Should you sell stocks or bonds in retirement?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

If you are planning to live off your investments in retirement, you will have to sell some assets to generate cash flow. But, should you sell stocks or bonds in retirement?

In this article, we are going to compare a few strategies to selling assets in retirement and see which one performs better. By the end of the article, you will have a good idea of what you should do once in retirement.

The simulations

To find whether we should sell stocks or bonds in retirement, we will simulate multiple retirement scenarios. And for each of these scenarios, we will vary the strategies.

I can see three main strategies for retirement:

- Sell stocks only

- Sell bonds only

- Sell based on asset allocation

We will compare these three strategies under different scenarios. For the first two strategies, when the stocks or bonds are exhausted, we will start withdrawing from the other assets.

For all my simulations, I will use historical data for US stocks, bonds, and inflation. This data covers the period from 1871 to 2024, with monthly returns. To start with, the portfolio will not be rebalanced at all. If you want to know about my simulations and date, you can look at my updated results for the Trinity Study.

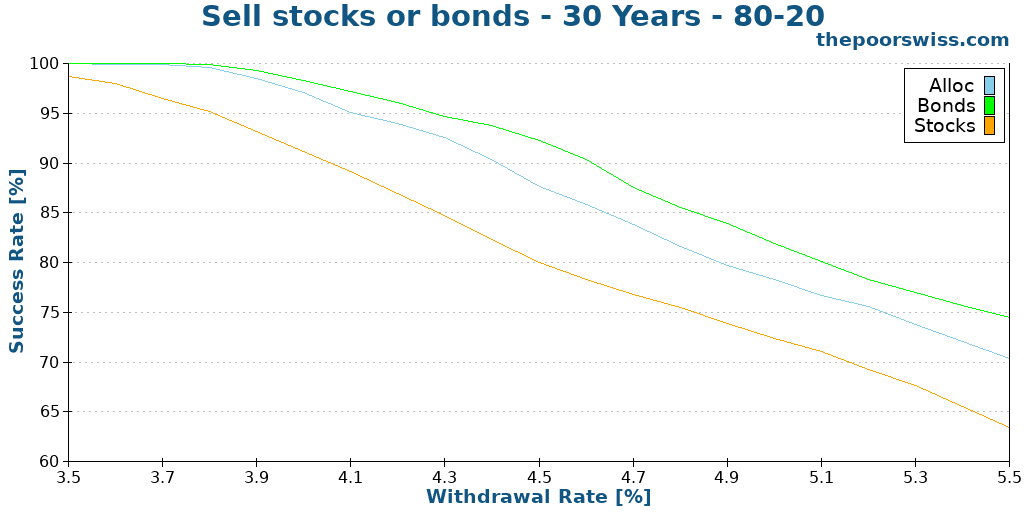

80/20 Portfolio

First, we can start with a portfolio with 80% stocks and 20% bonds. We will see what happens for 30 years of retirement when we sell only stocks or bonds. As usual, we look at the success rate, which is the probability of having more than zero at the end of the retirement period.

Even on a retirement of 30 years, the results are quite interesting. I was no expecting such a significant difference between the different strategies. At the famous 4% withdrawal rate, the difference is already more than 5%.

The worst strategy is, by far, selling stocks first. The standard strategy of keeping allocation is between both. And the best strategy is to sell bonds first. When we think about it, this makes a lot of sense. Stocks are excellent at providing high returns in the long term. And bonds are good at reducing volatility in the short term. If we sell stocks early, we are losing their potential. On the other hand, by selling bonds and slowly reducing them, they have already achieved their goal of protection at the beginning of the period.

In fact, selling only bonds or selling only stocks is the same as an equity glidepath. An equity glidepath will change allocation slowly in retirement. And the equity glidepath that works best is a glidepath where stocks allocation increase over time in retirement. So, by selling bonds only, we are doing an equity glidepath, but with a monthly step based on withdrawal rather than being fixed by allocation.

