 3a. But that is probably a good thing.

3. Break the contract

The third option is to go a little further and entirely break the contract. With that, you stop paying, and you get back the money from the insurance company.

With this option, you will get back the buyback value. This value is based on the current value minus some cancellation fees. Usually, this value is zero in the first few years of the contract. You have no choice but to transfer this value to another 3a account.

Once again, we can simulate this. I will assume that by canceling the contract, you will lose an extra 20% of the value compared to what you would have in life insurance 3a. This assumption is not precise since, in theory, you would lose more during the first few years and less during the following years. However, this allows us to make a simple simulation.

You may lose more than 20% or less than that based on your life insurance company. Unfortunately, they are not very transparent about these fees.

Here is what would happen if we were to break the contract after 5, 10, and 15 years.

We can see that the penalties can make a significant dent, but the returns of a good 3a easily recover this.

Again, the earlier you break the contract, the better the results will be in retirement. This effect is due to the compounding of the invested 3a.

I should repeat the disclaimer for the previous strategy: if you have only a few years, the stock market’s returns may not be great, depending on the timing. Therefore, breaking your contract a few years before retirement is not a great idea.

This is the strategy we used for our life insurance 3a. We broke the contract and got the money into a proper 3a.

Comparing the three strategy

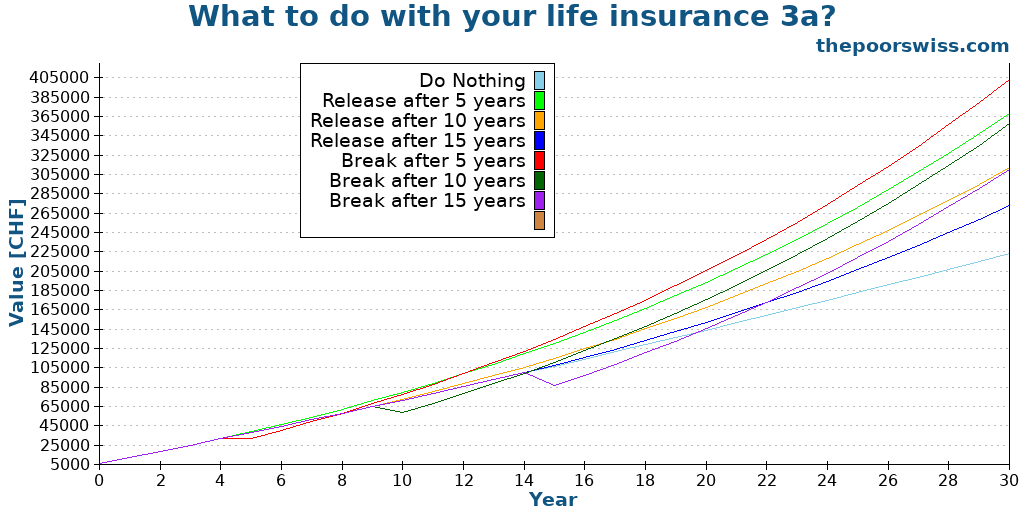

Here are all three strategies together on our graph to summarize them.

The difference between the worst and best strategies is almost 200’000 CHF! Such an amount of money can make a very significant difference in your life in retirement.

Unless you are very close to retirement, you should do something about your life insurance 3a. And doing something means either releasing your premiums or entirely breaking the contract.

The earlier you can do something, the better your returns will be in the long term. And generally, it should only take a few years to recover the loss from breaking the contract.

So, what makes the most sense is to break the contract and move the little money you get back into a good 3a and then invest regularly into that 3a. Releasing the premiums is also an excellent strategy that can make a lot of difference.

Life insurance 3a and mortgage

If you have tied your life insurance 3a with a mortgage for indirect optimization, you may be unable to change your life insurance.

Indeed, if you are using it for indirect amortization, your life insurance 3a policy belongs to the bank. Therefore, you will not be able to make any changes to the contract without changing the mortgage contract.

