How to track expenses in Switzerland?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I strongly believe that tracking expenses is one of the important parts of personal finance, at least when you try to improve your finances. Having an accurate view of all your expenses in the same place gives you a real sense of how much you are spending.

Once you have this accurate view of your expenses, you can take action to improve your finances if this is necessary. You can also observe some trends and avoid issues.

In this article, we discuss how to track expenses, especially in Switzerland.

Tracking vs budgeting

For me, tracking expenses is much more essential than budgeting itself. Tracking expenses simply means knowing how much we spent in a given month (or another timeframe). Whether you put these expenses in different categories or not only matters to you. Budgeting means assigning limits to each category of your expenses. But once you have tracked all your expenses, it should be easy to know where you can improve.

But many people think is it is too time-consuming to track all their expenses. There are some ways to make it easier and more accurate.

Application for tracking

We should start at the beginning. Where should you track your expenses? There is no right or wrong answer here. What matters is that the tool you are using works for you. Overall, I think you should not pay for a budgeting app. There are many free apps and alternatives.

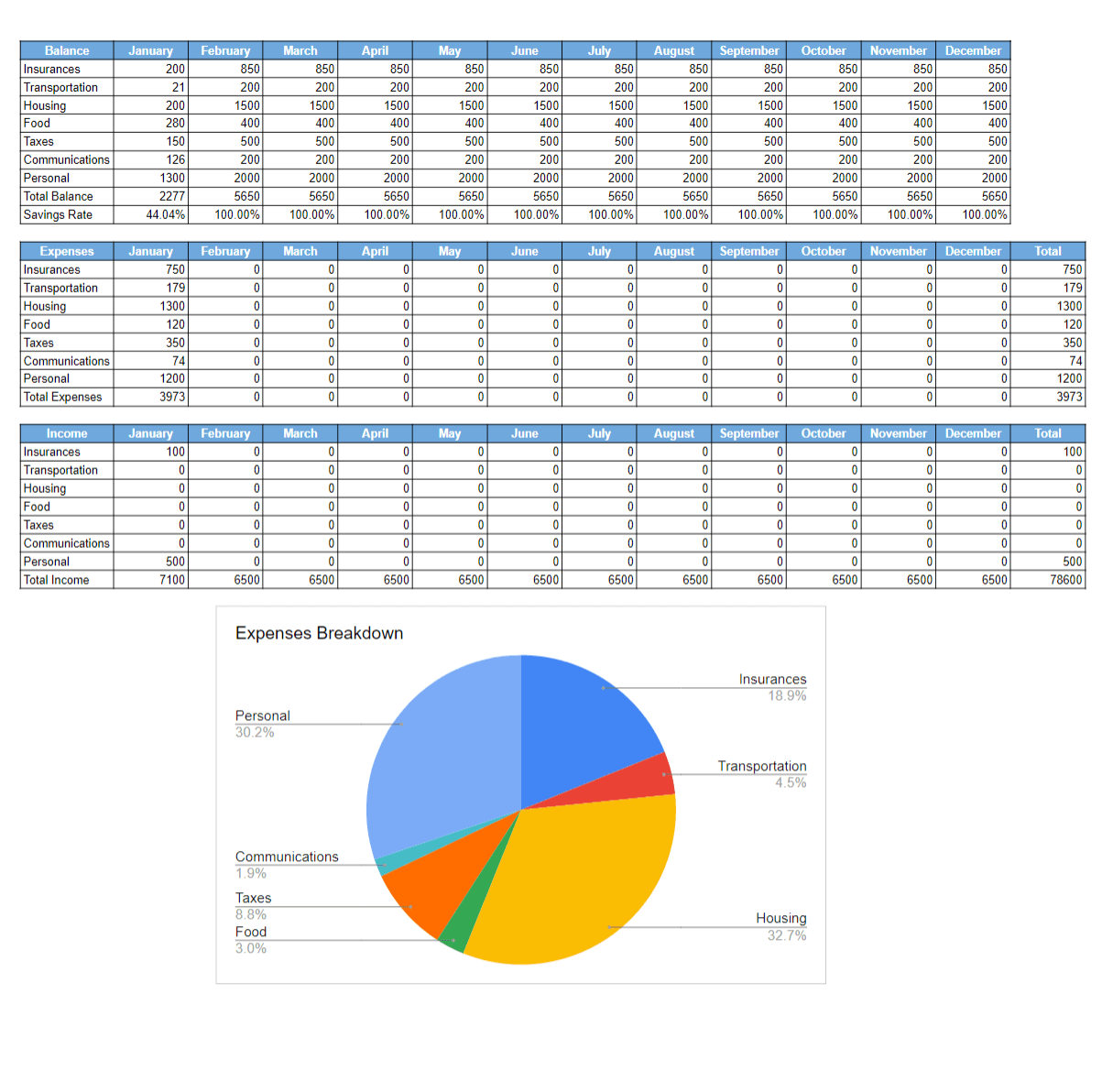

A simple Google Sheets template to start tracking your expenses and earnings and have an overview of your budget! Know your savings rate without effort!

When you are starting to track your expenses, the simplest way to start is to use a spreadsheet. And you do not have to pay for Microsoft Office, because there are some free open-source alternatives. So, you can use LibreOffice or OnlyOffice, for instance. But if you prefer, you can totally use Excel or Numbers or put the spreadsheet on Google Sheets.

You only need a spreadsheet editor. Most people can get started by themselves, but if you do not know where to start, you can check out our simple spreadsheet or our advanced spreadsheet.

The advantage of these spreadsheets is that they are simple to get started with, but they still allow a lot of customization. And you can add advanced features as well.

Additionally, there are many budgeting apps available. I do not have a real recommendation here. I would recommend avoiding paid apps since there are many free apps available. I built my own for my needs (budget warrior), but it is difficult to install. Recently, I have heard some good things about MoneyManager Ex, but never tried it myself. One feature that can be very useful is to be able to import your expenses through CSV. We will see later that this is the favored file format for expenses.

And finally, you can also do it on paper. This is probably what takes the most time of all the techniques. And you have to be more careful about how you store your paper notes. But it works well and forces you to do a little math, which is good for the brain.

I started with an Excel sheet on my computer. Then, I migrated to Google Sheets. And finally, I wrote my own application and have been using it for about 13 years now.

Tracking card expenses

