Should You Contribute to Your Second Pillar in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

In Switzerland, you can make a voluntary contribution to your second pillar. These contributions come with tax advantages since you can deduct them from your income. Therefore, you have a return equal to your marginal tax rate. And this return is almost instant.

However, the money is then blocked into the second pillar. And the returns on that blocked money have been very low in recent years. Finally, you can only withdraw the money from your second pillar if you retire, buy a house, start a company, or leave the country.

Many ask whether they should contribute money to their second pillar or continue investing in stocks. In this article, I answer this important question. And we even have a calculator that will let you do all this without any math!

Second pillar contribution

So, how does a voluntary contribution to the second pillar work?

Usually, you pay each month some amount of your salary to the second pillar. And this is matched by your company. You do not have a say in this. So, there is no way to optimize that.

However, you can contribute some amount to cover the holes in your second pillar. If you had a low salary when you started, you will surely have holes in your contributions. When you contribute, you can deduct it from your taxes, just like the third pillar. The second and third pillars are among the best tax deductions.

How much of a reduction in taxes this will realize is challenging to calculate correctly. It depends on your marginal tax rate. The amount will depend on your income, your wealth, and where you pay your taxes. In most cases, this will be between 30% and 40%. That means that the immediate rate of return of this contribution will be 30% to 40%. We can view voluntary contributions as a form of investment.

Now, the invested money will be blocked until you can take it. In the second pillar article, we have seen only four cases when you can take this money out:

- building a house

- starting a company

- retiring

- leaving Switzerland definitely

When withdrawing the money, you will pay a withdrawal tax. This tax depends heavily on each canton. The withdrawal tax is significantly lower than the taxes you can save with the contributions. You can save on the withdrawal taxes with staggered withdrawals.

Voluntary contributions are always blocked for three years (only the amount of the voluntary contribution is locked, not the entire second pillar).

As long as it is inside the second pillar, your money will get some interest rate. Unfortunately, the interest rate is currently low now. You can expect about a 1% interest rate in most pension funds in Switzerland. Nevertheless, it is a safe interest rate for now. It cannot go down. So, you can consider the second pillar as a place to allocate your bond.

However, if you are lucky, you will get a better pension fund. Some pension funds have average of up to 5% per year, but they are quite rare.

There is a second tax advantage to the second pillar. You do not have to pay taxes on the second pillar assets. So, if you have a large net worth, you will not have to pay wealth tax on your second pillar assets.

But this is a smaller advantage than the first one. It will still reduce your taxes a little further, but where the first tax advantage can be up to 40%, the second advantage is about 1% in the best case. Nevertheless, it is still important to know that you do not pay any wealth tax on your second pillar.

Scenarios

The obvious alternative is to invest in stocks. We can check how the same sum behaves if invested in stocks or contributed to the second pillar. First, we run some scenarios to see how that works. We will simulate a one-time investment of 10,000 CHF.

