Some extra income in retirement goes a long way

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Typically, retirement means a lack of income, but having some extra income in retirement can help a lot. Having some income in retirement means we need less from our portfolio. This can help you retire earlier, even if it means having something closer to a partial retirement than a true retirement.

But how much does extra income help in retirement? We will find out with our historical simulations.

Income in retirement

Obviously, for many people, income and retirement are not very compatible. The goal of most people is simply to not work in retirement. But many people want to retire earlier, and extra income in retirement may definitely help since it should make retiring easier.

We cannot count dividends as extra income in retirement since retirement is already based on dividends and capital gains. However, there are multiple other ways to generate extra income in retirement:

- Some people could do some part-time employment. Working one day a week can yield a significant income in retirement that can help reduce the needs of retirement. Examples could be working as a waiter or a barista or even doing some administrative work for a small company.

- Some people could do some side hustles. Examples could be doing some consulting or chores for other people (like dog walking).

- Some people could build a side business, like a blog or a small 3D printing venture.

Of course, there is also one major downside to income: income in retirement is not guaranteed. If you plan a partial retirement with 20% employment and you lose your side job, you may not be able to sustain your retirement expenses. So, planning for extra income in retirement needs careful planning.

Retirement of 30 years

To see the impact of some income in retirement, we will use my standard simulation:

- Use historical data from 1871 to 2025

- Each possible month is tested as a simulation starting point

- Use yearly rebalancing

- Use historical monthly returns from US stocks and bonds

- Use historical US inflation

A simulation is a success if there is more than zero left in the portfolio. Even a penny left at the end of the retirement period is a success. And the success rate is the percentage of simulations that ended up with a success.

If you would like to learn more about how I do these simulations, you can read about my updated trinity results.

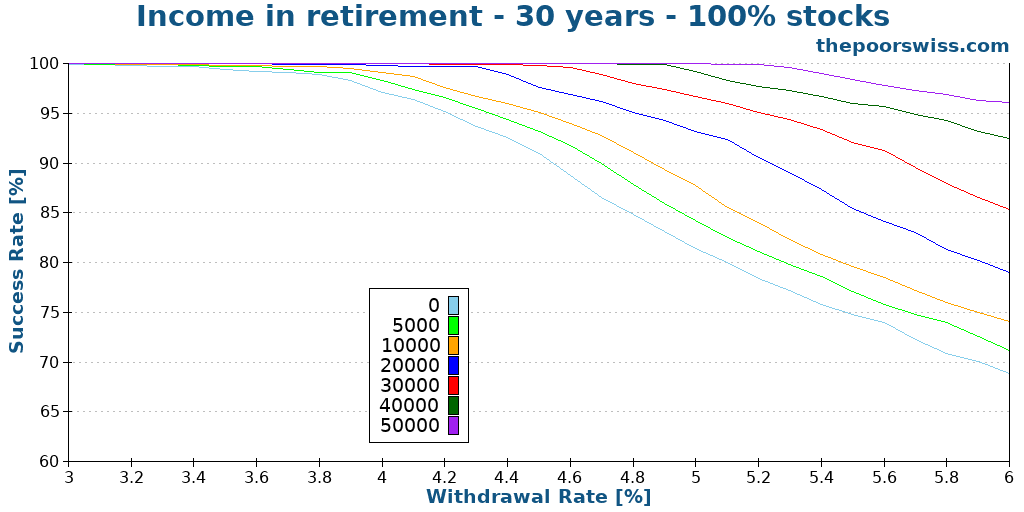

We can start with a portfolio of 100% stocks and 30 years of retirement. We will use an initial value of 100,000 USD and add some extra income to see the impact of income in retirement. In these simulations, I will not adjust the extra income for inflation. So in practice, if you can manage to follow inflation with your income, you can expect even better results.

We can see that income in retirement significantly increases success rates. Even adding 5,000 USD extra income (per year) can significantly raise the success rate. This represents 5% of the expenses. Even that would potentially allow raising the withdrawal rate slightly. And achieving a higher income will raise our chances even more.