In these cases, the best option is to wait until the next contractual deadline for your mortgage. Then, you can either switch to direct amortization or use another third pillar for indirect amortization.

Of course, you can also ask your bank to see if there is a quicker way out.

What we did with our life insurance 3a

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

By now, you may know that I also had a life insurance 3a. And if you have read my previous article on life insurance third pillar, you will know that my life insurance policy was really bad.

Early on, I thought I would keep it as a reminder of my error. Then, I was thinking of lowering the premium from 300 CHF per month to 100 CHF since it seemed possible. Since I had to wait a few more years because of my mortgage, I wrote these articles to support my evidence.

At this point, I have realized that my life insurance 3a needs to stop. Before, I did not know it was possible to stop paying the premiums completely.

In December 2025, we told the insurance company (with a letter) that we wanted to break the contract. The letter also included details on where to move the money (Finpension 3a). About a month later, we got the money into our regular 3a. Meanwhile, we also got a call from the advisor asking us if we were sure. It did not take him long to understand I was serious about this.

We have lost a significant amount of money (about 12,000 CHF) by breaking the contract. However, I have no doubt that breaking it now and moving the money to a much better 3a will pay off in the long term. If we had kept it, we would have lost money every year.

Conclusion

If you are trapped with a bad life insurance 3a, I strongly encourage you to do something about it. At least you should learn more about how they deliver very poor returns, have high fees, and are not transparent.

The results of this article show that doing nothing may cost you a lot of money in retirement. Before doing this analysis, I considered doing nothing. However, I have realized I need to break my contract, and as of 2026, we now have no more life insurance 3a.

If you need to find a good 3a after reading this article, you should read about the best third pillars in Switzerland.

What about you? What will you do with your life insurance 3a?

More reading

The truth about 3b pillar accounts

Flexible savings. What is the Pillar 3b? Learn the differences between free and tied pension plans and how to use 3b for early retirement.

Should you take a pension or a lump sum from your second pillar in Switzerland?

The big decision. Annuity or Capital? We analyze whether you should take your Second Pillar as a monthly pension or a lump sum cash withdrawal.

First Pillar: All you need to know to retire in Switzerland

Understand the First Pillar (AVS). Learn how the Swiss state pension works, how much you contribute, and what retirement benefits you can expect.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Dear Baptiste,

I cannot thank you enough for opening my eyes with this article. Thank you, thank you and thank you!

I have had for 7 years!!! a life insurance with SwissLife, following the recommendation of an “independent” financial advisor (putting it between quotation marks in the minimum I can do) who was recommended by a previous boss.

I have been following the evolution of the pillar, knowing that it invested in the market and that assumes some swings. However, I started to pay more attention to it – I have to confess I didn’t do it in the past cause I thought it cannot do it as bad as to offset the tax saving I get, but after reading your article I analyzed it carefully.

With SwissLife, I have made contributions of 51k over these 7 and half years. The savings I have in the pillar to date are 42k (almost 10k are already gone!!!) and the best part is that the surrender value is even lower, 31k!!!! So, 40% of what I have contributed over 7 and half years has simply vanished!!! This is absolutely outstanding and outrageous, so today I have sent the paper to close the insurance, write off painful loses and transfer the remaining funds to Finpension, with the hope it will recover over time.

Thank you for this clarifying article. It is incredible how some independent advisors have so little ethics with their costumers. I have used your code to open my account in Finpension because you well deserve it.

Best regards!

Hi Observer,

Thanks for your kind words and thanks for sharing your story!

The losses on top of the fees can quickly add up as you have seen. I am sorry to hear about your losses, but it’s great that you have decided to stop investing and transfer the money out.

It’s appaling to me that so many people still recommend these products :( The fact that these products are so bas is not well known and people continue to use them.