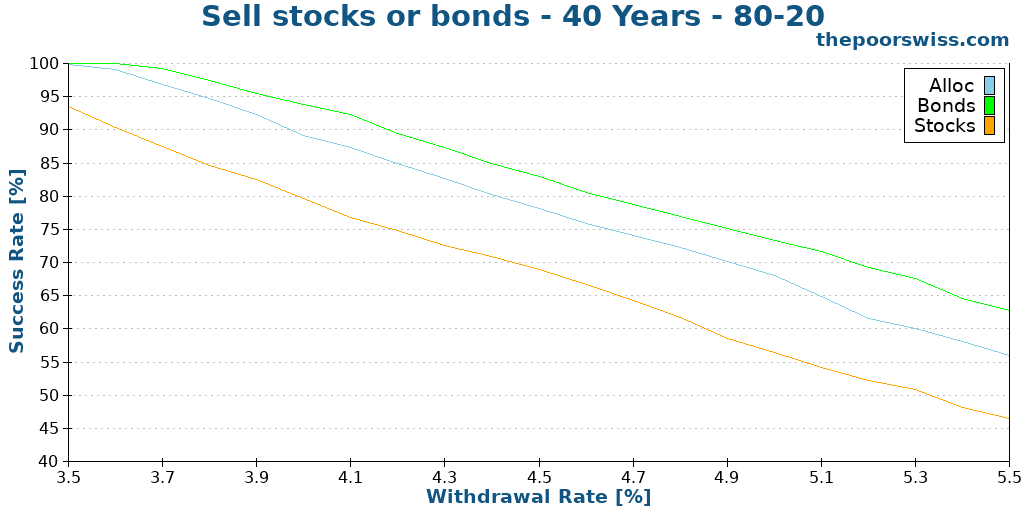

We can also continue looking at 40 years of retirement.

The results are quite similar. The strategy of selling only stocks is becoming significantly worse. And there is still about 5% improvement by selling only bonds.

