My 8 Biggest Budgeting Mistakes – How to fix them!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Over the years, I have made many budgeting mistakes.

In this article, I list a few of my big budgeting mistakes. I am talking here about mistakes in the way I did my budget. And I will also talk about spending mistakes. Some mistakes are not a big deal. But some others made me spend too much. Overall, I would be better off if I had known this a few years ago.

You can also find out how I fixed my budgeting mistakes. I have learned a lot from my budgeting mistakes, and I hope you can learn a lot from them too! The idea is, of course, to avoid them now that you of them!

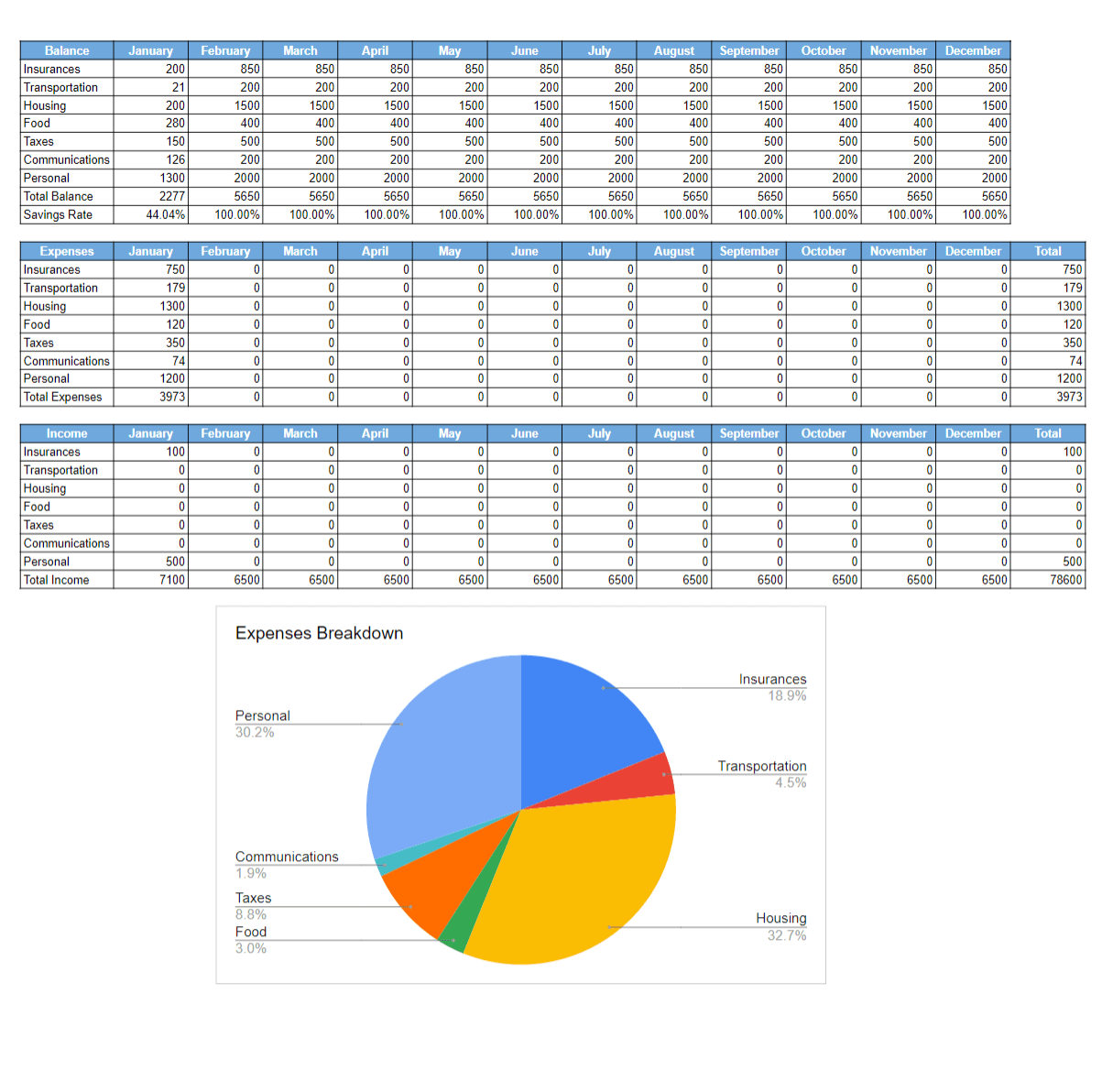

Not considering my savings rate

A simple Google Sheets template to start tracking your expenses and earnings and have an overview of your budget! Know your savings rate without effort!