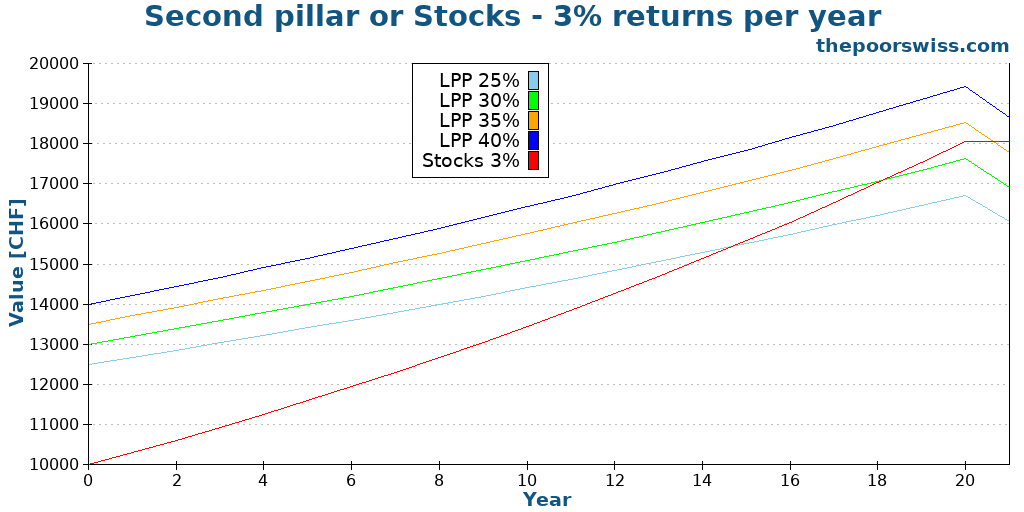

We start with a return per year of 3% for the stocks. This is a very conservative estimate. For the second pillar, we will consider 25%, 30%, 35%, and 40% marginal rates. The current interest rate on most second pillars is 1%. So we will take that as the reference.

The tax savings of the second pillar will be reinvested in stocks directly. So, if you have a marginal tax rate of 30%, 10,000 CHF invested in the second pillar will also result in 3,000 CHF in stocks.

Finally, we will consider a 4% withdrawal tax on the entire amount. In practice, this would only apply to the second pillar, not to the savings you have invested. But in practice, the tax is often higher than 4%, so applying 4% to the total is a reasonable assumption.

Here are the results for twenty years.

As you can see, it takes about 15 years for the stocks to catch up with even the lowest marginal rate. And it would take more than 20 years for the stocks to catch up with the high marginal tax rates.

In that case, a 3% return per year on the stock market is slow to catch up with a substantial interest rate as a tax deduction. So, if you expect 3% from stocks, you should probably favor your second pillar.

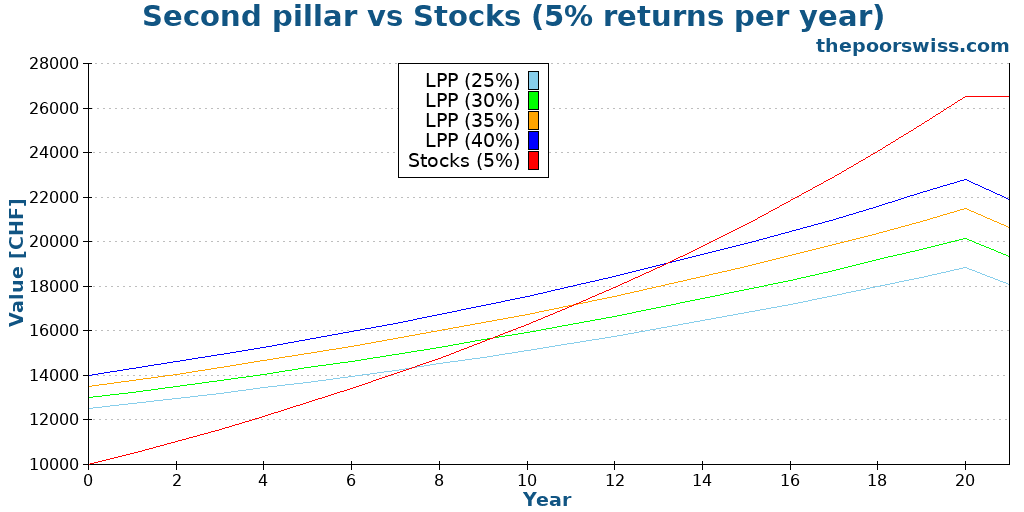

But generally, stocks are returning more than 3% per year. So, we will see what happens with a 5% return per year. This is what I expect on average from the stock market.

This time, it takes less than ten years for the stocks to increase as much as the second pillar, with the lowest marginal tax rate. But it almost takes 15 years to catch up with the highest marginal tax rates.

This exponential growth is the power of compounding. Even 5% per year can return a lot in the long term. 5% per year is what I expect from the stock market.