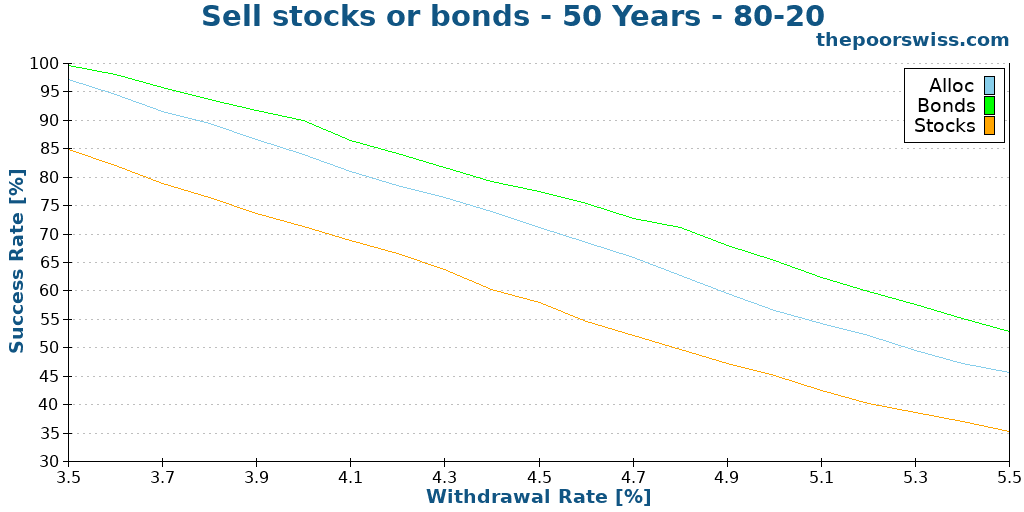

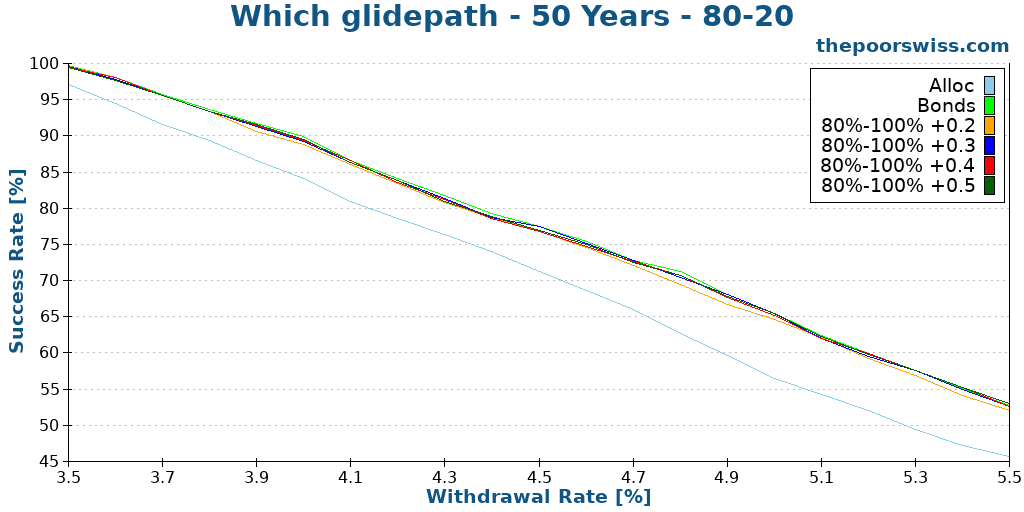

Finally, we also look at the same portfolio for 50 years of retirement.

Again, the results are similar and expected. We can see that selling stocks is a terrible strategy. And selling only bonds in retirement is a great strategy. Adding a 5% success chance is a nice improvement.

