VIAC 3a Review 2026 – Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

There are many third pillar providers in Switzerland. Some are good, but most are too expensive. You do not want to waste your retirement bank on fees. Therefore, you need to choose the best third pillar provider.

In 2018, VIAC started in the market of third pillars. VIAC is the first mobile third pillar. And they are really interesting! VIAC has very low fees and lets you invest up to 99% exposure in stocks. It is significantly better than what I have found before in other third-pillar providers.

In this article, I do an in-depth review of VIAC! Among other things, we will look at this service’s investing strategies and fees.

| Total Fee | 0.41% per year |

|---|---|

| Maximum portfolios | 5 |

| Stock allocation | Up to 99% |

| Maximum foreign exposure | 99% |

| Maximum investment in cash | 100% |

| Investment Strategy | Index funds |

| Fund providers | Credit Suisse and Swisscanto |

| Languages | English, French, German, and Italian |

| Sustainable option | Yes |

| Mobile Application | Yes |

| Web Application | Yes |

| Custodian Bank | WIR |

| Established | 2018 |

| Foundation’s domicile | Basel |

VIAC

VIAC is a recent actor in the third pillar area. It was launched in 2018 and is becoming increasingly popular.

It is pretty new compared to other big banks. It is essential to mention that VIAC is not a bank. The money you have with them is stored in the WIR bank. As such, you will have complete protection up to 100,000 CHF, like the other banks. This protection is critical. Without that, I would not consider this provider at all. You want your money to have maximum protection.

VIAC is quite different from the other providers. You will only have access through a mobile application or web application. They do not have offices where you can do operations with them. This absence of bank offices is what makes them offer very low fees.

They started with only a mobile application. But since then, VIAC has added support for a web application. The web application is great for people like me who are not fond of mobile phones. Most people will probably like mobile applications since they are fond of phones.

To learn more about VIAC, you can read my Interview of Daniel Peter, CEO of VIAC.

So, we will see how good VIAC is as a third pillar in Switzerland.

Investing Strategies

For long-term investors, the investing strategy of a third pillar is essential.

VIAC offers three sets of strategies:

- Global: Investing in the entire world.

- Switzerland: Investing in Switzerland

- Global Sustainable: Investing in the whole world but omitting some stocks, such as tobacco or weapons stocks. This is called sustainable investing.

Each strategy has five variants: 20, 40, 60, 80, and 100. These variants specify the allocation to stocks.

You can also define your strategy by composing it with their different underlying funds. This customization is an excellent way to choose exactly what you want to invest in. But then, you need to have a good idea of how to create a custom portfolio. I would not recommend this to a starter investor.

The fact that we can go up to 100% invested is great! For a long-term aggressive investor, this is ideal. They are investing only 99% since they keep 1% in cash in each portfolio. But 99% is already a great amount invested in stocks.

Interestingly, they allow you to invest in either cash or bonds if you do not fully invest in stocks. This is great for people who do not think bonds will overperform cash.

You can also have several portfolios, up to five. Having five accounts is great for optimizing taxes by making staggered withdrawals.

VIAC Global 100 Fund

The most interesting strategy is the VIAC Global 100 strategy, which I chose for my VIAC account when I used it.

This fund invests 99% in stocks. Out of these stocks, 40% are Swiss stocks. Each default portfolio is limited to 60% in foreign currency exposure. You can lift this limit by doing a custom portfolio with 99% in foreign exposure. However, the default portfolio uses Swiss stocks for 40%. The rest is invested in the entire world based on market-cap weight. The remaining 1% is allocated to cash.

This strategy’s TER is 0.45%, and there are no other fees, making it a very cheap solution for Switzerland!