I have had a budget for all my independent life. I have always kept my spending under control. But, I was primarily considering my income as my limit. I was happy when I could save 500 CHF at the end of the month. It was good at the beginning when my salary was low. However, as my salary grew, so did my spending. I did not realize it. But my lifestyle was becoming increasingly costly. This problem is called lifestyle inflation. And this is something everyone should be careful about.

In itself, it is not very bad. But if your goal is to save some money, you should try to save a specific part of your salary. It is your savings rate. And then, if your salary increases, so should your savings. After I realized this, I started being more frugal to increase my savings rate. I am now able to save much more money each month.

Now, I consider my savings rate as my most essential budget metric. But the exact number you need strongly depends on your goals. Not everybody wants to retire early. You may need a higher or lower savings rate depending on your goals and the time to reach them. The important thing is not to spend all your salary. And not to increase your lifestyle too much when your income increases.

Getting a life insurance 3a

In early 2017, I made a major mistake: I signed a life insurance 3a contract. This was before I started the blog and before I started to learn about personal finance in detail.

Later, I realized the life insurance 3a is a big trap. The returns are bad, the contributions are not flexible, the fees are huge, and you pay a huge premium for life insurance. In the end, you end up losing a lot of money compared to simply getting pure-risk life insurance and a good 3a.

There are multiple ways to deal with a bad life insurance 3a. In the end, we opted for breaking the contract entirely. Once done, the money was transferred to our Finpension 3a account, and it will grow there for about 30 years. The money we lost will be compensated by the fees we save and the superior returns.

Using Swisscaution as a deposit guarantee

The second of my budgeting mistakes was paying for Swisscaution. I did not think enough when I chose to use Swisscaution. I should never have paid them.

In Switzerland, when you rent an apartment or a house, you must deposit a bank guarantee. This guarantee is something like two or three months of rent. It will depend on the owner of your apartment or house. The guarantee is deposited in your name and the name of the owner. The money is blocked for as long as you rent the apartment; in case of damage, you will use it to cover them.

There is another option: Swisscaution. They will act as insurance covering the guarantee. You will pay a yearly fee, depending on your rental price. With that, you do not have to deposit much money in the bank. It sounds good, but when you do the math, Swisscaution is a terrible deal.

Instead of keeping your rental guarantee in a bank with minimal interest, it is placed in insurance with a significant negative interest rate. So why did I take it? I was lazy, and I did not do the math. And I paid the price for it. At least, it was not too bad of a price.

I will never advise Swisscaution to anyone again. And I will deposit a rental guarantee in a bank for my next apartment. I am getting information to see if changing from Swisscaution to a rental guarantee is possible. But it seems very difficult, and I will probably move in the coming years, so it may not be worth it.

Taking an apartment too expensive

My first apartment was a very cheap two-bedroom apartment. I was paying 910 CHF per month, including all fees. It was small but still enough for a single guy. I lived there for around two years. Then, I decided to have one more room for a real office. Since I spend a lot of my time in front of my computers, this made sense. However, this would not have been necessary.

I went on a quest to find a better one. I found a very good apartment. In the beginning, the new apartment was only 1050 CHF per month. It was fair. For 140 CHF per month, I could have one more room. However, the owner would make many improvements and thus increase the price. I hesitated when they told me the new price of 1300 CHF per month. But not long enough. I liked this apartment, so I took it.

I do not regret it since I had a good time. However, I regret having taken an apartment that was too expensive. It was not reasonable for a single guy, especially considering my salary then. Since then, I have reduced my rent to 1247 CHF per month. That is great, but I would have been better off with a cheaper apartment.

Using Swiss Life Select

Another thing I am not proud of is having paid for the services of Swiss Life Select.

Swiss Life Select (SLS) is a financial planning company for those who do not know. They cover insurance, budgeting, retirement planning, and even investing. “Normally,” they do not contact you unless somebody gives them your contact information. They “normally” only work like this. But I have some doubts about this (hence the “).

So, they contacted me and proposed I meet one of their advisors. The first meeting is free. First, they ask you a lot of questions. And then, they establish your financial profile and propose things to improve it. The second meeting with the solutions is not free. You have to join Swiss Life Select. There is a one-time fee of 295 CHF. I accepted their offer.

They proposed I change my car insurance. This I did since it was indeed cheaper than mine. I also agreed to take on legal insurance. I have some doubts now regarding this one. At first, they told me they could help me with my taxes, but they did nothing about this. They also told me they would contact me again to have opportunities to invest in better funds in their bank.