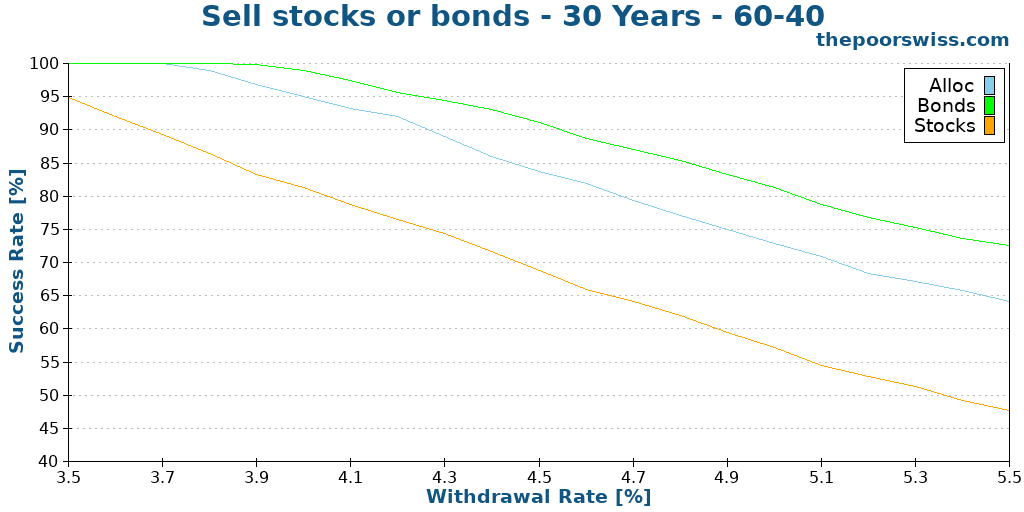

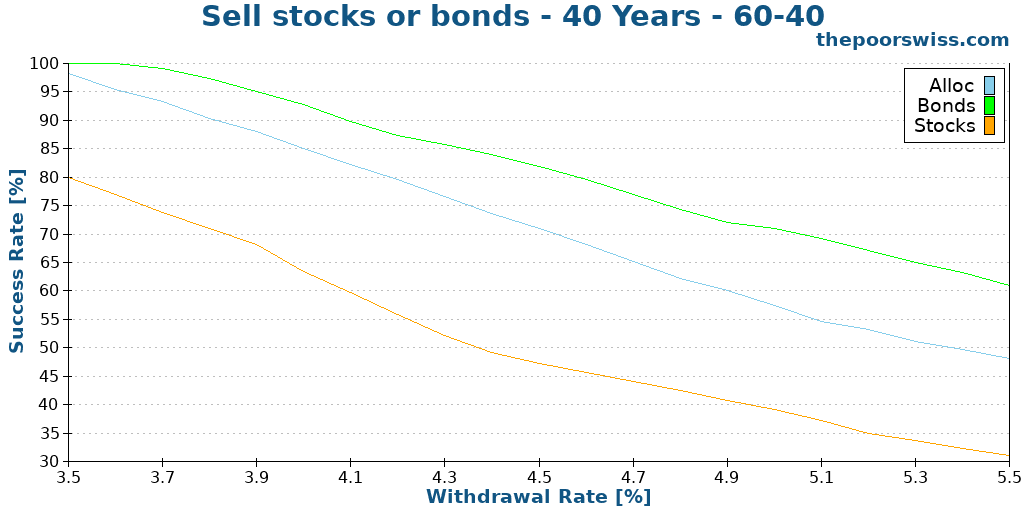

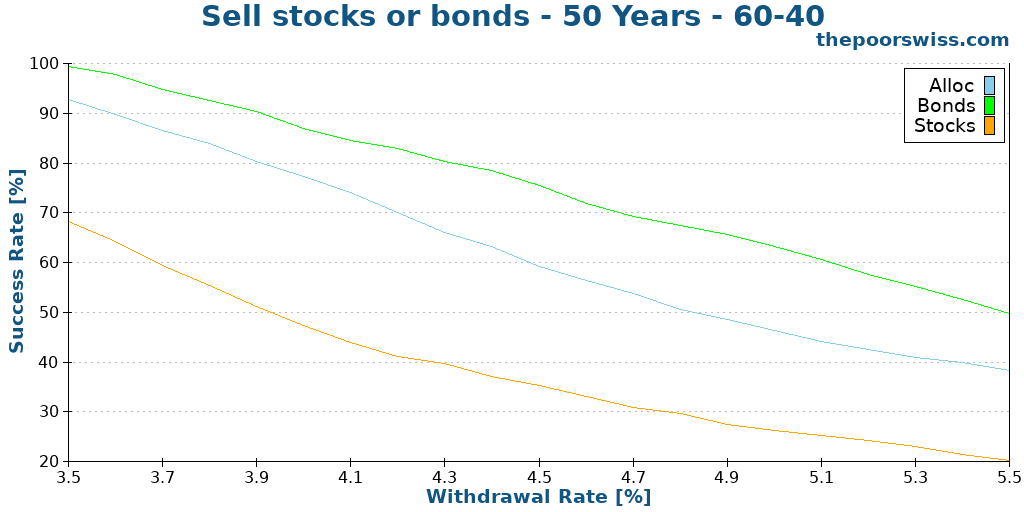

60/40 Portfolio

We should see if the same is valid for other portfolios. So, we can use the popular 60% stocks and 40% bonds as another example. We will start again with 30 years of retirement.

Again, the results are quite interesting. Since we have fewer stocks to start with, selling stocks only proves a terrible strategy. On the other hand, on this strategy, selling bonds only shows a significant improvement over the standard selling based on allocation. So, we can draw the same conclusions for a 60/40 portfolio than we do for a 80/20 portfolio.

We continue with 40 years of retirement.

Again, the differences between the three strategies are quite significant. In fact, they are more pronounced than before. We can get close to 10% improvement by only selling bonds, rather than selling both. And selling stocks only is really detrimental.