Obviously, in practice, you will not get 5% per year. You may get 10% one year and -20% the next year. But this is how the stock market works, and I am prepared for this. You can only expect average returns over the long term.

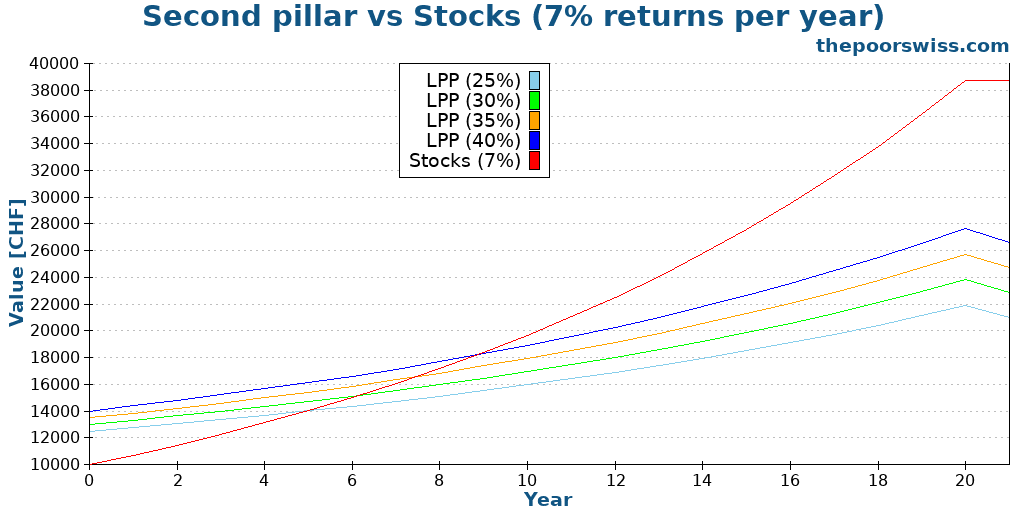

Now, some people are counting on about 7% of yearly returns. So, here is how that will go:

With 7% of stock returns per year, the return on the second pillar contributions is dwarfed. Even the highest marginal tax rates would be beaten after less than ten years. Compounding gets stronger and stronger as the returns increase.

So, we can draw a few conclusions from these results:

- The second pillar is interesting if you have a high income.

- The second pillar is interesting if you reinvest the tax savings in stocks

- If you expect very high returns from stocks, you should avoid the second pillar

- Over ten years, the second pillar is interesting

- Over more than 20 years, the second pillar is rarely interesting

However, there are other considerations. First, it will depend on the term of your investment. If you are investing long-term, it is probably better to stick with stocks. But if you are to get access to your second pillar soon, it may be a solid investment. It could be a good investment if you retire soon, build a house, or start a company in the medium term.

But do not forget that voluntary contributions are blocked for three years. So, if you intend to buy a house in the next three years, you should not invest in the second pillar (unless you already have enough in the second pillar without the voluntary contribution). If you plan to buy a house without the second pillar, you can continue your contributions if you have enough cash for the down payment.

Another thing you need to consider is whether you have a great second pillar account or not. If you have a good second pillar account invested in stocks, it will become more interesting to invest in it! But most people in Switzerland will not have access to a good second pillar.

The other consideration is whether you need bonds in your net worth.

Your bond allocation

Due to its safe nature and the guaranteed interest rate, I consider my second pillar bonds. I integrate my second pillar into my net worth as bonds.

So, another reason to buy into the second pillar depends on your allocation. If your bond allocation is too low for your current allocation, you can voluntarily contribute to increasing it. Given that it also has a nice tax advantage when you purchase it, it is probably better than bonds.

When Swiss bonds are negative, the second pillar is also much more interesting than Swiss bonds. If I need to increase my bond allocation, I will invest more in my second pillar instead of bonds.