So why am I not happy with them? For several reasons. First, they say they do not get paid on commission. But this is not true. SLS employees are paid based on the products they sell. So they have an interest in selling as many products as possible. Second, they said they would contact me again to offer me some investing opportunities.

They never did! It is probably fortunate since I discovered that their funds are too expensive. If they cared about you, they would offer you low-cost index funds. But they care most about the bonus they make on selling you new products. Third, everything they offered me I could have had from my existing insurance manager. And he is free.

And after this, I found out that the car insurance they sold me was not the cheapest. As for retirement planning, I already knew most of it. And I could have read it on the Internet, again, for free! And finally, they are trying to get as much contact information from you as possible.

I only gave them the contacts that were willing. I will never provide a contact number from a person without asking first. So, in the end, only a few people accepted. And the SLS advisor was not too happy about it.

Overall, their service costs 295 CHF. You can check insurance offers online with many websites today. Even if it is a pain, it is free. And a lot of insurance managers will offer this service for free. And you should not invest through their funds. You should invest in low-cost index funds. I should have thought longer about the real value of their service.

If you want to know more, I have an entire article on why you should not use Swiss Life Select.

Not correctly budgeting for vacations

I am not very good at budgeting for holidays.

And I am not very good either at being frugal when I am abroad. It is not a winning combination. At least, I budget the transportation and the lodging very correctly. My problem is that I do not have a budget when I am there.

And my biggest issue is when I am in a country cheaper than Switzerland, like China. I tend to consider everything cheap and do many small expenses. Unfortunately, these small expenses add up. And I only realize this when I am back at home doing the total of my costs!

For our next vacation, I will make a better vacation budget. I will not only carefully budget early expenses (planes and hotels). I will also plan a budget for the expenses while on vacation. It means planning how much we can spend on food, gifts, trips, and activities. It should let me avoid having big surprises when finalizing the budget after the vacation.

Not considering big expenses

Many expenses come as a hefty bill.

For instance, I pay car insurance only once a year. It is the same for my home insurance or my legal insurance. And the same with parking at work. I pay the awful Billag tax every year as well. I pay the power bill every three months.

There are also a few months when I do not pay taxes. I tend not to plan for them. Sometimes, I have an excellent month with none of these expenses. It makes me believe my month is very good, and I spend more. The problem is that they are regular expenses, and their fees should be spread over the entire year.

The easy solution for this is to spread the expenses for several months. But I do not like this since the budget does not fit reality. Now I am saving much more than before. This has improved this problem. I am more careful. Also, I am trying to think in advance of possible expenses like this. But I do not yet have a perfect solution to this problem.

Spending too much on computers

The last of my budgeting mistakes is spending too much on computers. For many things, I am pretty frugal. For instance, I spend little on clothing, going out, and groceries. However, I do have a problem with spending on technology. I am a big geek for computers and servers. I have played computer games for more than 15 years. And I also like home automation. All this did not come cheap at all.

My desktop computer is a large tower case with two computers inside, and I have three monitors. Together, it is probably worth something like 5000 CHF. And this is not the worst. I also have servers. I have a very tall computer rack (240 cm tall) with seven servers and networking utilities.

(I am not kidding, I have this in my office, at home)

I have probably spent around 6000 CHF on these servers. Also, I have a custom media center, a large flat-screen TV, and a home cinema system. For probably 2000 CHF more. Next to this, my home automation system is much cheaper. I probably spent about 1000 CHF on it. Aside from this, I have a closet full of pieces and components.

And everybody thinks I am crazy, but I can live with this!

Then I realized how much I was spending on these items and how little I was saving. It made me focus on my budget much more. So this is not so bad. And also, managing my ten computer installations was taking too much time!

I do not regret spending money on this. It has been and still is a lot of fun. But I went a bit crazy about it. I have a lot of material that I do not use today. And it takes a lot of room! I am planning to downsize a bit. I will reduce the number of servers I am using. For this, I will dismount a few servers and sell the parts. This will save a lot of room and maybe bring some money. If possible, I may also go for a smaller computer rack. And I have to go through my computer parts stash to save room.

Conclusion

As you can see, I have had my share of budgeting mistakes. Since this blog is about transparency, I wanted to share them with you.

I have learned a lot from my mistakes. In the future, I will focus more on my savings rate. And I will think longer about the value of some things I purchase. I should only buy things I will use and services of real value.

I do not have a problem with my budgeting mistakes. They taught me a lot. Moreover, I was smart (and lucky) enough not to get into debt. So my mistakes can seem of lesser importance to some people. That is a good thing for me!