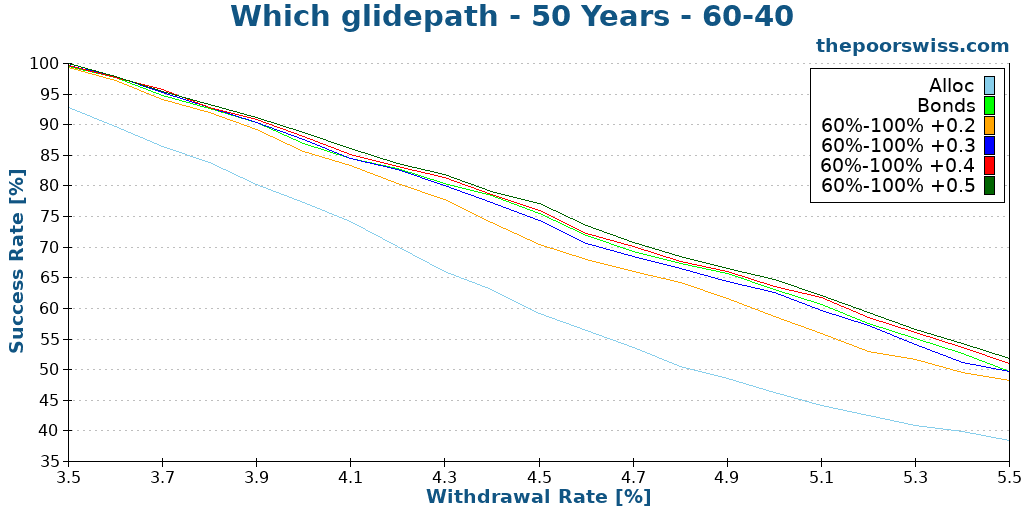

Finally, we can see what happens over 50 years.

Again, the differences are getting even more significant. We can get a significant improvement by only selling bonds.

On the 60/40 portfolio, selling only bonds is really better than the other strategies. You can gain up to a 10% success rate.

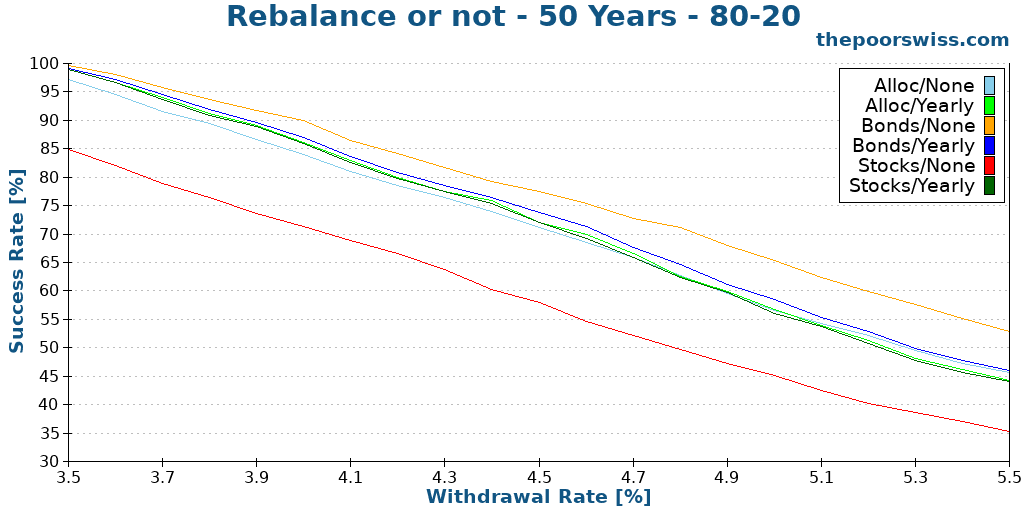

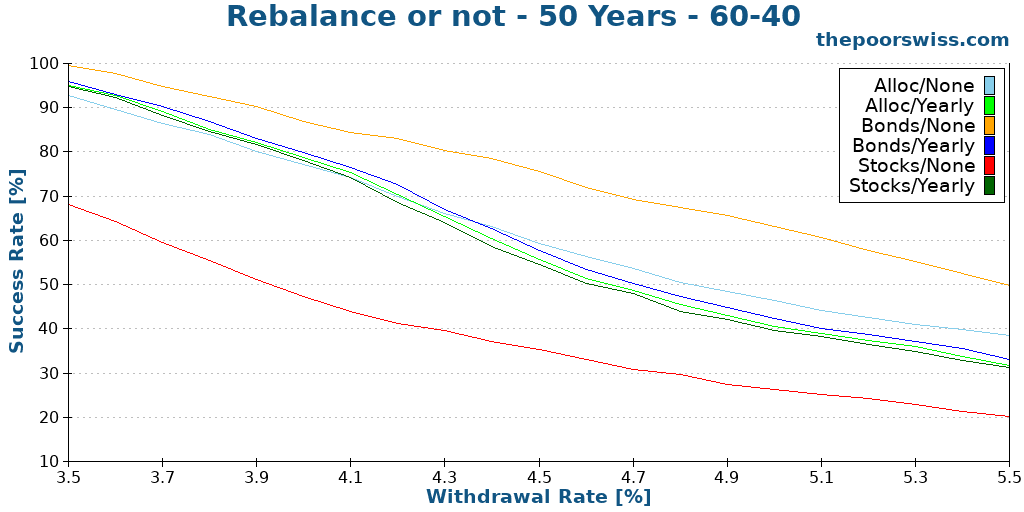

What about rebalancing?