For instance, if you are looking for a 90% success rate, you could use a withdrawal rate of about 4.6% without income. But if you cover 20% of your expenses with income in retirement, you could go up to a 5.3% withdrawal rate. This means you would have to accumulate much less money for your retirement.

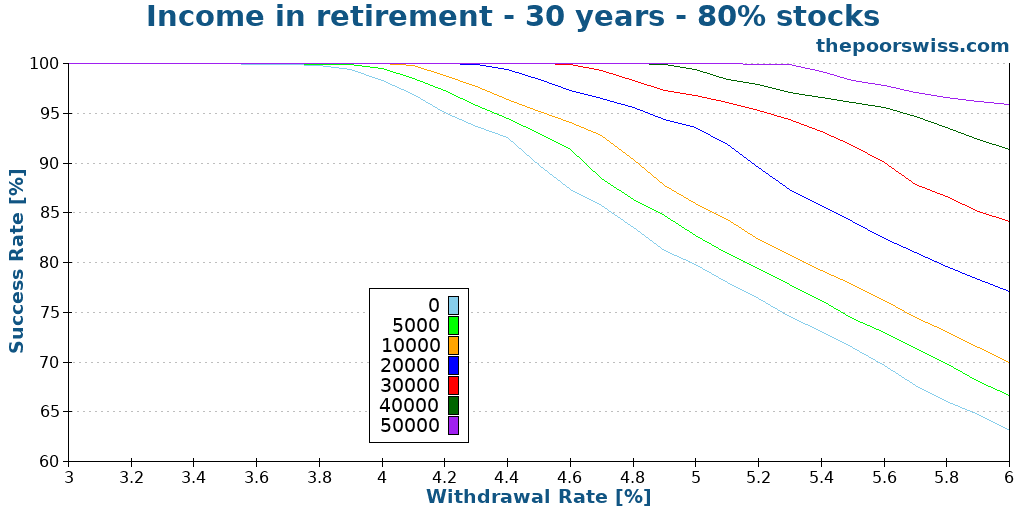

We can also see if these results are the same for a portfolio of 80% stocks and 20% bonds.

The scale of the improvement is comparable for the two portfolios. In both cases, we can expect a significant improvement to our chances of success by adding some income in retirement. To avoid filling this article with many graphs, we will only use these two portfolios. You can use the advanced FIRE calculator if you want to test adding extra income to your withdrawal simulations.

Of course, a retirement of 30 years is not very challenging to achieve. If you are looking for early retirement, you are likely aiming for more years, so we need to extend our simulation.

Retirement of 40 years

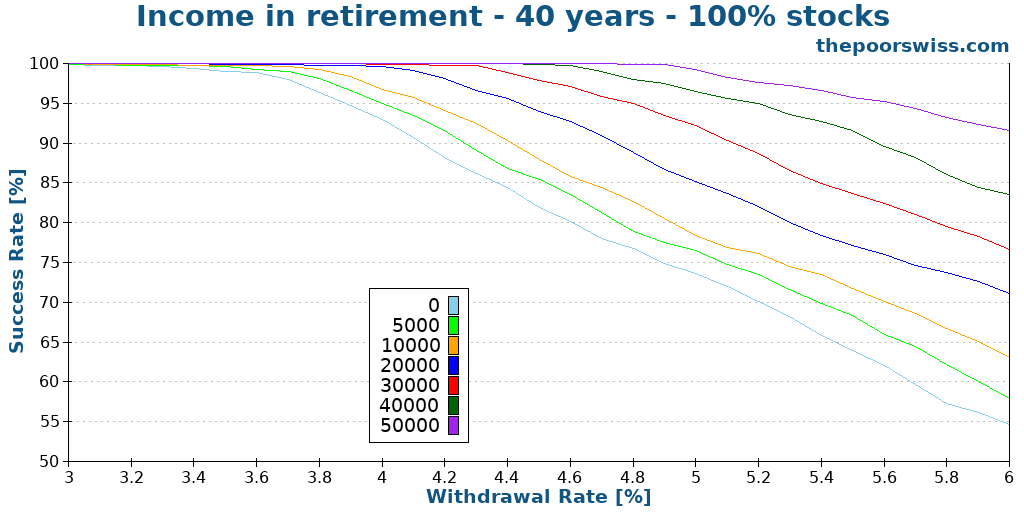

Let’s redo our simulation with 40 years of retirement to see the impact of income in retirement.