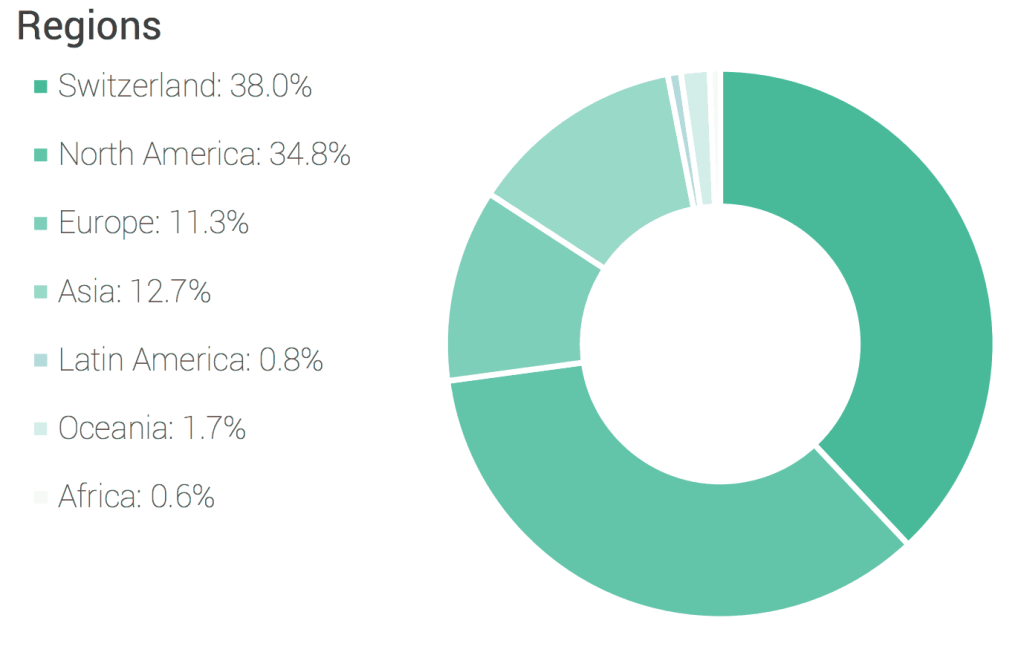

Here is the allocation by region of the Global 100 fund:

And there is the exact allocation of each sub-fund (as of September 2018):

- SMI (Swiss): 27.75%

- SPI Extra (Swiss): 9.25%

- Europe ex-CH: 10.60%

- S&P 500: 31.51%

- Canada: 1.93%

- Pacific ex-Japan: 2.54%

- Japan: 4.46%

- Emerging Markets: 8.96

- Cash: 3.00%

This offer is great. It is better than most other candidates:

- The allocation to stocks is high

- The allocation to international stocks is the maximum permitted by their regulations.

In the long term, this nice allocation to stocks and the relatively low fees will result in significantly more returns.

VIAC Fees

When investing long-term, it is important to look at the fees.

The base fee of VIAC is 0.52% per year. But you only pay this fee on the invested part (the stocks). So, if you have more cash, you get fewer fees.

In 2021, VIAC introduced a fee cap on its administration fee. So, you cannot end up with more than a 0.40% administration fee. If your strategy has a higher fee, it is reduced to 0.40%.

Now, some strategies also have product costs. These products can make the strategy more expensive than 0.40%; only VIAC’s administration fee is capped.

The fees at VIAC are different for each universe and strategy. For instance, here are the fees for the global strategies:

- Global 20: 0.17% per year

- Global 40: 0.28% per year

- Global 60: 0.39% per year

- Global 80: 0.41% per year

- Global 100: 0.41% per year

Fees for Switzerland strategies are slightly higher:

- Switzerland 20: 0.17% per year

- Switzerland 40: 0.28% per year

- Switzerland 60: 0.39% per year

- Switzerland 80: 0.42% per year

- Switzerland 100: 0.43% per year

And the sustainable strategies are the most expensive:

- Global Sustainable 20: 0.16% per year

- Global Sustainable 40: 0.28% per year

- Global Sustainable 60: 0.39% per year

- Global Sustainable 80: 0.43% per year

- Global Sustainable 100: 0.44% per year

Overall, these are excellent fees! Compared to most offers in Switzerland, this is better!

Other features

VIAC has several features that differentiate it from other third-pillar providers.

Indeed, with VIAC, you can get life or disability insurance. With each 10,000 CHF invested in your account (only the invested part counts), you get 2,500 CHF insurance.

You have to choose in your account whether you want disability insurance (in case of at least 70% disability) or life insurance. In the case of life insurance, this will be paid to your beneficiaries with the money from your third pillar. In case of disability, you will get the insurance payment directly from yourself.