So far, we have entirely ignored rebalancing because it would negate the effects of selling only stocks or bonds, since we would sell assets and then buy them back. At least, monthly rebalancing would entirely negate the effects of the glidepath. But maybe, yearly rebalancing could work?

We will directly start our simulation with 50 years, and we compare 6 strategies this time:

- Using the portfolio allocation to sell, with and without rebalancing

- Selling bonds only, with and without rebalancing

- Selling stocks only, with and without rebalancing

We can start comparing these strategies on the 80/20 portfolio.

As expected, rebalancing mostly cancels the glidepath of selling only stocks or bonds. We sell something every month to buy it back every 12 months. The best strategy remains the strategy where we only sell bonds. If we rebalance, it is still better than the simple strategy based on allocation, but the difference is not very significant.

We can also see whether that it true for the 80/20 portfolio.

Again, the results are similar: rebalancing does not work when selling only stocks or bonds. Selling only bonds remains the best strategy.

Overall, if we want to increase our chances of success in retirement, we are better off with selling only bonds without any rebalancing.

Comparing with equity glidepaths

Since selling only stocks or bonds is a form of glide path, we should compare it with the previous glidepath we have discussed. In this case, we have already seen that selling only stock is a bad idea (like a reverse glidepath), so we will compare selling only bonds with multiple glidepaths.

These results are quite interesting. Most glidepaths have about the same success rate. What is fascinating is that our simple strategy of selling only bonds works as well as the other strategies. But for most investors, it is much simpler to simply sell bonds rather than to adapt the allocation over time. So, we have a simple strategy that is as good as more complex strategies.

We can also verify how this works for the 60/40 portfolio.

In this case, our simple strategy to sell only is not the best. However, this strategy is not far off the best. A fast glidepath with a 0.5% step would be slightly better but would also be much higher maintenance and would get less than 1% extra success rate.

These two comparisons show that selling only bonds is an excellent strategy for retirement. And it is actually better than standard equity glidepaths.

Conclusion

Overall, should we sell stocks or bonds in retirement? The response is simple: We should sell our bonds first. Since bonds are better for the short term and stocks better for the long term, it makes sense to sell bonds first (until depletion).

This strategy works quite well and significantly improves the success rate in retirement compared to selling based on the portfolio allocation. Additionally, this also works as well as more complex equity glidepaths. So, if you have bonds in your portfolio in retirement, it makes sense to consider selling only bonds (or mostly bonds).

On the other hand, selling only stocks makes no sense. Since stocks are here for long-term returns, selling stocks early only reduces our chances of success.

If you are interested in improving your chances of success in retirement, you may want to read about whether being flexible in retirement can help.

What about you? What do you think about this strategy? Are you planning to hold bonds in retirement?

More reading

Sequence of Returns Risk can ruin your retirement

Protect your retirement. Learn what Sequence of Returns Risk is and how a market crash early in retirement can destroy your portfolio.

Some extra income in retirement goes a long way

Planning to retire early and looking to increase your chances? Would income in retirement help your chances of success? We do the test!

9 Reasons to Aim for Financial Independence

Why pursue Financial Independence? Discover the benefits of FIRE, from freedom and flexibility to reducing stress and owning your time.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

You have done an excellent job making the relatively complex topic of the glidepath strategy easy to understand and implement from a theoretical perspective. Your demonstration that a simple glidepath approach (gradually selling 20% of bonds in an 80-20 portfolio until depleted over a little more than five years, to navigate the most critical early retirement risk period of adverse sequence of returns) is indeed as effective as more complex strategies. Congratulations on this insightful finding!

Your article immediately triggered me to consider how to develop a practical plan for Swiss FI seekers. Here are some of my thoughts:

• Bonds should be denominated in CHF (or CHF hedged) to avoid exchange rate volatility undermining bonds’ stabilizing role.

• Bonds need to be diversified and issued by institutions or companies rated at least investment grade to minimize default risk.

• The ETF’s duration should be short to limit sensitivity to interest rate changes.