When you buy something with your debit card or credit card, it will be recorded in an application. This makes it easy to then record into your budget application because you cannot forget it.

There are two strategies to keep track of these expenses. Some people copy expenses from their card applications into their budget application very often (daily, often). This means they have to spend a little time with their budget every day. And some other people prefer to do it only once a month. In this case, you spend more time, but only once a month.

The strategy you choose should work for you. I do not think any of these two strategies has any significant advantage over the others. Personally, I prefer to do it once a month.

How long you will spend with your importing will depend on two factors:

- How fast you are to enter data into your budget application.

- How many expenses do you make per month.

So, if you want to save time, you can either spend less often or learn to use your application faster.

Automatically import expenses

A great Swiss credit card with excellent cashback (up to 1%!), very flexible, and with a good mobile application.

- No yearly fee

- 1% cashback in three shops

If you would like to save more time, you should try to automatically import expenses into your budget application.

Unfortunately, in Switzerland, we are far behind many other countries in terms of exporting and importing data from banking applications. In the US, for instance, there are tools that will automatically connect to your bank account and extract all expenses and put them into a budget. In Switzerland, we are stuck with older tech.

The only thing you can do to automate your expenses is to go through CSV files. A CSV file is a comma-separated-value file. It is an old file format to represent tables from spreadsheets. It works really well for expenses.

First, you must check whether your budget application can import expenses from CSV. If it cannot, there is not much you can do. You can ask the authors of the application to add this feature. Or you can switch to another application. If you are using any spreadsheet application, it should be fairly easy to import CSV data (copy into a new sheet, rearrange, and copy into the expense sheet).

Then, the main problem arises. You also need to check whether you can export data from where you are spending. And this is where it can begin to be complicated because not all applications are equal. You can almost always get a PDF statement, but not always a CSV statement.

Our primary bank, Migros Bank, lets you generate CSV statements for the transactions of a given period. However, most people use a credit card to spend (to get cashback). My favorite credit card is the Certo One card by Cembra. This card is great, and we can export CSV transactions from the web app!

I also sometimes use TWINT which does not support it.

If you are lucky, both your bank and your credit card let you generate CSV statements. If you are not, only one of them lets you do this. So, in this case, you will have to choose between convenience and cashback.

If you only have PDF statements, there is still something you can do. There are some online services that let you convert a PDF statement into a CSV table. However, this will still require you to clean up the output CSV. It is not difficult, but it is still multiple extra steps. And some statements will work better than others.