At the start of 2021, we had 5.2% allocated to bonds in our net worth. Since we aim for 10% bonds. So, it shows that we should contribute a little to our second pillar. Unfortunately, it is not a good time for us, as we will see in the next section.

Proper Timing

There are some cases where it becomes very interesting to make such contributions.

- When you know that you will retire or buy a house in the medium term (but further than three years). Since they are short-term investments, it is good to use them as such.

- When you know that you will leave your company and switch to vested benefits account. This could be the case when you are retiring early or leaving Switzerland. These accounts are often much better than second-pillar funds. So it could be interesting to max out your contributions to have them invested properly.

On the other hand, there is one case where you should not contribute to your second pillar: when you do not get any tax advantage. When you withdraw money early from the second pillar (for a house or business), you will not get any tax advantage until you have paid back the withdrawn money. So, as soon as you withdraw money from the second pillar, it becomes pretty much useless to put more money into it.

This is the case for us. We just withdrew money from our second pillar and cannot get any tax advantage until we contribute at least 50,000 CHF. So, without the tax advantages, it does not make sense for us to invest in the second pillar.

These examples show that timing is important for second pillar contributions.

Our second pillar strategy

We have decided to contribute to our second pillar each year. So far, we intend to contribute 10,000 to 20,000 CHF each year.

We have a few elements to back up our decision.

- I plan to retire early. If my plan works, my money will only sit in a second pillar for at most 15 years. Then, it will go into a vested benefits account where it can be aggressively invested.

- We have a high income in a high-tax canton, meaning a high marginal tax rate (at least 40%).

- We currently have a decent second pillar. The conditions are good, and the historical average return has been more than 3% per year, which is above the average of second pillars.

If these conditions were not met, we would probably not contribute. But together, these conditions make the second pillar a good investment for us.

Use our calculator

If you do not want to do the math yourself for your exact situation, we have developed a second pillar calculator. This calculator will let you enter all the data about your situation:

- How many years until retirement?

- Your taxes.

- How much returns do you expect from your second pillar.

- How many returns do you expect from your investments.

- How much withdrawal tax you will pay on your second pillar at retirement.

We hope this helps you find out for yourself whether a contribution to your second pillar makes sense for your situation or not.

Conclusion

We have been contributing to our second pillar for the last few years to reduce our taxes.

From an investment standpoint, contributions to the second pillar can be a good medium-term investment. However, you should only do them if you have a high income.

Moreover, if you expect very high returns from your stocks, the second pillar becomes less interesting. And you should try to reinvest your tax savings in stocks. Even though they have a substantial initial return on investment, they have very low returns per year after that.

Moreover, the money in a second pillar is an excellent alternative to bonds. They have a guaranteed (at least for now) interest and offer an excellent tax reduction. These tax reductions would be quite interesting as one is nearing retirement. But remember that you can only contribute to your second pillar if you have a salary or have your own company.

But it is not necessarily the best investment at all times. Like every other investment, it will depend on your context and your situation. You should consider every element before you decide on any investment. And never make any rash decisions!

Finally, keep in mind that if you are withdrawing your second pillar from another country, the withdrawal taxes may be entirely different, so you will have to adapt the calculations if that will be the case for you.

If you are interested in saving money from taxes, you can read my article about the best tax deductions in Switzerland.

What do you think about this? Are you contributing to your second pillar?

More reading

Third Pillar: All you need to know to retire in Switzerland

Save on taxes today. Learn everything about the Third Pillar (3a) in Switzerland and how to choose the best account to grow your retirement savings.

First Pillar: All you need to know to retire in Switzerland

Understand the First Pillar (AVS). Learn how the Swiss state pension works, how much you contribute, and what retirement benefits you can expect.

Your second pillar when you stop working in Switzerland

Learn what happens to your second pillar when you stop working, become self-employed, or leave Switzerland. Essential tips for every situation.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Mr. The poor Swiss,

Another great article from you, may you explain a little bit how the initial numbers at year 0 came from from each graph. How you do pick this number as the start point in year 0. Thanks a lot in advance.