The inevitable consequence of these criteria is a relatively low expected yield (my gut feeling is around 1% annually) and therefore, the bond ETF(s) chosen (since selecting individual bonds would be difficult and time-consuming) must have a low total expense ratio. Given this, I searched for ETFs meeting most of these conditions and found….nothing. The closest was Vanguard Global Aggregate Bond UCITS ETF – CHF Hedged Accumulating (VAGX), but its average duration of 6.3 years makes it vulnerable to interest rate hikes, which could significantly reduce its value.

What would you recommend to Swiss investors looking to implement the simple glidepath strategy you have shown to be quite effective? Would picking individual bonds be the best approach?

Thanks and best

Marco

Hi Marco

Thanks for your kind words.

I agree with your thoughts. We unfortunately do not have access to great bonds in Switzerland. If used only as a glidepath, I would think that the iShares Swiss Domestic Government Bond 0-3 ETF is our best bet. Its returns have been bad (which makes sense because of negative interest rate), but it is short duration. The 3-7 variant is likely slightly better but not great for short-term as you pointed out.

Picking individual bonds is tricky, I am not sure I would recommend it.

Another option is to hold cash instead of bonds. In Switzerland, cash has sometimes performed better than bonds. It’s not ideal.

I don’t have a good solution to this solution, I am afraid.

thank you so much for all your work. It is really amazing what you are doing.

My mom is thinking in retiring this year, and she has 750K CHF. She is moving to the south of Spain where is cheap, house already paid there on the coast close to Malaga. We invest in Interactive broker, my idea was to have 90% in Stocks (ETF SP500 CHF from UBS) 3% Cash 22.500, (estimation of expenses living like a queen in spain) and 7% in US Bonds that pay around 4% of interest. do you think is correct? i would rebalance every december. or should we use a 80/20 stock/bonds ratio?

Hi Jean Pierre

I can’t really say if the ratio is correct because it depends mostly on your mom. At first sight, it looks a bit aggressive.

However, I would be careful with a few points:

* US Bonds does not seem great because of USD/EUR risk, what about EUR bonds?

* Have you considered taxation in Malaga?

Hi Baptiste, in the last paragraph before the conclusion, you write: “These two comparisons show that selling only stock is an excellent strategy for retirement. And it is actually better than standard equity glidepaths.” I think you meant “selling only bonds”, no? This message is what I got from this article, and it came just in time to save me from plundering my Roth IRA to buy a car (I’m in the US). Thank you.

Hi Birgit

Good catch and bad typo from me. You are absolutely right; the phrase was entirely reversed in meaning.

Hi Baptiste,

Thanks for sharing the interesting article!

I understand that selling stocks should generally be avoided. But what about not selling them at all?

Behind this slightly provocative question is a thought I’d like to explore further.

Many of us use IBKR as our broker, and IBKR offers the possibility to take out a margin loan.

In retirement, this feature could potentially be used to access funds without selling any assets.

What are your thoughts on this approach?

I’d be really curious to see how the numbers play out.

Thanks again and best regards,

Loïc

Hi Loïc

This is a very fair point, actually. You could use a margin loan in some specific cases to help with your retirement changes. You cannot use it for the entire period of course, but using it to fund a part of your spending may be a great idea. This was tested by Big ERN (here) and showed promising results.

I never did the simulation myself, but that’s a fun idea to try out. The problem is I do not have fully historical data on margin loan interest rates. I could probably infer them from bonds.

This is a very interesting concept.

What about borrowing against stocks if and only when you actually retire and the market is doing badly ….indeed to mitigate the sequence of returns’ risk?

Does IBKR grant loans in CHF and what is the interest rate compared with the USD?

Loans in CHF are usually much cheaper than loans in USD, so it may be a good option for us. The problem is indeed timing, but I think it would likely make sense to optimize based on market and only use margin loan to optimize.

For the moment I have 100pc in stocks (80pc SP500 and the rest in SMI, SPI and a Bitcoin ETF) and I’m between 2 and 4 years from retirement. I will have a private retirement pension from an international organisation which should cover my basic expenditure. Nevertheless I was thinking I should perhaps now start to build up some alternative investments in the 2-4 years before retirement. What would you recommend? I had thought about a gold ETF, but perhaps bonds might make more sense, reading your article. If so, which bonds would you recommend? If I intend to retire in Switzerland then I suppose it would have to be a Swiss bond or hedged to CHF but my feeling is that returns in CHF are very low indeed. Is there a convincing argument not to have 100pc in stocks, especially as I have held most stocks for over 15 years?