Hello Observer,

Did you manage to cancel your 3a life insurance with Swiss Life? I am in the same situation, and just realised that now. How did you proceed, what was your answer? I have the Swiss Life Dynamic Elements Duo product from them, and I want to cancel it immediately, but as I have read the conditions, this can only be done if: I reach age 60( not an option, I am 27), buy a property( also not feasible for me), move out of CH, or become self employed. All of these are no options for me. All inputs are welcomed :). Thank you all

Hello I switched mine to fin pension this year. I lost an amount but I feel much safer with my money there rather than a life insurance with Axa where I actually lost money and zero transparency. So I recommend to do as I really don’t trust these life insurance programs.

Hi there!

Thank you so much for this article! I hope I had seen it before. I don’t know if I have a normal 3a pillar combined with a life insurance or a life insurance 3a. I have a product with Swiss Life called Swiss Life Dynamic Elements Portfolio Global Equity. But I have also asked for a life and disability insurance. Am I in the trap completely or only partially? Can I only cancel the life insurance part or should I cancel everything?

Hi Vanessa,

It’s not clear indeed and I think it’s on purpose. For me, it looks like simply a life insurance with an invested portion.

Personally, I would cancel it entirely, but that’s of course up to you.

Hello,

I signed my bad contract with insurance company in December last year. I paid 3000 and today I ask about transfer this money to another provider. The consultant told me that if I will do it now, I will lose almost everything, because of fees! He said that first 3 years is for fees and some other stuff to cover. Is that even possible? Should I ask layer? I don’t know what to do.

Thanks for this article

Hi Alicia,

It’s, unfortunately, entirely possible. Most life insurance contracts have this kind of system where early years are lost to the contractor. No need to ask a lawyer.

If you are convinced this is a bad product, you should cancel it now before you lose more money.

Dear Baptiste,

Thank you so much for researching and offering this information. I wish I had seen it sooner.

I invested all of my 3A to AXA in 2018 40k. Since then I didn’t look at it, invested the max approx 500 per month to that.

Then I had a statement recently that says I have 29000. It makes no sense and when I enquirer they say I have now two 3A pillars with them. I meet them mid April to discuss but I’m worried if I move it I loose a lot. Is there a right time to move / stop payments?

I’ve also lost my job so I had to stop paying but this is seen as a ‘vacation’.

So any advice on how I could proceed would be more than welcome.

With kind regards

Z

The most important thing is not to start paying again into the life insurance.

It may say that you can withdraw 29’000 CHF. It does not mean everything else is lost.

If you want to cancel it, the earlier the better because it will get better returns in another account.

But it will depend on your investment horizon and your entire asset allocation.

Man thank you so much for your article. Helps heaps.

I signed a really shiitty life insurance linked to my third pillar with Allianz. Anytime I ask for clarifications on what are the fees, what is in it, how is the performance of the invested part I get no answer or really vague ones. I started digging in and realised I got pretty much scammed by Allianz.

Everything I have put in my 3rd pillar in the first 2,5 years was to pay the life insurance and only recently did I start to add to the fund in my 3rd pilar.

On top of that, I use it for my direct amortisation for the house.

I have now decided to release the 3rd pilar from my bank. I will have to put 13k in cash to my bank to compensate for the indirect amortisation and whatever is in my 3rd pillar will go to Viac.

I will have lost quite a bit but in the long run it will have been worth it and this way I will be in total control of my money.

Whatever financial decision allows me to sleep best at night is the best one for me.

Hi James,

Thanks for sharing your story! And congratulations on moving out of this bad asset. It sucks in the short term, but you will be happy in the long term.

It seems you are in the same situation as mine, where the bad 3a is tied to the mortgage. I have to wait a few more years to stop the indirect amortization. Did the bank push back of switching to direct amortization?

Hi Baptiste,

Thank you so much for all your work on this blog. It’s always a great read and I’m learning a lot from it, especially while being young.

I was one of those who, unblinkingly better, signed a contract with an Insurance 3A (PAX). Thankfully because I started very early (mid 20s) and only been putting little money there (300/month), I have little to lose. I was offered to simply move the contract to a 3B pillar and stop paying and this wasn’t really mentioned in your article (mostly because I don’t even have 3y in the contract yet, not everyone’s case).