We can draw similar conclusions for 40 years of retirement as we did for 30 years of retirement. We can see that the magnitude of the improvement is more or less the same.

Again, we can take an example from these results. If you look for a 95% success rate, you would need a 3.9% withdrawal rate. But you could use a 4.2% withdrawal rate with 10% of your expenses covered by income in retirement. Even a 0.3% difference in withdrawal rate will make a very significant difference.

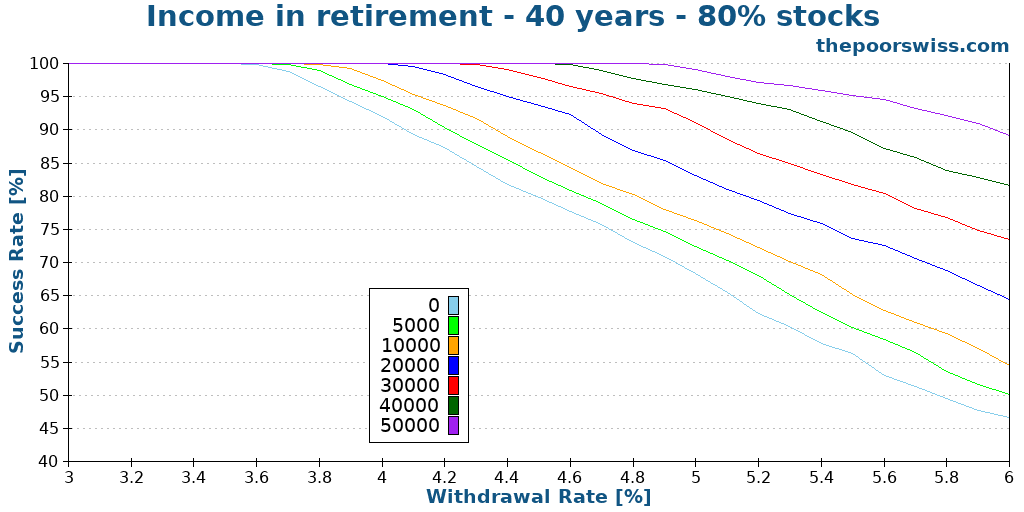

Let’s quickly see if this holds for our second portfolio.

Indeed, this still holds true.

We can draw a quick rule of thumb: in these simulations, by covering 10% of our expenses, we can increase the withdrawal rate by about 0.2% without changing our chances of success. And each extra coverage is better than the previous coverage.

Covering 10% of expenses with extra income is doable, but more than 10% will be a stretch for many people unless they are considering multiple days a week of work, which does not sound much like retirement.

