Should you invest in structured products in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Structured products are complex investment products often suggested by banks. In fact, structured products are very popular in Switzerland, more than in most countries. They are widely used but often misunderstood. Products like reverse convertibles and barrier reverse convertibles may look attractive but come with hidden risks.

So, should we all invest in structured products? In this article, we go into the details of what these products are and how they work. By the end of this article, you will know whether you should invest in structured products or not.

Structured Products

A structured product is a package of investments. They will usually combine a product with fixed income, such as a bond, with a derivative. The derivative itself generally aims to track the performance of a stock. They can be heavily customized for different risk/return profiles. Like every other investment, there are some low-risk structured products and some high-risk structured products.

It is essential to understand that when we buy a structured product, we do not buy a stock, but instead we buy derivatives (contracts). So, we own a product from the issuer (the bank) and not a stock of the company. This is critical because it already adds a layer of risk: the issuer risk. Since we buy a contract from a bank, we are at risk if the bank goes bankrupt. And this is in addition to the market risk related to the equity itself.

In general, derivatives are riskier than stocks since we do not own them directly. And the protections are weaker in case of bankruptcy. Furthermore, a derivative is more complex to understand than a stock. Structured products usually work with stock options as derivatives.

Structured Products in Switzerland

Structured products are available in many countries, but Switzerland is among the countries where structured products are the most popular. Switzerland may even be the world leader in structured products.

All large banks in Switzerland offer access to structured products. And many of them (like UBS or Raiffeisen) issue them themselves.

I think there are three factors that make these products so popular:

- Structured products are extremely accessible. Almost every bank will try to sell you structured products.

- Many Swiss investors have a blind faith in their banker. So, they do not mind a lot of complexity as long as their banker tells them it will serve them well.

- Swiss investors do not have the necessary knowledge to either understand these products or know that there are better alternatives.

Types of structured products

As usual, banks are very creative when it comes to creating complex investment products. There are four main families of structured products:

- Capital Protection Products

- The goal is to protect some investment, while keeping a limited upside.

- These products are made for conservative investors who want to guarantee their capital.

- Yield Enhancement Products

- The goal is to generate higher income by taking some downside risks.

- These products are made for investors who want higher returns and can accept some moderate downside risks.

- Participation Products

- The goal is to make it easy to track an index or a set of stocks.

- Leverage Products

- The goal is to increase returns in markets moving up by using leverage.

- These products are for very aggressive investors who can take large risks to gamble for large returns.

And of course, in each of these families, there are multiple subtypes of products.

Each year, the Swiss Structured Products Association (SSPA) produces data on the structured products. In 2024, 196 billion CHF were exchanged on these products (SSPA Source). And here are the market shares of each type of product:

- 47% for yield enhancement products

- 28% for leverage products

- 11% for participation products

- 10% for capital protection

It appears that Swiss investors are truly interested in yield. Since they are the most commonly used, we can dig deeper in yield enhancement and see exactly what they are.

Reverse Convertibles

We can now delve a little deeper into yield enhancement products. As said before already, banks are very creative, and they come up with multiple of these products.