Do you see anything sketchy with that approach?

I have < 10k deposited in the 3A so far. I could as well take the money of from the 3B, but I don't think it's worth to be taxed on it right now (if I got it right).

Many thanks and take care!

Italo

Hi Italo,

The most important with so few years is indeed to stop paying. However, you should know that this money in a life insurance 3b will have an opportunity cost compared to have it invested properly. So, it could make more sense in a proper 3a like Finpension 3a.

I am not sure how exactly this plays out since you should be able to withdraw money out of 3b, but not 3a without conditions.

What makes the most sense mathematically is to stop paying and transfer the money to a good 3a and keep it invest for the next 30 years. But again, the most important is that you stop paying it!

Hi, thanks for the great articles. Last year I started a 3a life insurance with monthly contributions and also deposited a lump sum in True wealth. Through this years downturn my True Wealth has lost 13% but my 3a 31%. Considering my 3a is a monthly deposit, this is a disaster of an investment. With the downturn and penalty, I will lose over 50% in total when I close the 3a. At least I’ve only paid in for a year and a half👍

Hi Robert,

Be careful about doing any conclusions on such short term. But 31% in a year is very high. In the current bear market, the world stock exchange did not lose money than 28% from top to bottom, so I don’t know how they can lose so much. Since you have only one year, it’s a great time to quit!

It sucks, but you will make it up in the long term.

Hi Baptiste

Thanks so much for your article, I have been reading a lot on your blog this last year and have learned a lot.

But that I started a Life Insurance 3a a few years ago bothered me since I learned how bad they were. I always thought it would be a bad deal to cancel it, but turns out I could transfer it to finpension without any fees or penalty.

Hi,

How could you transfer it without penalty? Usually, a part would be lost in the transfer when breaking the life insurance contract.

I was surprised as well and I’m not really sure why. I think there with my contract I only would have paid in the first two years. Or maybe there are some hidden fees I did not notice.

I just checked and I defiantly lost a good part of the money I paid because the “Rückkaufwert” is less than what I paid. But they did not also have any other penalty or fees.

That’s what I was calling a penalty :)

Normally, there is no extra penalty, but a large part goes to the risk premiums, especially in the early years.

Hi there! Thanks so much for this article :)

I have a question: i’ve always heard that you should have multiple (5 I think) 3rd pillar accounts with a certain max amount, so that you can take the amount out over some years and avoid paying too much in taxes. Is this true and still relevant? Maybe you already did an article on that and I missed it, but I’m really wondering where I should put the money of my insurance 3a (you’ve totally convinced me haha)

Have a great day!

Hi Nat,

You are correct and it’s still relevant. I am talking about it on my article about the third pillar.

You will probably have to transfer your life insurance 3a (well done!) to a single account. But you can create a new account just for that. If you don’t know which one to use, I have an article about the best third pillar.

Thanks so much for your answer! I will look into it, since I already have two 3rd pillars in banks (one invested, one not because it’s linked to my mortgage) and I live in Vaud.

I have made the request to transfer my insurance (yay!), let’s see how much I will actually get since I’m in the first 5 years haha

Have a nice day!

Well done! I hope you won’t lose too much, but you should make that up with future returns!

Hi,

Great article, as always. I’m in a similar situation as you where my Swiss Life 3a is linked to my mortgage with Credit Agricole. The solution I found is the following:

– break the contract with Swiss life at no cost.

-open a 3a bank account with Credit agricole for indirect amortization of my mortgage (around 4000chf per year). It cannot be invested but it has a 0,25% interest rate. Not much, but this will allow me to keep benefiting from the tax benefits of indirect amortization.

-add 2880 chf to a finpension 3a and invest it.

Do you think this is better than just switching to direct amortization and investing everything in a 3a with finpension?

Thanks

Hi Justin,

I do not know whether that’s better, I have not run all the math on that yet.

Bear in mind that the difference between 0.25% per year and 5%-6% is huge. Whether that’s better than indirect amortization will depend on how much taxes you pay and how much interest you pay and such.