For instance, I used Zamzar to convert PDF statements from Cembra to CSV in the past. I then have to remove some lines from the file and merge multiple tables to then be able to import it. You can also use AI for this. I have used ChatGPT, and at least the latest ChatGPT 4o model did not have any issues transforming the PDF to a single CSV file. In the past, it did not work so much, but this was on an older and smaller model.

This is an area where the Swiss banking system still needs to do a lot to make it easier for people to track their expenses.

Why not use your bank application to track?

All the services you need to pay, save and invest, in a neat package, with extremely good prices!

Use code tpsummer to get one year of Neon Plus and your debit card for free!

- Invest with great fees

Many of the recent digital banks give you some reports on your expenses and let you categorize expenses into categories. For instance, with Neon, you can see your incoming and outgoing transactions and put them in different categories. You then have some limited reporting on where your money is going.

So, why not use this application directly? The main reason is that most people spend money in different form:

- Debit card

- Credit card

- Cash

- TWINT

- And possibly others

Since each app only has the knowledge about its own transactions, it does not make sense to use your banking application as a budget tracker. Another reason is that expense tracker applications are better at doing this than banks. There is a trend that bank applications try to do everything. But I strongly believe that no bank can do it all. A bank application should do banking only. I do not believe in the myth of the super app or universal bank. One bank cannot be great at everything.

Therefore, unless you strictly only use one mean of payment, using your banking application for tracking your expenses is not possible or interesting.

Tracking cash expenses

Cash expenses are probably the most complicated to track. Indeed, if you buy something in cash, it is easy to forget about it and never track it.

There are a few strategies on how to improve that so that your tracking is better. The first strategy is obvious: avoid cash payments. Everything you do on a credit card or debit card will be recorded by the app, and you do not need to remember it. Of course, some people are against card payments and is there is the issue that they are pricier for the stops (which ultimately makes them more expensive for customers).

Another strategy is to make sure you keep the receipts on you for each cash payment. Once you go home, you either note down the expenses or save the receipts for later. If you do not get a receipt, you can write it down on a small notepad you could carry on you at all time. And again, at the end of the day, you either store your note or write down the expense in your system.

The last strategy is quite different. If you would rather not keep track of each cash payment, you can consider that all cash withdrawn is spent. So, if you withdraw 200 CHF in cash, you can write down the expense as 200 CHF directly. This is less accurate because you do not know exactly how you will spend it. But you know this amount has left your bank account, and you are going to spend it. This is the simplest of the 3 strategies but will not accurately represent your expenses. On the other hand, this is simple and will accurately represent what leaves your account.

I also struggle with cash payments. And I use a mix of the three strategies. I try to avoid cash payments as much as possible. Then, if possible, I keep the receipts for later. And in some cases, for instance when going to a small market, I simply write down the total cash as one expense because in a small market you can only pay cash, and you do not get receipts.

What to do with the data?

Now that you have collected all this data about your expenses, what should you do about it? Data is good, but it is still useless if you do not make something out of it.

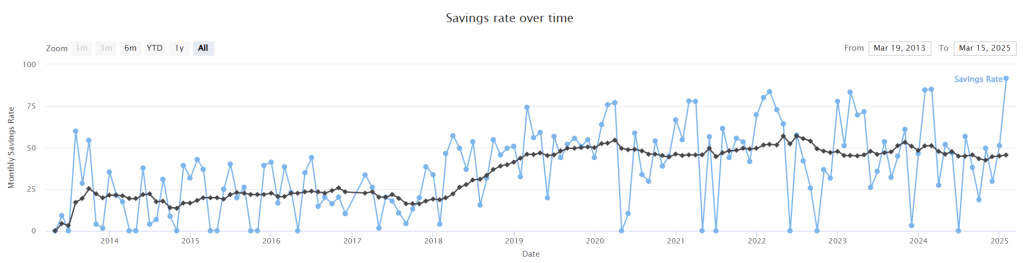

The first thing I recommend you do is compute your savings rate. Your savings rate is simply your net income divided by your savings (your net income minus your expenses). This important financial metric tells you how much of your income you are saving. It is a good metric to try to increase. When you are starting to improve your personal finances, lowering your expenses can have a very significant impact on your savings rate.

Then, you can look at trends in your expenses. By trends, I mean how you your finances are evolving? Are you spending more or less each month? Which category is improving or getting worse? These questions will help you figure out how to improve your expenses.

