What is the best third pillar in Switzerland for 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

In Switzerland, contributing to your third pillar is one of the easiest ways to save on taxes. I recommend everybody to contribute to their third pillar.

But contributing to your third pillar is not enough. You should invest the money in your third pillar. That means you have to pick the best third pillar for your money. Since there are many options, choosing the best third pillar for your needs may be difficult.

So, this article is here to help you! We see how to choose the best third pillar!

What makes the best third pillar?

First, we must consider what makes the best third pillar. We must decide which factors will drive the choice.

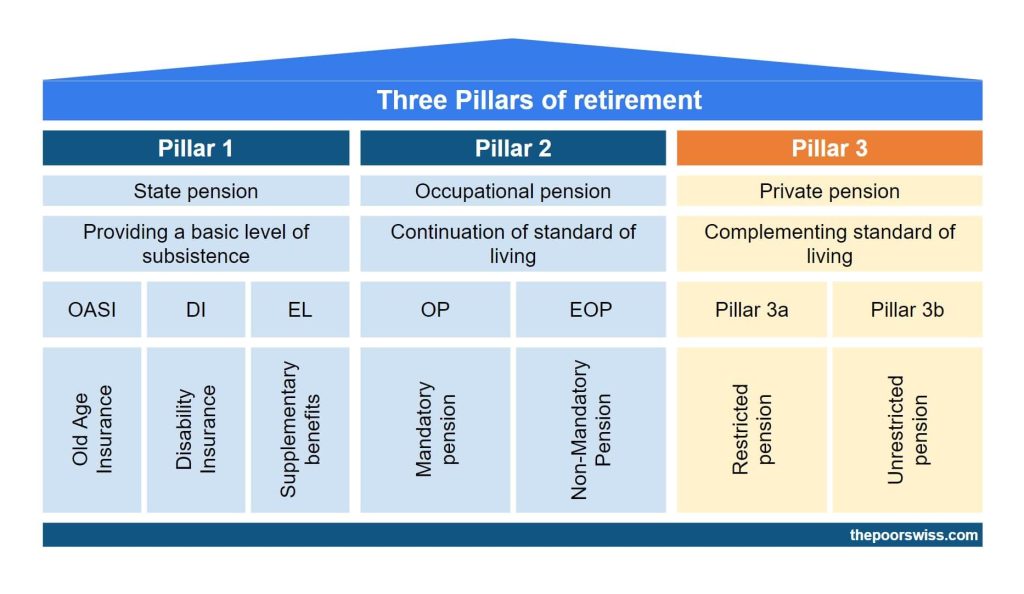

I assume you already know about the third pillar and are contributing to it. If you do not, you should learn why you should contribute to the third pillar.

We only consider bank third pillars, not insurance third pillars. Indeed, in almost every case, a bank third pillar is much better than an insurance third pillar.

The goal of your third pillar is to provide you with enough money to retire comfortably. Therefore, you want your invested money to grow as much as possible while not taking too much risk. So, the best third pillar must support this goal!

There are three critical factors in choosing the best third pillar:

- A large allocation to stocks will increase your returns in the long term.

- A diversified stock allocation reduces the volatility of your portfolio.

- Low management fees to avoid wasting your returns in fees.

Since we are counting on the long term, there are also some things we can ignore:

- How good the app looks is not relevant. You will spend less than an hour every year.

- The interest on the cash part is irrelevant unless you do not want to invest.

We will now delve more into the details of the three critical factors.

Allocation to stocks

The best third pillar has a significant allocation to stocks.

It will depend on your situation, of course. You need to choose yourself your asset allocation. Recently, Swiss bonds have had negative interest rates for about ten years. When this is the case, what is not in stocks should be invested in cash.

I want to allocate as much of my third pillar to stocks as possible. I already have bonds in my second pillar, and my current allocation to bonds is more than enough. Ideally, a third pillar will have a 100% allocation to stocks.

Diversification

The best third pillar has a diversified stock allocation.

Switzerland is too small of a country to only invest in its stocks. We need to have global stocks (stocks outside of Switzerland). Ideally, the allocation should be the same as a world stocks fund. Since the Swiss stock market represents about 3% of the entire stock market, we should avoid investing much more than that.

Unfortunately, this is not possible in Switzerland. The law states that the third pillar must have at least 40% allocated to Swiss stocks. So, an ideal third pillar should have 60% of international stocks and 40% of high-quality Swiss shares.

As we will see later, there is a way around this limit, making some third pillar providers significantly better than others.

Fees

And finally, the best third pillar has fees as low as possible.