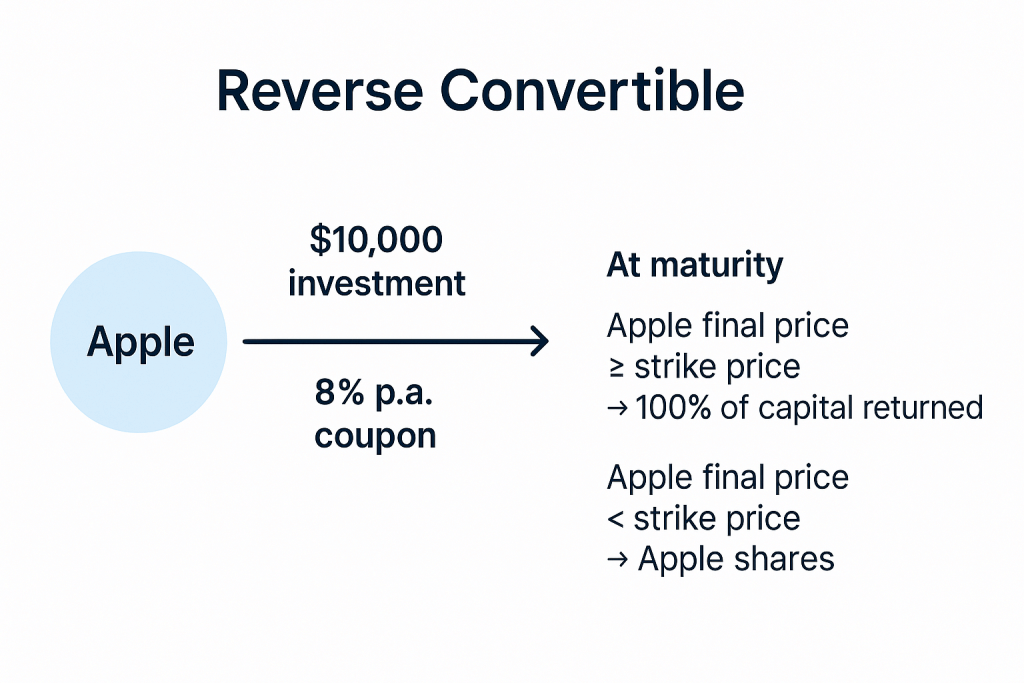

The most common product in this category is the Reverse Convertible. This product has a term and an interest rate. Additionally, the investment is bound to the performance of the underlying share. And there is usually a strike price that will dictate what will happen to your initial investment.

Confused? I think that is the goal of these investments. We can make an example with a Reverse Convertible on Nestlé shares. The term will be 12 months, and you will get 6% per year. The strike price is 95% of Nestlé’s price at issuance.

- The interest rate is guaranteed. You will receive 6% in a year, regardless of the stock performance.

- However, the capital itself is not guaranteed.

- If the stock price is below the strike price, you will get Nestlé shares instead.

- If the stock price is above the strike price, you will get your cash back.

So, if the stock price moves down a lot, you will bear the full downside risk (minus the interest rate you did). And if the stock prices move up a lot, you will not get the full upside returns (only the interest rate). This is a bit like betting that the stock will not move much. But if the stock moves much in either direction, the product is not helping you much.

Already, we can see these products are far from perfect while being complicated. And this is one of the simplest structured products.

We should also not forget about fees. Generally, you will not see any fees on these structured products. However, it is not because you do not see any fee that there are none. I do not know any traditional bank in Switzerland that has no fees. Commonly, issues will capture the margin of the put option. Unfortunately, this is not transparent, and we do not know exactly how much is charged (it can also vary from one product to another). We can estimate that these fees are at least 0.25% as a baseline, but they can easily go up to 2-3% in some extreme cases.

Finally, there is one more disadvantage to this product: you get income instead of capital gains. And income is taxed at your marginal tax rate, while capital gains are not taxed, unless you are a professional investor.

Typically, these products are implemented with a put option. If you would, you could directly take a put option, and you would probably be better off (except for potentially being considered a professional investor).

Barrier Reverse Convertibles

The second most common type of yield enhancement product is the Barrier Reverse Convertible. It is very similar to a Reverse Convertible, but it adds another level of complexity, with a barrier level on top of the strike price.

At maturity (end of term), if the underlying share finishes above the strike price, you get your full capital and your coupon (the interest). If the underlying share finishes below the barrier price, you will not get your capital but get the shares instead. In this case, you also get the interest. Finally, if it ends between the two prices, you will get your capital and you coupon.

There are unfortunately more subtleties. The main one is that there are two types of barriers:

- The European Barrier is only checked at maturity. This is pretty dumb because it means that a Barrier Reverse Convertible with such a barrier is actually the same as one without a barrier but a lower strike price.

