February 2025 – Back from China

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

At the end of last month, we left for China to visit our family. It was the first time we went to China with our son. Our goal was for him to meet his uncles, aunts, and cousins. And my wife was also looking forward to seeing her siblings again. It was great to meet everybody again, but exhausting.

Financially, it was a good month. Our expenses were slightly high because of the hotels in China. But our income was also significantly higher than average because of some shares I received. So, we managed to save about 80% of our income.

February 2025

The main event in February was being in China for almost the first two weeks of the month. We went there to visit our family. Our son was happy to travel and meet his cousins, uncles, and aunts.

Obviously, there is also a downside to travel with a 3-year-old. The first flight was starting at noon and our son only slept 1 hour out of 13 hours. This was quite exhaustive for everybody. On the other hand, he did not cry nor make any tantrums, he was just quite demanding. On the way back, we flew during the night, so we could all get a few hours of (bad) sleep.

We visited multiple cities: Hong Kong, Shenzhen, Ebu Zhen and Xia Men. The idea was to see people in different places. We only regretted going to Hong Kong. In Hong Kong, everything is small and most places were closed because of the Chinese new year. If you add the lot of people on top, this was not a great experience this year (except for the fireworks!). We had a better experience in Shenzhen. Next time we go, we will limit the cities we go to.

Whenever I could, I used my Neon card to spend money in China. But China is not credit-card-friendly. It is very rare to be able to use a credit card. They much prefer using WeChat, but WeChat is not foreigner-friendly since we cannot use our cards there to charge money. In our case, this is fine, I withdrew cash, gave it to my wife who put it in her account and then use Wechat to pay for almost everything. If you go there alone, I would recommend preparing some cash and be prepared to not be able to pay in some places because some places are WeChat-only.

I took time this month to do our taxes. Our personal taxes are simpler now that we have the LLC since everything is separated. Normally, we should end up paying about 3000 CHF less for 2024 than for 2023. This is mostly because the income of the blog is only partially extracted. On the other hand, we had lower deductions this year because we did not do anything on the house. Next year may go down even more, since we plan to contribute more to our second pillar this year.

I have taken some time to refresh my disaster file this month. It was a bit out of date. And I needed to upgrade some of my passwords which, I felt, were at risk.

Financially, it was a good month. Of course, we had some extra expenses because of the holidays (mostly hotels and apartments). But we also had significantly higher income because I received some shares at work and my ESPP shares vested as well. As a result, we could save 80% of our income this month.

Expenses

Here are the details of our expenses in February 2025:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 831 | Expected | Insurance for the three of us |

| Transportation | 0 | Lower than expected | Nothing |

| Communications | 20 | Expected | One phone plan |

| Personal | 3863 | Higher than expected | Holidays, kindergarten, courses and more |

| Food | 437 | Expected | Groceries after coming back |

| Housing | 810 | Expected | Power, heating and mortgage |

| Taxes | 1462 | Expected | Only municipality taxes |

In total, we spent 7425 CHF. Without taxes, we paid 5962 CHF. For the holidays in China, we spent 1682 CHF. This was mostly for hotels and food. The plane tickets were paid several months in advance. Overall, we managed not to spend too much this month given the holidays.

As mentioned before, the accounting for the holidays is not precise because my wife paid in yuan everything and I then withdrew money to put back into her account. However, things are so much cheaper in China, we did not spend too much for two weeks in China with our son. And we even booked nice hotels. Otherwise, we could have spent much less, but it was not necessary.

Other than the holidays, there is not much special in our expenses this month. We will soon put our son a second half day in children’s school (kind of school before primary school) because he likes it a lot. This will add 120 CHF per month to our budget.

Our food budget is really low, which makes sense since it is only two thirds of the month. And other categories are not much to talk about.

Overall, I am happy about our expenses this month. Despite holidays, we managed to not spend too much money.