Blue ~10500

Red ~12750

Yellow ~ 13750

Green~14000

Hi,

It’s actually the returns of each of the investments after 1 year

* With stocks, you made 5% each year

* With the second pillar, you make an instant return (tax saving) of your marginal tax rate (30%, 35%, 40%) and 1% on the second pillar itself, and then in the following years, you can invest the tax saving in the stock market.

Does that make sense?

Good article.

Not so sure about your calculations though.

I’m assuming that you are using CHF 10k as amount to invest in stocks when not contributing to your second pillar.

With 30% marginal tax rate the amount to contribute to the second pillar would be CHF 10k/0.7=14285.71. Which means the graphs show incorrect representations for the contribution cases.

With 15 years left that would mean a required return on the stocks of 3.43% to break even. Not to mention the risk difference between the two options.

Hi capmac,

¨

I am using 10K in both cases. In the case of the second pillar, this brings in extra returns based on your marginal tax rate. These extra returns are invested in the stock as for the 10K for stocks.

In the case of stocks, 10K is invested in stocks.

The marginal tax rate does not give you more to invest in the second pillar, it gives you more to invest in stocks. By investing X int the second pillar, you are saving X*marginal tax rate. And then you can invest this amount in stocks.

Thanks for stopping by!

Hmm, I think this is a similar problem as with your third pillar calculations. Applied maths is always affected by perspective and can be biased.

My view is that in both cases you don’t get additional money to invest.

In case of stocks you even have e.g. 30% (the marginal tax rate) less to start with than with the second pillar case. So starting with 10k in both cases is already an issue.

I did contribute to my second pillar in 2018 and the expected tax reduction I received was exactly the marginal tax rate applied to the lump sum I paid in. But I don’t understand that as a return as that reduction basically ended up in my 2nd pillar.

Also I have roughly 15 years max left in the 2nd pillar and the interest rates are more around 2% in my case. So the stocks option is not really competitive in my case.

Is there any limit of 2nd pillar contribution like ~7k for pillar 3a?

Hi papuu,

There is, but it depends on each situation. It will depend on your contribution gap. So you will have to ask your second pillar provider to know the limit you can contribute.

It will depend on how much you have contributed, how much your income increased over the years, how many years you did not contribute.

Thanks for stopping by!

Hi Mr. The Poor Swiss

Have you thought of including wealth tax into your calculation? If you prepare for your retirement by investing into stocks, you probably will reach the limit, where you start to pay wealth taxes. This will somehow reduce the return of your stocks by having to pay more taxes.

Hi RetirementDreamer,

By my calculator, you mean the graphs on this article or the calculator on the website about retirement?

For the first case, I don’ think it matters much. Either for the second pillar or stocks, it will grow your wealth tax. And for your stocks, they should compensate for the growing wealth tax by returning more than the second pillar.

For the second case, you can include the estimated wealth tax in your expenses and the simulation should be accurate enough. Of course, we could add a wealth tax on top of that based on the current value. But I do not think this would add enough value to make it more complicated.

Thanks for stopping by!

Thank you for your response!

I do mean for the graphs in this article. As far as I understand, you will not have to pay wealth taxes on your second pillar, whereas you do have to pay them, if you invest yourself. This could have an impact on your decision to pay into your second pillar or not. It is different for each canton, but it looks like, that the wealth tax is in the range of per mill and not percent. So it will probably have a negligible impact on your decision.

It was just a thought to try to be as thorough as possible.

Hi,

Ok, I understand then :)

It’s a good point! You do not pay wealth taxes on the second pillar until retirement age. And then, you will pay a wealth tax. But you are right that this especially matters during accumulation. So this could be a good way to avoid some wealth taxes by having more money in the second pillar.

I will add try to do this once I update this article!

Thanks for the suggestion!