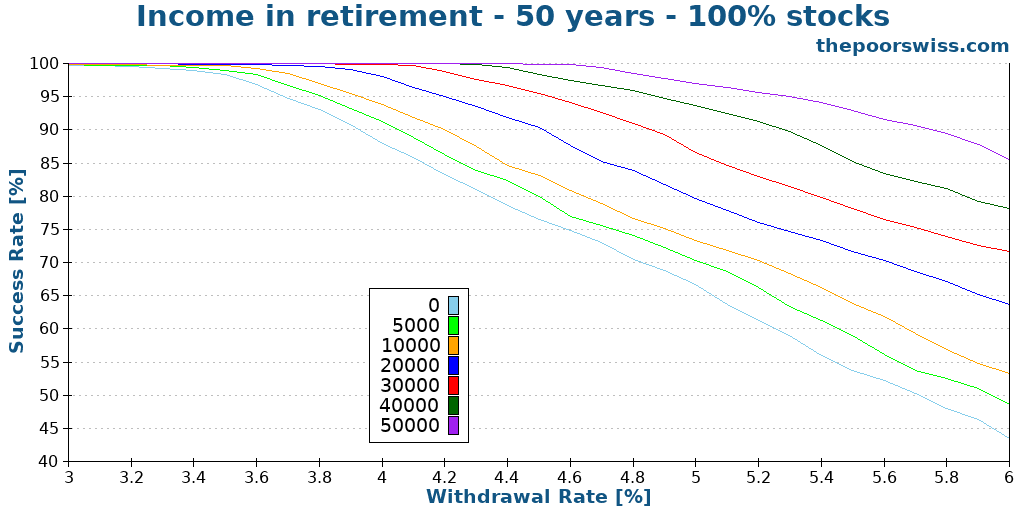

Retirement of 50 years

Finally, we can continue our simulations with retirement lasting for 50 years. This is a long enough period to be useful for most people.

We can observe that income in retirement is slightly less potent than before, probably because we do not adjust the income for inflation. Over 50 years, this can make a significant difference. However, the effect is still very significant and on a similar scale as for 40 years of retirement.

We can take a final example from the results. If you want a 90% success rate, you need a 4% withdrawal rate without income. But if you manage to get 20,000 USD of income, you will only need a 4.6% withdrawal rate.

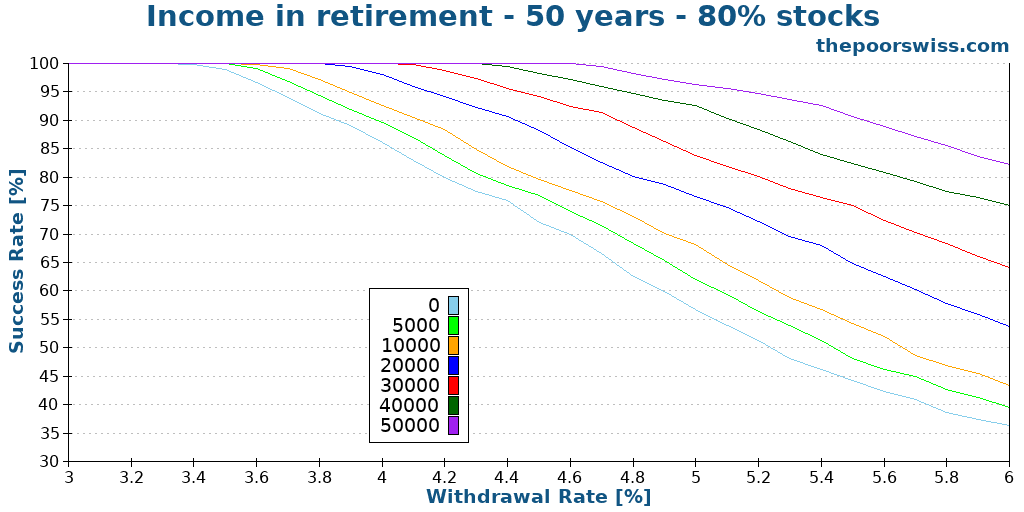

Finally, we can see if this stays the same for our second portfolio.

We can see that the results are really similar and the conclusions are the same.

A simpler way to look at income in retirement

Until now, we have assumed that extra income in retirement would help us use a higher withdrawal rate, which makes sense. But it is not very practical to calculate since you need a FIRE calculator to find out which withdrawal rate you can use.

Another simpler way to plan for extra income is to reduce the withdrawal amount accordingly. Indeed, if you get some extra income, you do not need to use your portfolio for so many expenses. For instance, if you are planning for a retirement with 60,000 USD per year and can get 12,000 USD income per year, you only need 48,000 USD from your portfolio. You can do some FI planning with this number instead. And this means it is easy to plan for extra income in retirement.

Again, I should emphasize that you should account for the probability of the income staying for long. If you plan for only 75% of your expenses and lose your side income, you will have to either cut down your expenses to 75% or go out of retirement (if possible).