- The American Barrier (Continuous Barrier) is checked at all times

So, with an American Barrier, you will receive Nestlé shares (and your coupon) if the barrier is triggered during the term and if the stock ends up below the strike price. Now, we are starting to understand the complexity of these instruments.

With such a product, the risk is higher, so the coupon will also be higher. But the general profile is very similar to that of the Reverse Convertible.

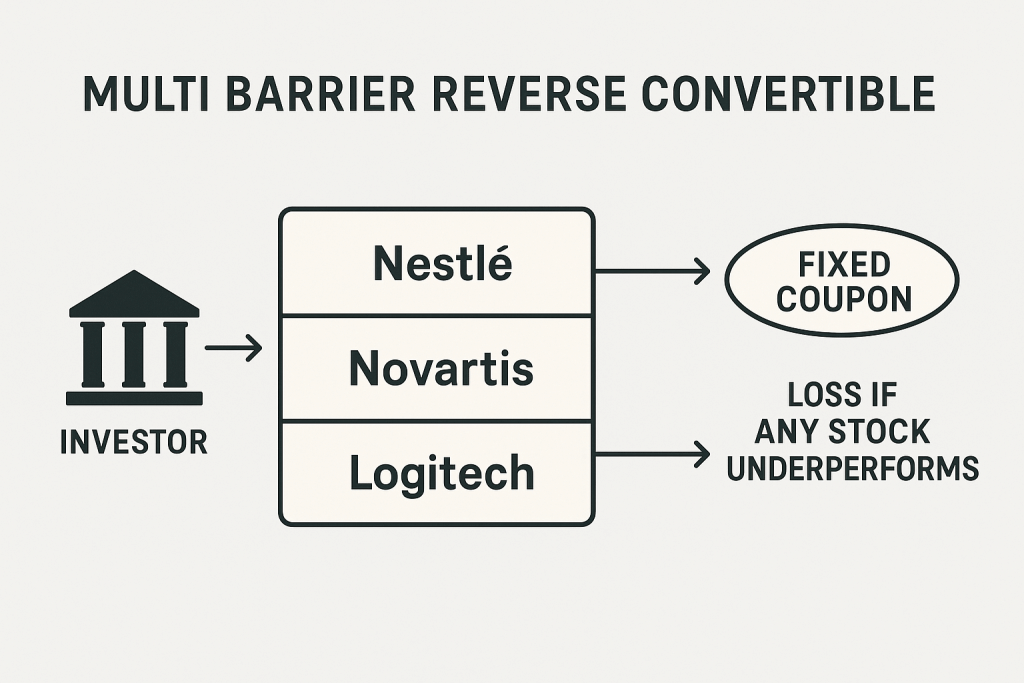

Multi Barrier Reverse Convertibles

Another very common type of structured product is the Multi Barrier Reverse Convertible. It is similar to a Barrier Reverse Convertible, but it works on a basket of stocks instead of a single stock.

In this case, the barrier is checked for each of the stocks. And if one of the stocks triggers the barrier and ends below the strike price (at maturity), you will get shares instead of your capital. It is important that a single bad stock can cause the barrier to trigger. Again, the coupon itself is guaranteed.

Again, this adds an extra layer of risk since there are multiple stocks, so the coupon will also be higher.

Callable vs. Auto-Callable Structured Products

We can cover two more details about structured products to close up this chapter.

Reverse Convertible are sometimes auto-callable. In this case, this adds another level of complexity. The product defines multiple observation times at which point the product can be automatically recalled. At this observation point, the price of the underlying product (or products if there are multiple) is checked against a trigger level.