I want my third pillar to have zero load fees. I do not want to pay to get money inside the fund. The absence of load fees is essential. You should never use any fund with load fees.

Moreover, the yearly fees must be low, and the TER must be as low as possible. Most third-pillar accounts in Switzerland have higher than 1% TER.

When you are investing for the long term, it is essential to minimize investing fees. The difference in returns in the long term is significant.

Third Pillar from a Bank

Most people in Switzerland will invest in a third pillar their banks provide. And they have a ton of options. Historically, they have been the only option available for third pillars.

I will not go over all the possible offers here. Indeed, there are too many of them. And most of them are terrible options. But I will go over some interesting options from some popular Swiss banks.

We will use the third pillar accounts from banks as examples. These are not the best third pillars.

Migros Bank Fund 85 V

My current bank is Migros, so I wanted to check their offer.

They have several retirement funds. The most interesting is Migros Bank Fund 85V. It has 85% in stocks and the rest in bonds and money market. The TER is 0.94% per year.

The allocation to stocks is slightly low but not too bad. The TER is not that bad for a Swiss bank. But I would not recommend this fund.

LUKB Expert Fund 75

Many people recommend the Luzerner Kantonal Bank’s LUKB funds. Let’s take a look at their LUKB Expert Fund 75.

This fund has 75% of stocks, which is alright but not great. 40% is invested in Swiss stocks, 35% in global stocks, 15% in Swiss bonds, 4% in international bonds, and the rest in liquidities and real estate. The diversification is not too bad when compared with other options.

It has a TER of 0.8%. For third pillar accounts in Switzerland, this is a good TER. However, it has a load fee of 0.4%. The TER is okay, but the load fee makes it highly undesirable.

PostFinance 3a

Many people are using retirement funds from PostFinance. These last few years, they have changed their lineup many times.

For me, the only interesting fund they are offering is the PF Pension – Passive 100 Fund. This fund invests 100% in stocks. Only 8% is invested in Swiss companies, while the rest is invested globally. This is a good allocation (better than average). However, only 25% are invested in foreign currencies, so this fund relies heavily on currency hedging.

The TER is 0.87%. This is expensive but better than it used to be. It would be better if they had lower fees and lower hedging, but at least PostFinance is going in the right direction.

Raiffeisen Pension Invest Futura Equity

Since many Raiffeisen banks have a good reputation, it is a good idea to look at their retirement funds, and more specifically, the Pension Invest Futura Equity fund, a mouthful.

This fund has between 80% and 100% in stocks. I do not know why it is not fixed. But the last invested value I saw was 95% in stocks, which is good. 47% is invested in Switzerland, which is not great but not the worst.

The TER of the fund is 1.42%, which is awful. While it is not the most expensive fund in Switzerland, it is the most expensive that I will mention today. And it is far too expensive for people to consider.

Swisscanto Fund 95 Passiv VT

Swisscanto provides many Swiss funds, and many banks use them. We can examine the Swisscanto Fund 95 Passiv VT.

This fund invests 95% in stocks, which is excellent. The diversification is also good, with 65% invested in foreign equities. However, they hedge most of the equities, with 72% in CHF for the entire fund. This is not great for currency diversification.

On the fee side, this is an excellent example of how banks are trying to make it complicated for people to know how expensive it is. The flat fee for the fund is only 0.38% per year. At first sight, it sounds great. But if you look in detail, we can see that this is a fund of other funds, so there is an extra 0.33% in fees for the sub-funds. But they never show the full fee of 0.71%. On top of that, they are adding a 0.1% issuance fee and a 0.09% redemption.

It is the most complicated fee system I have seen during my research. They use several small fees not to scare customers away, but when you add up all the costs, this does not make them very attractive. And just because of this lack of transparency, I would not invest in their funds.

Independent providers

As we saw, offers from banks are not that great. Fortunately, recently, many independent providers have started in this market. And they are offering much better conditions than banks.

We have observed that banks have high fees, sub-par diversification, and not aggressive enough portfolios. Independent providers are fixing all these issues. So, to find the best third pillar, we need to look at these independent providers. Note that they are not all good. There are also some bad options.

There is no disadvantage to having your money in a third pillar from these companies instead of at a bank. They only have advantages.

There are many, but I will only mention two main providers in this article: Switzerland’s two best third pillar providers.

Finpension 3a – Best Third Pillar

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

For most long-term investors, Finpension 3a will be the best third pillar available in Switzerland.

Indeed, they have some powerful advantages going for them:

- You can invest up to 99% in stocks

- The fees for an aggressive portfolio are extremely low, at 0.39% per year.