It is a nice bonus, but this is not life-changing. This will only be useful if you die or get disabled (and you have to pick) before your retirement age. And the amount is still quite limited, so, for many people, this will not replace proper life or disability insurance. But this could still be very useful. And since it is free, it is not a bad deal for VIAC users.

Another extra feature is that VIAC has a partnership with WIR to provide mortgages. The interesting point is that you can use your VIAC 3a as indirect amortization, and that you can even pledge it.

Sustainability of VIAC

More and more people are interested in investing sustainably. They want their money to work for a better future and not invest in companies that are not sustainable for our world. But does VIAC offer a sustainable option?

When you choose the sustainable option, VIAC will invest in different funds. It will invest in two different types of funds:

- Socially Responsible Investing (SRI) funds.

- Environmental Social Governance (ESG) funds.

These two kinds of funds are very similar. They select companies based on sustainable factors. For instance, they will not invest in companies that make weapons or in companies that exploit children.

While this sounds good in theory, there are many issues with these funds. For instance, it was shown that about 80% of sustainable funds had exposure to fossil fuel companies. These companies are the antithesis of sustainable investing.

Also, the criteria for selecting companies in these funds are not very transparent or even agreed upon between different funds.

Finally, these funds are not very selective. Indeed, it was shown that nearly 90% of the companies in the S&P500 are present in ESG funds. So, very few companies are excluded.

Regarding VIAC, these options are likely more sustainable than the default options. However, this sustainable option is not very sustainable. I would not call this greenwashing, but this is level zero of sustainable investing. The only advantage is that this is simple and cheap.

So, I would not say sustainable investing is very sustainable, but it is better than nothing.

Security

We can also look at the security of the VIAC third pillar.

The applications’ technical security (web and mobile) is pretty good. All communications are encrypted between the application and the server. And since you cannot do anything with your third pillar until you retire (or in a few other special cases), the apps are well protected.

The only thing I would like is a proper second factor of authentication on the web application. But again, since you cannot do much, it is unimportant.

If you hold cash, it will be held by WIR Bank, the custodian bank of VIAC. This cash will be privileged in case of bankruptcy up to 100,000 CHF. This protection is the same as the bankruptcy protection of other Swiss banks. If you are an aggressive investor, this should not matter much since you should have very little cash.

The securities themselves are invested in institutional funds. These funds are very stable and are held in your name. The funds are not directly on the balance sheet of VIAC but on the balance sheet of the foundation. So, if VIAC goes bankrupt, these funds are safe in the foundation. It will be up to the foundation to find a new manager for these funds and to get you access to this money again.

Finally, I have never heard of any data leak that would have occurred at VIAC. This is always a good sign, even for recent companies.

Overall, I think that VIAC’s security is quite good and well-regulated. The applications are well-made, and the foundation is organized, so your assets are well-protected.

Alternatives

In Switzerland, there are many alternatives.

Compared to third pillar accounts from banks, VIAC is a great third pillar, much better than anything a bank proposes.

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

However, compared to other independent third pillar providers, VIAC is not the best available. Finpension 3a is currently the best third pillar available. Finpension 3a has several advantages over VIAC:

- The fees are slightly lower.

- You have more freedom in designing your portfolio.

To learn more, read my detailed comparison of VIAC and Finpension 3a.

VIAC FAQ

Is VIAC regulated?

Yes, VIAC is regulated in Switzerland as a third pillar foundation.

Is VIAC safe?

VIAC is well regulated and assets of the investors are fully segregated from the main entity. In case of bankruptcy, the foundation would have to find an alternative manager but investor funds would be safe.

How much fees will I pay with VIAC?

VIAC has an administration fee of 0.52% per year (currently capped at 0.44%). On top of that, you also currency exchange fees, at around 0.05%.

Who is VIAC 3a good for?

The VIAC third pillar is a good third pillar for conservative people or people that do not have a very long term horizon.

Who is VIAC 3a not good for?

VIAC 3a is not the best for aggressive investors, with a long term horizon. Indeed, you can invest more aggressively with some alternatives.

VIAC Summary

VIAC is a good third pillar, with good fees. It is a great third pillar for conservative investors.