Of course, the best thing you can do with expenses is to reduce them. If you can spend less (without detriment to your quality of life, ideally), it will help your finances. If you do not know where to get started, you can check out my best tips to save money in Switzerland.

For many people, tracking expenses and having a global view over what they spend is enough. For others, it is necessary to set a budget. There are multiple strategies, and they do not work for everybody. But if you do not know where to get started, you can check the main budgeting methods and choose the one that fits you best.

Conclusion

As of writing this article, I have been tracking my expenses accurately for about 13 years. As a result, I now have a wealth of data to see where my expenses are going and see how I can improve them. I believe tracking my expenses has been one of the important factors in how I significantly improved my finances over the last decade.

If you are not yet tracking your expenses and struggle with your finances, I strongly encourage you to start tracking your expenses today.

How about you? How do you track your expenses?

More reading

The 13 Steps of My Monthly Personal Finance Routine

Take control of your finances. Discover my monthly personal finance routine to track expenses, pay bills, and ensure your savings goals are on track.

How to set goals to improve your life

If you want to succeed in your life, it is very important to set yourself goals to reach. Find out how you can set good goals with this guide!

Cars are not always bad for finance

Are cars really money pits? I argue why owning a car in Switzerland is not always a financial mistake and how to minimize the costs of driving.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Excellent comprehensive guide on expense tracking! I’m curious about your experience with the Swiss banking limitations you mentioned. Have you found any workarounds for automatically syncing TWINT transactions, and do you think Swiss banks will improve their CSV export capabilities soon?

Hi Neva,

No, I have found no workaround for TWINT. For us, it’s not a huge deal because we don’t use it much. But for many people, it may be a big issue since they use it in priority. My biggest issue is the PDF from Cembra, which I have to convert through either ChatGPT or Zamzar before I can import in my tracking tool. This is where we do the bulk of our expenses.

Unfortunately, I am not sure Swiss banks will improve, they are very slow at doing that and I do not think there is much push in that direction.

Hi,

I have been using YNAB for several years now and it was a true blessing. The approach with envelope budgeting and the ease of use of the app changed everything for my budget and my finances and I will remain grateful to them.

That being said, the steep price increase over the past years has been really annoying, especially given the lack of innovation – but none of the alternatives I tried was satisfactory.

Until I found Actual Budget (actualbudget.org): this is an open-source application, that can be deployed easily for much less than YNAB, but that can even be self-hosted for free (this is not for everyone but not utterly complex if you’re a bit tech-savvy). It supports both envelope budgeting and budget tracking, it is very close to YNAB in terms of ease of use, the mobile web interface is also quite nice.

I switched 2 months ago and cancelled my YNAB subscription and I don’t miss it. The YNAB tutorials and Youtube channels on how to budget remain valid and worth following for people new to budgeting and expense tracking, but as for the app, I can only recommend Actual Budget, it works well and fit all my needs.

Gosh, re-reading it, it sounds like spam :-) sorry for this.

I am not affiliated with ActualBudget (or YNAB), but I admit I am quite happy I found a decent replacement to YNAB, it took an long while with lot of false hope…

I did the same recently! 🖖 but I am still finding out how to use it.

Are you happy with YNAB so far?

As I said, I was except with the price, hence the switch to ActualBudget. And yes, I’m still quite happy with it.

Thanks for sharing!

This is typically the kind of task I’m going to try to get an AI to do for me – I use almost no cash, so I can probably feed it my card and bank statements, sort out guidelines for what to categorise where, and have the results go into a spreadsheet or some kind of dashboard. Will probably require some work but I think it’s a good use case!

I’ve tried to give to Claude the PDF of my bank statement and asked it to analyse and extract a CSV. My bank doesn’t offer the export to CSV functionality with the free account.

I can feel its pain while analysing the file but eventually it can make it. I can then use the CSV in my custom tracking app

It’s good to know that Claude can do it. Did you have to tune the prompt to get a good result?

I got prompted (!) by your comment and asked ChatGPT again with the latest model and it worked really well this time!

Hi Stephanie

That’s definitely a good use case. I actually asked ChatGPT to extract the data from the PDF from Certo but it failed miserably the first time I tried. I should try again with the most recent models.

For the people who use the Swisscard Cashback cards in the app there’s a hidden functionality to filter and export the expenses in Excel or CSV. You can find it under the “menu” (bottom right corner) and then app.swisscard.ch

Thanks a lot for sharing this trick, this can be very useful!