I feel like topping-up the second pillar is something for your 40s and up in my case. Right now, my marginal tax rate decreases significantly with my 3a (with VIAC) but wouldn’t decrease much more with 2nd pillar contributions. The more I earn, the more likely I’ll be able to decrease the tax rate by investing in 3a and 2nd pillar. Am I wrong?

Hi retireby50,

No, you are not wrong. You can do large contributions to the second pillar. This could help with a large salary to reduce your tax rate.

For really young people, this is not great since it’s a very short-term investment. But for people that are getting closer to retirement, it starts to make more sense.

Thanks for stopping by!

Dear Mr. Poor Swiss,

Topping-up the second pillar is an excellent tool to reduce taxes. There are also ways to pay no taxes on withdrawals (e.g. relocate to a foreign location that doesn’t tax capital payouts and has a double-tax treaty with Switzerland). I fully agree with your post that putting money into a second pillar is a lousy investment per se. However, it can be a powerful tool used strategically for paying less income taxes and plan the withdrawal well! Cheers, Matt

Hi Matt,

Yes, you are right that if you can avoid the taxes at withdrawal, it becomes more interesting.

It is also very interesting for the short-term for instance 4-5 years before buying a house.

I plan to retire in Switzerland, so I will pay taxes on withdrawal. Therefore, it’s not that efficient for me.

Thanks for stopping by!

Thanks for the great post.

Should we consider the combined investment?

If I pay 30kCHF in second pillar, and get 30 to 40% back on day 1 (let’s say 12kCHF at 40%), basically I can combine the two investing the 12kCHF.

With a total ‘cash out’ of 30 kCHF I would have:

30kCHF in second pillar 3%

plus 12kCHF invested at 3 to 7% in stock

Maurizio

Hi Maurizio,

This is a nice way to think to it. Especially since the extra money you get back from investing in the second pillar is not in the second pillar. I didn’t consider it like this, but it seems more correct.

You are not going to get 30% back since this will be money that you are going to save on your taxes bills, not something you are getting back. But it’s true that by the end of the year, you will have extra money to invest.

I have run a few calculations and it is indeed significantly better! It’s still not as good as stocks, especially with a high % returns, but it gets closer.

Thanks for pointing that out! I will have to redo my calculations once I get some time :)

Hi

Thanks for these calculation. Do your charts take into account the tax on payout? (Kapitalauszahlungssteuern)

Afterall it takes away about 5% of the FINAL value.

Hi,

No; my charts do not take into account. The final number for the second pillar will be even smaller. Unfortunately, it is difficult to compute how much taxes will be paid on the second pillar.

But you are right that I should account for that! I will try to update the post to make that more clear

Thanks for stopping by :)

Clear and simple explanation.

well done !

Thanks weirded :)

My question is if you are only allowed to invest in very low yielding debt instruments in your second pillar, tax-advantages account? Do you not have an opportunity to invest in stocks, mutual funds, ETFs through that account? If you can, tax-advantages stock returns are better than after-tax stock returns, assuming your ultimate goal is a secure retirement. If you’re looking for liquidity and have a more pressing purchase in mind, after-tax is the way to go.

Hello Young (YATI? YI? :) )

That is a very good question.

If we could choose the allocation of our second pillar, it would make sense to invest as much money as possible into it. Unfortunately, Swiss second pillars are much worse than 401(k) from the United States. The pension Funds companies are allowed to invest the money as they wish but they only give you very little (1% per year currently) of the returns. This really sucks. But there is nothing we can do.

We cannot choose what our second pillar money will be invested into. Therefore, it’s not as good an investment as it seems.

I hope that makes sense

Thanks for stopping by

Well that stinks. That makes it tough to justify putting in more than the amount to receive the employer match.

And I suppose YATI is the best. It’s what some others have called me.

I agree, it stinks. There is still the advantage of the initial tax advantage. So I am going to use it if I want more bonds. But for now, my second pillar is already quite big compared to my stocks.

Thanks for stopping by YATI ;)