Product Brand: VIAC

4

VIAC Pros

Let's summarize the main advantages of VIAC:

- You can allocate up to 99% in Stocks

- Very low fees

- VIAC is very transparent

- A small interest rate on the cash part

- Strategies with low allocation to stocks are cheaper

- Mobile and web applications

- 99% can be invested in foreign currency

VIAC Cons

Let's summarize the main disadvantages of VIAC:

- Not the cheapest third pillar

Conclusion

The conclusion is pretty simple! VIAC is an excellent third pillar provider in Switzerland. The fees are very low, and VIAC offers a high stock allocation. These facts are great for long-term investors. And since most third pillar investors are in for the long-term, this is excellent.

I also like VIAC’s transparency. They communicate well and share as much information as possible. VIAC is the best third-pillar provider for this information. It is also very clean and modern. They do not try to hide fees, and they have been quite helpful in answering my questions for this article.

When VIAC was introduced, they were the best third pillar available. Now, there are other competitors. If you want to keep up to date, I have an article about the best third pillars in Switzerland. I moved my third pillar from VIAC to Finpension 3a, but both are great options.

If you like VIAC, you may like other services from VIAC:

- VIAC’s vested benefits

- VIAC Invest, their new robo-advisor

Which third pillar do you use? What do you think of VIAC?

More reading

Pilla 3a Review 2026 – Pros & Cons

Pilla 3a is a new digital third pillar account proposed by CA next bank and the Liberty Foundation. Is it good? We review it in detail.

Yuh 3a Review 2026 – Pros & Cons

Yuh 3a. Read our review of the Yuh 3a pillar. We analyze the 0.50% fee, the investment strategy, and how it compares to VIAC and Finpension.

Frankly 3a Review 2026: Pros & Cons

Frankly Review. We analyze ZKB's 3a app, its fees, and investment strategies to see if it competes with VIAC and Finpension.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi poor Swiss thanks always for your great articles and rich information.

You mention here that the VIAC total fees is 0.45% but when I looked at their global 100 portfolio the total cost is 0.41% which is not so much more vs finpension at 0.39% or I am I missreading the VIAC total cost? Thanks for your feedback on this.

That’s weird because if I open the factsheets, it states a 0.45% fee. I don’t know where the 0.41% comes from. I will have to look into it.

Thanks for letting me know!

Great blog, exhaustive and clear! I always follow your useful advice, last by subscribing to VIAC!

Hey Mr. TPS,

I’ve been following your blog for the last year, terrific work you are doing out there :)

A couple of weeks ago VIAC mentioned that they will now move to a weekly rebalancing. I have 5 portfolios with equally split amounts as standing orders. What do you think from a risk management perspective: does it make sense to further split those recurring payments from a monthly base to a weekly one in order to benefit from market fluctuations even more?

Thank you for your time and keep up the amazing work!

Hi Filip,

For me, the weekly rebalancing is good but not a game-changer. The main advantage is that your money gets invested faster when you send money to your account, at most one week instead of at most one month. So, your money is in the market longer.

But I would not recommend weekly investing, no. It’s just too much trouble. Invest money when you have it and it will be fine :) I invest money once a month, just after my salary and I don’t do anything else for my investments for the entire month. And for my 3a, I actually max it in January as soon as possible.

Now, if you get paid once a week, it could be interesting, but I do not even think this would be worth the trouble.

Great blog! Love it. Clear and exhaustive. Thanks for sharing all this useful info.

Thanks for the great review! I just signed up for VIAC and this is my first step in investing! The next step is to set up an account in DEGIRO and start investing in global ETF.

Still loving VIAC, great returns so far.

Hey i have seen different options of 3th pillar, definitely the ones that has an insurance include are the worst ones.

For you which is the best one with less fees more % per year.

thanks

Mia

Hi mia,

Generally, life insurance third pillars are strictly worse than “bank” alternatives.

For the best option, you can read my article about the best third pillars.

I also recommend VIAC, and they also lowered their fees this week.

Hi,

It seems VIAC decreased the fees retroactively from 1st of March.

Thank you poor Swiss for this blog!

Bye,

F.

Yes, they just decreased several of their fees now that they reached one billion of assets under management! This is great news!

I still have to update all my articles about VIAC to reflect that.

I can also highly recommend VIAC as it is possible to open multiple portfolios with different strategies and a large equity exposure.