- They have a mobile application and a web application.

- You can make custom portfolios with a lot of liberty.

Finpension 3a is the best third pillar for long-term returns, with a high stock allocation and low fees. This is a great way to ensure your money is well invested until retirement.

Interestingly, Finpension also runs an excellent vested benefits account. They are experienced in the pension industry and provide great products.

Finpension 3a is the best third pillar available for aggressive long-term investors. So, in 2021, I started investing my third pillar in Finpension 3a. As of 2025, I am still using them, and I have five portfolios with them.

For more information, you can read my review of Finpension 3a.

VIAC – Good Conservative Third Pillar

In some cases, VIAC is an interesting alternative as well.

VIAC is a little more mature than Finpension 3a. They also offer an excellent third pillar. In general, they have several disadvantages over Finpension:

- Their custom strategies for investing are more limited.

- The fees are very slightly higher.

However, they have some advantages for conservative investors who would not invest fully in stocks:

- They allow you to invest in cash or bonds.

- The fees are lower if you invest in stocks and cash. Indeed, you only pay fees on the invested part.

So, if you are a conservative investor (or a short-term investor) and do not want bonds, VIAC may be better. But this is only true if you do not use bonds. If you use stocks and bonds, Finpension 3a is cheaper. VIAC used to be the best third pillar until Finpension 3a came along. But it is only interesting in a few cases now. Another advantage of Finpension is that they are leading in innovation. For instance, they allow 99% of foreign exposure long before VIAC.

For more information, you can read my complete review of VIAC.

True Wealth 3a – Cheapest Third Pillar

True Wealth is first a robo-advisor, but they also offer a third pillar account. They are the most recent of the 3 third pillar accounts. But they have some interesting characteristics:

- They are the cheapest 3a available, at a 0.18% fee

- You can invest 99% in stocks

- You can invest 99% in foreign currencies

On the other hand, they have some disadvantages as well:

- It is impossible to customize the 3a independently of the robo-advisor assets

- It is impossible to use a different strategy for different 3a accounts

- You cannot choose to which portfolio you transfer

For more information, you can read our review of True Wealth 3a.

Conclusion

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

Overall, the best third pillar available in Switzerland is Finpension 3a. They offer the highest allocation to stocks and the lowest fees. On top of that, you can create custom portfolios with a high degree of liberty. This makes them an excellent option!

For these reasons, in 2021, I invested in Finpension 3a instead of VIAC, and I recommend that all aggressive investors do the same. I have five portfolios with Finpension 3a.

If you open a Finpension 3a account, please use my code FEYKV5. This code will give you a fee credit of 25 CHF (if you deposit 1000 CHF in the first 12 months) and will help my blog as well.

If you need additional information on these two third pillars, I have an article on VIAC vs Finpension. This article goes more in-depth into the comparison.

What about you? Which is your favorite third pillar?

More reading

Frankly 3a Review 2026: Pros & Cons

Frankly Review. We analyze ZKB's 3a app, its fees, and investment strategies to see if it competes with VIAC and Finpension.

Interview of Beat Bühlmann – CEO of finpension

Inside Finpension. Read our interview with Beat Bühlmann, CEO of Finpension, and learn about their mission to revolutionize Swiss pension plans.

Pilla 3a Review 2026 – Pros & Cons

Pilla 3a is a new digital third pillar account proposed by CA next bank and the Liberty Foundation. Is it good? We review it in detail.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi The Poor Swiss, thanks for this great content, s always :)

VIAC just announced a fee cap at 0.44% which makes it equally cheap with finpension, even for aggressive strategies.

Hi great post!

Are you sure that postfinance applys a 1% TER?

I found this of their website:

Issuing commission (one-off)

– 1% at PostFinance, or 0.5% for

holders of a private account plus,

a youth or student account

– no issuing commission for the

retirement funds

Swiss federal stamp duty (one-off)

– only due when purchasing units in

funds domiciled abroad (0.15%)

Hi Jack,

TER and issuing commissions are not the same thing! The TER is a management fee that you are going to pay every year on your invested money (in percentage).

The issuing fee is how much you pay to get shares of the funds.

Hello there,

VIAC has lowered the prices of its 80 and 100 strategies! For example Global 100 is 0,45%. Still a bit more than finpension, but it is a very good news!

Yes, this is great news for third pillars!

I have to update all the articles now :P

Hey Mr. The Poor Swiss,

First of all, I want to say a huge thank you for your amazing website! I’m reading and following it for a few moths now and it was very helpful for me. I started investing (for now through Selma and TrueWealth as I can’t decide which broker to choose (…) so for now I opted for boots instead of nothing), opened a Neon account and 2 Viac 3a.