If the price is above the trigger level, the product is redeemed entirely. In this case, you will receive your capital back and the coupon accrued until now. This is sometimes called an early redemption. This feature makes it even more complicated to understand what will be going on especially when combined with a barrier. In the end, you end up with many parameters:

- The strike level for the reverse convertible itself

- The barrier level and observation times (European or American)

- The trigger level and observation times (usually quarterly)

Finally, there is also something else: callable products. While rarer than auto-callable products, there are some Callable Reverse Convertible products available in Switzerland. In this case, the issuer is free to redeem the product early. This type of product only protects the issuer, since they can stop the product if it is no longer profitable for them.

On the other hand, there is sometimes a higher coupon in this case, but it is rarely worth it since the risks are mostly on the investor side. And this makes the income even less predictable.

In summary, an auto-callable product can be automatically recalled based on market conditions, and a callable product can be recalled by the issuer.

I believe there is no need to delve into more examples of structured products. We have proven that they are complex and varied. But know that there are many more types of structured products, and some are even more complex than those I discussed in detail.

Structured products and taxes

It is important to discuss taxes in detail because there are some significant differences between investing in structured products and investing directly in the stock market.

Most structured products have a coupon that is guaranteed. On this interest rate, you will pay income taxes. So this will be added to your taxable income.

On the other hand, when you invest in stocks directly, you usually have two components:

- The dividends, taxed as income

- The capital gains, usually not taxed (unless you are a professional investor)

In most portfolios, capital gains will outweigh the dividends.

In most cases, structured products are split into two components:

- An interest component that is taxable

- An option premium component that is tax-free.

So, depending on the split, you may end up paying more or less taxes than with stocks. Again, this is a complex system, and you have to be really cautious about which product you want to use. You will need to read the fact sheets of each product to know.

In the best case, the entire return is tax-free, like a stock without a dividend. In the worst case, the entire return is taxable, much worse than stocks.

Disadvantages of structured products

There are many disadvantages to structured products.

For me, structured products are too complex. They are simply too complex for most people to fully understand. And even if you can grasp the basic products (like a Reverse Convertible), it is difficult to grasp how it will perform in relation to the stock market. And the most advanced products are even more complicated. This complexity also makes these products quite opaque, helping banks hide spreads behind them.

Another issue is that we cannot capture the full upside benefit. If the stock moves more than the coupon, we have lost money. On the other hand, we capture most of the downside side (minus the coupon) in most cases. There are some products that work differently, but these are how the standard products work.

A smaller issue is that we do not own the underlying asset (nor the derivative) directly. First, this means we do not get dividends nor any vote. But this also means that we have an extra issuer risk. If the issuer goes bankrupt, you are treated like a creditor of the issuer and this will be resolved through standard bankruptcy claims. There is no deposit insurance on structured deposits. This makes them riskier than stocks and ETFs.

Advantages of structured products

Structured products have slight advantages.

If the underlying stock does not perform well (below coupon and above strike), you may get more money with a structured product than with the stock itself. But that is akin to gambling on the future to be in a rather narrow window.

Structured products produce more cash flow than stocks and ETFs. So, if you are in a special situation where you need to optimize cash flow instead of capital gains, these products may be interesting.

Overall, the advantages of structured products are only relevant in a few niche situations.

Alternatives to structured products

By this point, I believe nobody should invest in structured products. So, what is the alternative?

There are some simple alternatives: low-cost Exchange-Traded Funds (ETFs) or index mutual funds. These products are much simpler and much cheaper. Additionally, they are also more diversified because you can find indexes covering thousands of underlying stocks.

The most efficient way to invest in ETFs is to invest by yourself, through a broker account. You can read my guide on starting to invest if you do not know where to start. But even if you do not want the extra complexity of doing it yourself, you can invest in low-cost ETFs through a robo-advisor. In Switzerland, we have many robo-advisors that will invest in ETFs for a much lower fee than traditional banks.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

So, should you invest in structured products? No.

These products are overly complex and opaque. I think that banks are making these products complex deliberately just to hide the fact that they are not that great products. By complicating them, they can make investors believe that they must be good products.