Hello, is there a typo in this phrase

“Your savings rate is simply your net income dividend by your savings”?

I guess you meant “divided by”…

Or maybe it’s a way of saying the opposite of “savings / net income”?

I guess this is a better definition of saving rate.

Thanks, Maurizio. It’s indeed meant to be divided and not dividend :) I will fix it.

J’ai entendu du bien de Finary ou YNAB, mais pas envie de payer pour ça. Mon excel est à la fois trop simple et trop compliqué, il faut que je change.

J’avais regardé pocketsmith qui me semblait prometteur.

https://pocketsmith.com/

Thanks for sharing, JPO. I had never heard of PocketSmith before. It does look good.

P.S. Please comment in English, on English articles (or in French on French articles).

I have been tracking all my expenses since I was a student, as I needed to keep an eye on my finances. This practice has been a very helpful tool for self-discipline, and I continue to do it today.

I use LibreOffice with a simple spreadsheet I created back then, which has almost the same naming conventions today. I also tried to integrate it into the accounting tool I use for my company, cashCTRL, since it’s intuitive and easy to use. However, it takes a lot of time, and since I already have everything in Excel, I wonder if it’s worth the effort. Anyway, I do not need any complex accounting for these expenses, just simple overview and that’s it.

Honestly, I would consider switching credit card primarily because of its CSV export capability! I also thought about changing banks because BKB’s “experts” have made the E-Banking experience worse. They still do not manage to provide detailed or separate columns for “collective payments” in the CSV output. As a result, all payments made on the same day are combined, requiring me to manually extract the information from a PDF. I have already complained about this, but they seem unwilling or unable to make changes. Either you make the payments on different days, you change bank or you take the PDF file and manually paste line per line into your sheet. Cornercard has updated their tool over the years, but they still provide a great CSV output. I’ve been using this credit card since I am 20 years old, and I remain loyal to them.

Well done, Thierry!

The state of banking is quite sad :( I can’t believe it’s so difficult to get a proper CSV exports. I really wish this was the baseline, not a feature to distinguish banks and credit card companies.

As you described above, it is quite tricky to get all expenses together. Especially since my wife an I don’t have shared accounts. I eventually resorted to an expense overview in G-Sheets, I update every six months or so. Some positions are calculated based on data and some are estimated. Already that helped me to find expenses to cut. Not perfect, but better than nothing.

Hi Lars

It’s a very good point. If you do not have shared accounts, it makes tracking much more difficult.

For many people, an estimation is better than nothing and something even enough.

Thanks for sharing

Hi

I track expenses using csv exports of online banking. Doing it almost daily.

I copy them into a selfmade Excel sheet where I can enter monthly or yearly budget values as an indicator.

Had to do a selfmade Excel sheet because banking switched off the nice feature that allowed me to classify each payment in the online banking application directly.

for budget I use a excel file from https://de.smartsheet.com. Works nicely

Hi Dan

Thanks for sharing!

For the long term, it’s best to have your own spreadsheet. That way, if you change bank, you can still continue to track everything.

Hello Does anyone here use Banana.ch for accounting and tracking expenses? I am used to tracking all expenses in Excel via bank statement downloads. I am starting to log receipts in Evernote, although I find any tracking of receipts tedious. I also try to avoid all cash payments to facilitate the electronic logging.

We started with a spreadsheet, tried Banana for about 6 months, and I absolutely hated it. I found the interface to be really clunky and it wasn’t easy to find basic data. It seemed to be built more for businesses than households. We’ve since switched to YNAB after reading some other blogs. There’s a free 1-month trial and then you do have to pay for it (about CHF110/year). You also need to enter transactions manually since Swiss banks won’t connect to it, but once you get the hang of it it’s very quick. The concept, interface, and data analysis are amazing and I’ll never go back!

I’m using YNAB also and very happy with it :). With the mobile app installed it’s so easy to add directly your expenses. I tried spreadsheet but if you want to have some KPI you need to do it by yourself in YNAB you’ve a lot of informations ! For me the price worth it :) and it’s budgeted.

Thanks for sharing, Elio. I am happy to know that many people are happy with YNAB. I should try it out.

Hi Simone,

I am using banana for the blog expenses. But it’s a bit painful to use and not very flexible. I am not sure it would facilitate your life.