Conclusion

The results are clear: even a modest income in retirement can help a great deal with your chances of success. As such, we can retire with less money or retire with more safety if we are capable of generating some extra income in retirement (outside of dividends).

Of course, the absolute numbers are highly dependent on the US data. Income in retirement will help in any country, but the scale of the improvement may be different.

Obviously, getting some income means doing some work. For some people, it is entirely acceptable if this helps them retire sooner, but many people want their retirement work-free. So, income in retirement will not meet all needs.

There is also one big downside to income: it is not guaranteed. It is essential to take this into account. If you account for a large income in retirement and you suddenly lose that income, you may be in big trouble. As a margin of safety, I would probably account for a portion of the income in an FI plan.

On our side, we are too far from retirement to know whether we will have any income in retirement or not. However, I can imagine that the blog is still generating some income when I quit my main career. Once I am closer to retirement, I will plan accordingly.

If you want to learn more about income in retirement, you should read about the impact of social security on early retirement.

What about you? Are you planning to retire with some income or income-free?

More reading

Out of The Rat Race – Financial Freedom – Book Review

Out of The Rat Race is a good book by Eric Duneau that tells how to achieve Financial Freedom by leveraging Real Estate properties, with low savings rate.

Not All Assets are Created Equal – Introducing the FI Net Worth

What counts for FIRE? Learn why your "FI Net Worth" is different from your total net worth and which assets you should exclude from your calculations.

How to choose a Safe Withdrawal Rate?

Your Safe Withdrawal Rate (SWR) is a fundamental piece of your retirement planning, here is a step-by-step guide on how to choose it for you!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

If you retire before the official retirement age in Switzerland, you also need to bear in mind that you will be obliged to continue to contribute to the AVS system based on your assets if you are not working. However, if I have understood correctly, if you have some other activity bringing in money, you may be able to contribute only on the basis of that activity and not your net worth. Do you have any experience of this? I also understand that it cannot be completely marginal.

Hi Max

There is indeed a minimum of 530 CHF per year for the first pillar. If you have high wealth, this can increase significantly as well.

If you have a full time income (or more than 50%), you will not pay this minimum contribution, but pay based on your income.

If you have less than 50% employment, you need to pay at least half the minimum (based on wealth) with your job or contribute the difference.

So, yes, the income must be real to offset that contribution.

My opinion renders the discussion of “early retiring” quite problematic: let’s take a man/woman who has a life expectancy (upon actual official Swiss data) of about 82/86 years. Let’s make another assumption, that they work from 20 to 82/86 years, meaning just … of the years they live (men: 38/82 = 0,46; woman: 38/86 = 0,44; altogether about 45%). Do you really think, that’s it correct to work for your live less than half of the time and depend for the rest on others…… because someone has to pay the bill …….

My credo of a work-life balance is: to heavily invest energy during your working live (20-65 yrs) and enjoy only afterwords. Otherwise you let work others for you, and that’s selfish …. . the social components of our taxes have to be payed…. and so also for infrastructure, etc ….

In conclusion; I think that early retirement is not an altruistic procedure (and should therefore be abandoned), about all if you are healthy and I good shape……

I think that once upon a time, there should be a contrarian thinking to your – otherwise excellent- research.

Hi Andrea

I don’t think I agree with you :)

During the early retirement years (from let’s say, 50 to 65), an early retiree does not get any pension or social support. So, they do not cost much to others. People with early retirement actually rely much more on their own than others. Usually (if they planned well), they would not need any help in retirement.

But it’s true that they contribute less in taxes. And I agree that it’s not altruistic, but I don’t believe that working more would be much altruistic either.

How are you letting others work for you if you are literally living off your savings and investments? That’s money you have earned and not yet spent.

Yes, I think it’s fine to only fork 20/80 years if you can manage it. This world has become to capitalistic, if you work, you are with a very high likelihood just being exploited for the benefit of someone ten to hundred times richer.