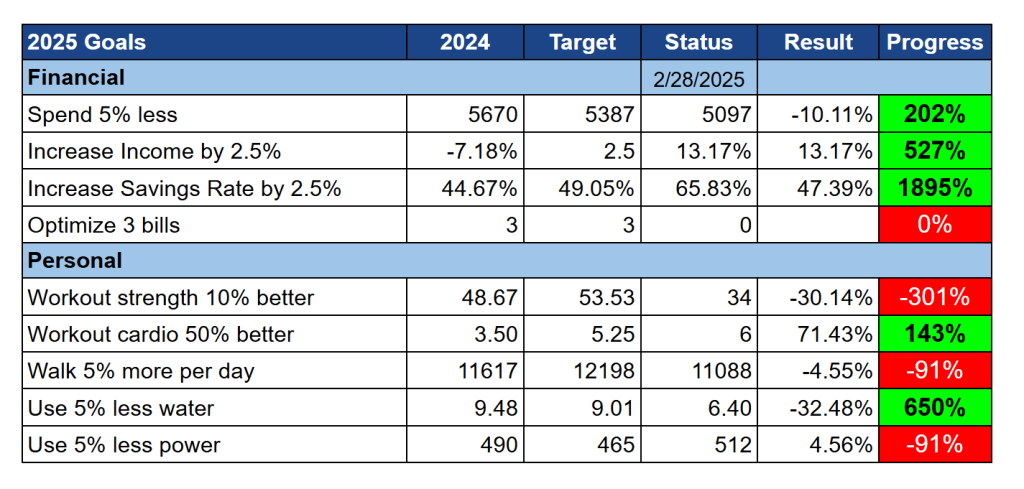

2025 Goals

Here is the status of our goals by the end of February 2025:

It looks like half of our goals are doing well while the other half is doing poorly.

Our financial goals are doing well. Our spending is still below the spending of last year, despite the holiday. So, this is a good thing. Our income this month was excellent, so this makes our average income very high as well. Next month, this will become even better and then this will go down during the year. This also helps increase our average savings rate.

On the other hand, my strength workout training is not great this month. This is simply I could not do any trainings while in China. And since I was sick in January, the average is bad. But I hope to get back in the habit in March. For the same reasons, walking is also below target. We will see if I can improve that in March as well.

Our water usage is really low this month since no water was used while on vacation. On that note, we also changed our shower head to one with should save us a significant amount of water. We opted for one from Gjosa which was heavily recommended. We will have to wait until the end of March to see if it makes any difference on our water consumption. But at least, the feeling of the shower head is good.

I was expecting our power usage to be great this month. But I had the bad surprise to see that this month was actually awful. Despite being 10 days in China, our power usage is the worst we have ever seen. It is 50% higher than our average. We had turned off many things while on holidays, so it does not make sense to me. At this point, I have no good explanation.

Overall, our goals are doing well considering the situation.

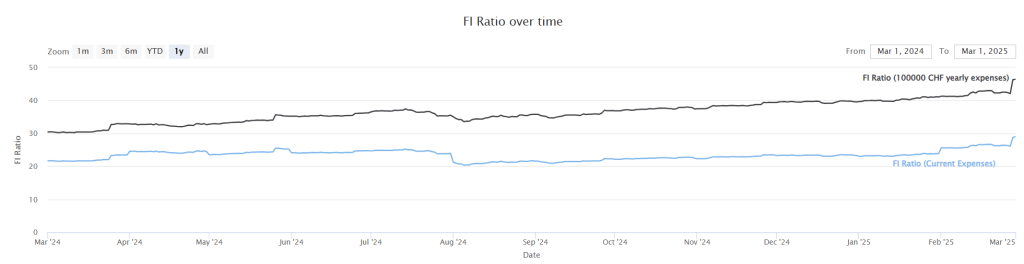

FI Ratio

Here is the progress of our FI ratio as of February 2025:

We had a nice bump in FI Ratio this month. This is due to two factors. First, we saved a lot of money this month. And second, we got a significant yearly payment landing for the blog.

You may have noticed something strange in the graph, it looks nothing like the one from the previous month. Unfortunately, there were two issues in my code for these graphs. First, the formula for the FI ratio itself was plain wrong, making it higher than real. And the average expenses of 12 months which I used was not entirely accurate, causing several jumps in FI ratio.

So, while our FI ratio was getting close to 40% last month, it is now getting close to 30%. The good news is that my projections for time to retirement were not wrong. If everything continues as such, we should reach financial independence in about 12 years.

During this month, I finished my rebalancing over my two brokers. I sold all my remaining CHSPI shares from IB and transferred the proceedings to Saxo. My portfolio is not extremely well-balanced, I will need to buy more CHSPI in the upcoming months. But since I will also invest more into my second pillar next month, my home bias is fine right now.

I think our Fi ratio is doing well, despite the code issues, of which I am not proud.

The Blog

While I was in China, I had limited access to the blog. Fortunately, this year, my VPN worked so I could keep track of emails and comments. This allowed me to not have a massive pile of work when I came back. I know it is not ideal to have to do that while on vacation, but I usually did that in the morning when my wife and son were still sleeping. And it was really nice to come back and have less to do. On the other hand, I could not take the time to update articles, so there was still a significant amount of work that needed doing.