Hi Max

Thanks for sharing.

Currently, Swiss bonds are bad, unfortunately. I would rather hold cash than bonds at this point. Gold may be a good alternative currently although we don’t know where it’s headed.

You don’t need to have bonds. I only own stocks (except for second pillar) and we plan to keep that in retirement as well. So, if you only have stocks and can handle the volatility, you should be good. This is especially true if you are going to have a pension (you can take more risks outside the pension).

Thanks Baptiste for your reply and insights.

In addition to a gold ETF, maybe I will consider increasing my exposure to CHF through the SPI or SMI to give added protection against a possible continued decline of USD (but how far can it go and will it remain structurally weak?) especially during the first few years of my retirement. Btw, my pension will not be in CHF (but in Euros) so this gives me an added incentive to rebalance from USD to CHF.

Thus actually brings me to the question of ETFs hedged in CHF. Have you made any comparative studies between yields in CHF of SP500 ETFs (taking into account the USDCHF exchange rate) and SP500 ETFs hedged in CHF over the medium to long term?

Regarding hedging, it is generally commonly believed that it works well in the short to medium term but is not great in the long-term.

In your case, it does make sense to try to shift a little more to CHF since your pension will be in EUR, that’s a fair point indeed. In the end, it will also depend on your risk capacity and on your margin of safety.

Thanks a lot Baptiste, you show-cases the answer to a question that I posed myself for a while. My concern would be mostly of a psychological one.

When I stop working and no longer get a regular income through my salary, in an event of a crash, I would probably get stresses out when I see my stocks decrease by 50% or more. So even if from a rational/historical point view it would be best to hold a maximum of stocks. Therefor I might rather tend to increasing my share of bonds that are less volatile and therefore sell at least some of the stocks.

Hi Barbara

That’s a very good point. Mathematically, everything is easy. But in practice, you have take emotions and psychology into account and then it becomes much more difficult. I think I will be fin ein retirement with 100% stocks, but the only way to find out is to actually retire with the that allocation.

It’s very important to know oneself. You are much better off selling bonds than panicking and selling all your stocks to prepare for something that may not happen and ruin your retirement.

The problem with a high stocks allocation is the SORR. I think it makes sense to have 3-5x yearly expenses in cash shortly before retirement, and for the first 5 years in retirement, so draw from cash instead of having to sell stocks in case of a market crash. You have to survive the first approx 10 years in retirement (avoid withdrawals when markets are down a lot).

These days, cash are almost the same as bonds. So having an allocation to cash and selling/using it for the first years makes sense. But that also means that you are lowering your retirement returns, everything has drawback. But it’s indeed a good idea to play it safe.

Isn’t the title question in itself not flawed?

Basically you are asking if selling stocks at the point in time when cash is needed is the best option. Regardless of current market conditions, and independent of how long that stock has been held.

The alternative being that stocks are sold before the time of need and kept in a second pot with less risk exposure.

Understanding that “buffer” time period and reduction in risk exposure might be worthwhile to look into.

That said if stock is sold at regular intervals at the time of need (e.g. once a year for many years) perhaps that already addresses market volatility.

Hi capmac

I do not understand why it’s flawed. When you have a portfolio with stocks and bonds and you need money, you have to choose between stocks and bonds, no?

Of course, you have to sell, but you can schoose your asset class to sell.

I meant the question is too indirect, perhaps? There is an overriding question.

Do you keep a second “buffer” pot for cash needs, or do you sell stock at the time of cash need, is the question you should be asking in my opinion. That second pot would be regularly topped up by selling stock, and can hold bonds or cash. Also bonds are considered to be short to medium term assets, and are sometimes used to cover the portion of a portfolio to be accessed in case of emergencies.

I think we are not talking about the same thing.

My article has nothing to do with buffers. If you have a portfolio of stocks and bonds in retirement, what should you sell first to have cash to spend? The idea is to sell things each month to have cash to pay your bills, month after month.