I would like to share one piece of information for those of you who, like me, regret the lack of ID checks at registration with finpension. You can simply send pictures of your ID per mail. finpension will check your identity and keep your photos on their file. It’s what I did and now I have a Durable 100 3a by them :)

Regards,

Hi Arafinwe,

Congratulations on starting investing!

It’s good that they take IDs by mail. That way, your account will be somehow verified :)

Thanks for letting me know!

Love reading your articles. Good stuff! Keep it up!

Thanks :)

Any thoughts on UBS (CH) Vitainvest – World 100?

I am assuming you are talking about the World 100 Sustainable. It’s incredibly expensive, at 1.63% per year. That’s three times more than VIAC and four times more than Finpension 3a!

Thanks for the article Swiss Poor,

Viac is offering the option of decreased processing fees by inviting other members. How do you think it compares to finpension with this offer included?

Hi Nick,

Since this is capped at only 5500 CHF without fees, this only makes a difference for “low” amounts of money in the third pillar. So, if you have less than about 30’000 in your account, VIAC can be cheaper because of this bonus.

But this is not counting on the potentially higher returns of Finpension with 99% instead of 97% in stocks and potentially more foreign exposure. So, overall, I do not think this invitation system matters much.

Hi,

I am considering moving to FP as well, but what’s the advantage? In 6-7 years I will be retiring….

– 0.1% lower fees

– 99% investing in stocks/etf’s

What is the risk (assuming similar performance)?

– etf course risk

– 1 month out of business

– on boarding at FP without personal identification

– any experiences with FP?

Hi Klaus,

The advantages are indeed the lower fees and the 99% in stocks. If you want, you could also get more aggressive and max out the exposure to foreign currency, which could increase your long-term returns.

The risk is mainly on the added volatility but should be minimal. The cost of 1 month out of the stock market could be high, but impossible to evaluate.

Now, whether you should move to FP depends on where you are now. If you are with VIAC and only have 6-7 years befor retiring, it won’t make a huge difference either way. So, if you are happy with VIAC, you can stay with them. If you are using something else, it’s likely worth it to move to FP.

Hi Mr Poor Swiss,

yeah right now i´m with VIAC (Sustainable 100) and quite happy with them. They have 2 other points should be mentioned:

– very helpful and responsive support

– chat function

The point is i have 6-7 years before retiring. I´m not sure the two arguments 99% in stocks and lower fees are worth moving especially when having 1 month out of investing. right now this can be very high cause the markets are booming a bit….

Cheers, Klaus

Hello Mr Poor Swiss,

currently i´m with VIAC (SUSTAINABLE 100) and quite happy with them. I also think there will be not a big difference. Ok lower fees and maybe more gain because of higer stock percentage but on the other side the risk of losing profit during the outage of 1 month.

VIAC has 2 advantages vs FP:

– chat functionality and

– so more responsive support staff

FP is not planning to implement this in the near future.

But anyway, i´m curiuous how FP will develop in the future and are there any experiences about their performance?

Kind regards, Klaus

Why are bank third pillars, generally better than insurance companies?

Hi,

With an insurance 3a, you will have to pay for the premium of the insurance itself. With a bank, you get to keep all your money.

Also, with banks, you get much better investment options like Finpension and VIAC. I am not aware of any insurance that will let you invest in low-cost funds with up to 99% of your money.

Hey Poor Swiss,

this article, or the previous one about third pillar, made me investing in finpension 3a. It was a great choice so far. Thanks again!

Do you consider writing an article about an upcoming crash and how to behave before and during one? This could be interesting since the internet is full of articles talking about this topic recently. Your opinion would be highly appreciated.

Have a great day :)

Hi DB,

Congratulations on choosing Finpension!

I have an article on how to invest during a bear market.

But except for my article about opportunity funds, I have no articles on preparing for a bear market. I will put this on my list.

Thanks for stopping by!

great article.

which of these offer capital protection ?

and whats your view on zurich vs swisslife for pillar 3 a & b

Hi Yasin,

No third pillar invested in stocks will ever offer capital protection.

I have no idea about Zurich vs Swisslife for third pillars. Both of these are insurances are not bank third pillars. I do not recommend third pillar life insurance because it’s too expensive for the life insurance premium and the returns on your money are extremely low. If you actually need life insurance, take a proper life insurance, not one linked to the third pillar.

What about Frankly?

I have a review of Frankly where you can find my thoughts on it.