I did some improvements to my free cheat sheet e-book this month. It required a refresh in multiple places. Additionally, I finally translated it to French and German. This is something that had been highly requested.

I also did some improvements to the broker comparison tool. There are now multiple scenarios:

- The standard investing scenario.

- A selling scenario where we only sell.

- A scenario where we invest multiple years for a given goal and then liquidate everything.

- A scenario where we accumulate money until retirement and then withdraw each month to sustain the retirement.

I also added a third pillar comparison tool. I quite enjoy working on these comparison tools. And I think there is value for my readers. I still need to find a way to make them more known by my readers. Please let me know in the comments below what you think about these comparison tools and any suggestions you may have to improve them. I may complete the set with a comparison tool for vested benefits accounts. Talking about some readers, I also feel like I could do some more calculators, such as to compute whether it is worth contributing to the second and third pillars.

I still have not gotten to fill the taxes for the blog. I plan to do this in March. Indeed, I was not really motivated to do it this month and I still have until August to complete them. Furthermore, I would rather not do two sets of taxes the same month.

Even though I do not pay much attention to it generally, I was a bit shocked to notice the traffic to the blog is now down 50% year over year. I do not know what is going on and it may be temporary. I should probably spend time looking at the rankings of my article and try to improve older articles. But I do not think I will have the time to do that in the future.

Finally, I am organizing another meetup for the blog readers in Fribourg. This will be organized on the forums. If you want to join, you can vote on the forum poll.

Next Month – March 2025

We do not have much planned in March, which is good. Financially, it will be a great month because I will receive my bonus. March is generally our highest-income month of the year. I typically splurge a little of this bonus every year. But our savings rate will still be very high.

What about you? How was February 2025?

More reading

Third Year of Blogging – The Poor Swiss is 3 years old!

The Poor Swiss just turned 3 years old! Find out all that happened during the third year of blogging and what will happen in the future.

October 2019 – Holidays

October 2019 was a great month, with a week in Barcelona, Spain, a very nice city!

2018 Goals Review – Too Easy!

Here, I review our 2018 goals. In the end, the goals were too easy and did not require much effort to be reached. We will need better goals.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste

Thank you for a very informative blog. I only started reading it regularly since middle of last year (thanks for pointing me to IB, which I now use as my primary stockbroker, while keeping PostFinance as a secondary).

I trawled also through your updates from the previous years and I still have a question regarding your FI/net worth calculation:

Do you include your equity in your primary residence in the FI ratio calculation in your monthly updates?

I know you may choose to include it or not depending on your plans, but how do you deal with this in your case? (I do not include it in FI calculation because I do not expect a significant downsizing at retirement in terms of property price, so the equity will most likely stay tied up)

Hi Vladimir

I am glad my blog is useful for you!

I do not include my house equity for my FI ratio computation. My rationale is that if I sell my house, I need to find another one or rent out and both will not help FI but hurt it.

I have talked about it here: Not All Assets are Created Equal – Introducing the FI Net Worth

Hi Baptiste

Thank you for the answer. I have the same thinking, if I planned to downsize significantly or to move to some cheaper place, then I would take a portion of equity into account.

Considering that I find the growth of your net worth quite phenomenal. I think in March 2020 you were somewhere around 300K, compared to myself: I bought an apartment at that time, my NW excluding it was around 500K at that time, mostly tied in my second house and the 2nd pillar pension). Now you are at around 46% of the FI target with 100K expenses, which translates with 3.8% withdrawal to 100K / 3.8% x 46% = 1.2M

Well done, I am still stuck somewhere around 1.1 M. I did only very little investing though, and until recently we were 1.1x income family.

Hi Vladimir

Some of my growth is due to the stock market since we are heavily invested. But a lot of the growth is due to high savings. We have a high savings rate on a high income. Over time, the place for the investing growth should get bigger, but for now we are quite driven by income.

Hi Baptiste, since a couple of years ago you can link your foreign card to both Wechat Pay and Alipay, it doesn’t work 100% of the times in physical business, but it does for online payments. I paid most of my stuff in China with Neon via Alipay. Check it next time ; )

Thanks a lot for sharing, Tomas. I tried to topup about 5 years ago and it did not work, but I have not retried since. I’ll definitely try again the next time.

Ah, topping up your balance is not possible with a foreign card, you pay directly with the foreign card via Alipay/WechatPay.

Oh, that makes sense. I never tried adding the card of payment! Thanks for the detail.