My budgeting mistakes were not my only mistakes. Recently, I wrote about my nine biggest investing mistakes. Everybody makes mistakes. The important thing is to learn from them. And never repeat your mistakes.

What about you? What big budgeting mistakes did you make?

More reading

What’s the Time Value of Money?

Money today vs tomorrow. Understand the Time Value of Money (TVM) and why a franc today is worth more than a franc next year due to inflation.

How to manage your finances as a couple?

Money and Love. Discover practical tips to manage finances as a couple, from joint accounts to splitting bills, and avoid arguments about money.

6 Steps towards a Solid Budget can make you Debt-Free

Do you want to become debt-free? Find how to work towards a solid budget to help you become debt-free!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Thank you for sharing this honest blog. I just moved to Switzerland in June 2025 and your blogs really helped me. But sadly I didn’t find out earlier so I already fall for Swiss caution as deposit guarantee but at that time, I didn’t have enough money also. So it is fair.

This year 2026 is my first tax return year (Permit B) and I am looking for tax advisor. I found out Clark with offer for the professional preparation of tax return with price CHF 99.- for single persons plus potential extra charges for transactions (till 10 transactions, no extra charge).

Can you provide reviews for tax advisors also?

Hi Coco

I am glad you find my blog useful. Swisscaution is not too bad, there are much worse traps (3a life insurance!).

I have never had a tax advisor, so I don’t think I would be capable of doing reviews for tax advisors. My recommendation is to learn to do it yourself. Maybe you can use a tax advisor for the first year and then do it yourself, it’s really not that complicated.

Very helpful Mr. The Poor Swiss! Btw thanks for using a rawpixel image! (calculator)

We have a ton more of blog-worthy photos for free here > https://www.rawpixel.com/free-images?sort=curated&premium=free&page=1

Enjoy :)

Hey you’re using a rawpixel image, COOL! (biggest mistake banner)

We got heaps more at http://www.rawpixel.com you should check out. Very useful for more of your amazing blog posts like this one :)

Enjoy!

Hi Nica,

Thanks a lot of the pictures. I think I got them from Unsplash (or maybe pixabay).

They are really nice :) It’s really useful for people like me who are really dumb for pictures ;)

Keep up with the awesome work!

Nice server rack !

And that’s a lot of (unused ?) CPUs and GPUs !!! Feels like a photo from Digitec’s stock hahaha. Might want to sell all the extra parts (before your extra parts become too much obsolete and loose value unlike your ETFs ;-) ) and buy more ETF shares ! Get some place back and super easy “free” money than can go to your net worth ! That could be a motivation for eliminating what you don’t need. ;-)

For the big expenses, I also had the same problems as you until the beginning of the year when I starting getting into “PF/FIRE” spirit & community and discovered all of this world and I started using YNAB and now few months after, I became completely addicted to this great piece of software and wonder how I could make it until now with zero budgeting done until this year. Now I just split big one time expenses in twelve months and I set monthly goals or target date goals with the exact month date I know I’m gonna need to pay that specific big expense. And forecasting by creating in advance future bills/transactions with recurring dates (monthly, annually and so on…) for example. That’s so convenient and everything became so easy. At least for the bills that you can know you’re gonna get. My financial life changed completely because of this software and mostly because I finally started budgeting. I don’t remember if you’re using it or no or another budgeting software.

Thanks Cashfl0w :)

The boxes inside the shelf are all empty ;) But I always keep the boxes in case I sell something later. I’m not that crazy to have so many unused parts. However, to save power, I’ve currently shut down 2 servers. I plan to strip them and sell the parts. I’ve also found a good pile of things that I’ll be able to sell. I found some things that I would never have thought I still had haha. Yes, it’s a good motivation to transform into a better value.

Yes, if you can split the big expenses in twelve months and create goals for big expenses, it’s a really good way. I’m not using YNAB but another software: budgetwarrior (for geeks haha). I plan to talk about it in a future post. The most important is, as you discovered, to have a budget. It can make a very big difference.

Thanks for stopping by :)

Thanks for sharing this post. I didn’t know about those Swiss scams. Someone from a similar financial planning company keeps calling me and trying to get me to use their services. I am glad I said no.

Also, cool computer room :P

You’re welcome :)

They are not really scam, let’s be honest. They are just not in the best interest of people.

In switzerland, it’s terrible how many people are trying to get you, especially for insurance. It’s a real jungle.

I like my computer room too, but a bit crazy haha