Moreover, these products are also tax-inefficient and often hide some fees behind the complex structure.

In most cases, investors will be better off with much simpler alternatives like ETFs or mutual funds. Even investing in a single stock would likely be better than using such structured products.

What about you? What do you think about structured products? Would you like me to delve into them in more detail?

More reading

Imputed rental value is going away – What changes?

Imputed rental value is going away in the next few years. Should we do anything differently now? Here is what will change and our strategy.

Should you invest in gold in 2026? How to invest in gold?

Many people invest in gold for its rarity and value. But should you invest in gold yourself? Will gold help you retire?

Buying a house in Switzerland: The Complete Guide

Buying a house is no simple affair. However, with this guide, you should know exactly what you have to do to buy a house without issues!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

„Another issue is that we cannot capture the full upside benefit. If the stock moves more than the coupon, we have lost money. On the other hand, we capture most of the downside side (minus the coupon).“

Is wrong, it depends on the product! Have a look at the swiss derivate Map.

This products feel like simple option trading with extra steps. Definitely not appealing!

Yes, they are indeed like options but more complex and more expensive.

and what do you think about options on SPY and QQQ? these are indeed ideal for active trading and speculation, not investing, but i believe they are still easier than such structured products

I have written about options in the past: How do stock options work?

I think they are better than structured products, but they should be avoided by most passive investors.

Structured products are often composed (structured) of options.

Indeed. I have mentioned this in the article. My comment was to say that if you are interested in options, it’s better to use options directly rather than to rely on structured products.

I agree with the previous comment, the tax section is far from complete and partly incorrect. The last sentence has no end.

Have you looked at structured products termsheets when writing the article or read the circular n° 15 from the SFTA ?

Most of the issuers split the coupon between an interest (taxable) and option premium (tax-free). The split is shown in the termsheet.

Depending of the caracteristics, some structured products are totally tax free.

Thanks, I will update the section.

I’m not a fan of structured products, but the section on tax treatment is completely wrong.

Can you expand?

Read a BRC fact sheet. The coupon is usually made up of an interest payment and a premium payment. Only the interest payment is taxable in Switzerland. The Premium payment is not. Structured products can therefore be more attractive from a tax perspective than ETFs.

Example: “The product is considered as transparent and has no predominant one-off interest (Non-IUP). The Coupon of 7.00% p.a. is divided into a premium payment of 7.00% p.a. and an interest payment of 0.00% p.a.. The option premium part qualifies as capital gain and is not subject to Swiss income tax for private investors with Swiss tax domicile. The interest payment is subject to income tax at the time of payment. The Swiss withholding tax is not levied. In the case of physical delivery of the Underlying at maturity, the federal securities transfer stamp is levied on the basis of the Cap Level. The Federal securities transfer stamp tax is levied on secondary market transactions.”

Thanks, I will update the tax section.

Thanks Baptiste. Great article.

You mention that structured products are only relevant in a few niche situations…

But which niche situations do you think someone should be using structured notes?

Thanks video,

I do not have an example. My thinking is that if you need the money in a fix amount of time and do not to take too much risk and want interest, maybe they can be useful. But this is really niche.

Hi Baptiste, but the solution to that would be to purchase a bond that matures at a specific date or to buy an ishares bond ETF with a fixed maturity date.

Curious to know in real life terms when or IF a structured note could really be useful. (or is it just a legal scam?)

I am not convinced there are cases where they are really useful. But there are cases where some of their characteristics are not so bad.

But I do not see any reason where I would need them, and same for 99% of passive investors.

The fees are more like 1–3%, which is why banks are pushing them. You should have mentioned the recent UBS debacle, in which clients incurred combined losses of hundreds of millions in FX derivatives. If your bank tries to sell you something opaque, steer clear.

Hi Karl

I will emphasize on the fees more, but the conclusion is the same: Opacity and complexity only to hide bad things.