US ETFs are the best ETFs for Swiss investors

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I mostly invest in US ETFs, and I have recommended these ETFs many times on this blog. I consider US ETFs to be the best available ETFs. I have talked several times about what makes them great in various articles. But since I still get many questions, I will go into all the details of these US ETFs.

I am talking about Exchanged Traded Funds (ETFs) that invest in the United States. I talk specifically about ETFs from the United States. What matters here is the domicile of the ETF. This is more important than many people realize.

So, here is what makes these US ETFs great.

Availability of US ETFs

First, we need to address the issue of the availability of US ETFs, or lack thereof.

If you are in the United States, you will not have any issues. However, if you are in Europe, this is another story. Indeed, due to European regulations, many countries lost access to US ETFs.

In fact, in 2018, all the countries part of the European Union lost access to US ETFs. This is due to the PRIIPS regulations. These regulations are part of a bigger package known as MiFID II. These laws force the fund providers to provide a Key Investor Document (KID) in the investor’s language. And so far, US fund providers have not provided them, and they are unlikely to do it. So, for now, European investors cannot invest in US ETFs.

In theory, these laws protect investors by providing them more information on the instruments they are using. However, in practice, they are only here to force people to invest in European funds.

However, Switzerland is not part of the European Union. Therefore, Swiss investors still have access to US ETFs. However, this may change when the Swiss equivalent of the European laws enters into effect. Now, it is not entirely clear if this will apply to foreign brokers (like Interactive Brokers) or not. But for now, we are free to use these ETFs.

I believe these restrictions will not apply to execution-only brokers like Interactive Brokers. So, they should still be available in the future.

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Furthermore, not every broker provides us with access to these ETFs, even though they could do it by law. For now, only foreign brokers, like Interactive Brokers, give access to these ETFs. This is good since Interactive Brokers is the best broker for Swiss investors.

If you want more information on these regulations, you can read my article on the availability of US ETFs.

US ETFs have lower fees

The first advantage of US ETFs is that they have lower fees than their European alternatives.

What matters to us is the Total Expense Ratio (TER) of the ETFs. The TER is the total fee you pay for holding the money. This fee is expressed in percentage and is removed from your money over the year. So, if you have a TER of 0.1% and 100,000 CHF in the fund, you will lose 100 CHF each year to fees.

Since you will pay the fees each year, it is important to optimize them. If you are a passive investor, ongoing fees are the most important cost you can optimize. So, it is important to do it well. And the more money you have in the funds, the more fees you will pay.

We can compare a few ETFs to see the difference in fees:

- Vanguard S&P 500: The US ETF (VOO) has a TER of 0.03%, while the European ETF (VUSA) has a TER of 0.07%, twice as expensive

- Vanguard World: The US ETF (VT) has a TER of 0.08%, while the European ETF (VWRL) has a TER of 0.22%, almost three times more expensive

- iShares S&P 500: The US ETF (IVV) has a TER of 0.03%, while the European ETF (IUSA) has a TER of 0.07%, twice as expensive

- iShares World: The US ETF (URTH) has a TER of 0.24%, while the European ETF (IWRD) has a TER of 0.50%, twice as expensive

As you can see, the TER of European funds is significantly higher than US ETFs. Over the long term, this will make a significant difference in your returns.

When you are investing in ETFs, investing fees are not to be ignored. And this is especially true if you want to retire early based on your portfolio.

US ETFs are more tax-efficient

The second advantage is even more significant, but it is also a bit more complicated and is only for Swiss investors. Indeed, US ETFs are more tax-efficient for Swiss investors.

This tax efficiency is based on the way dividends are taxed. Especially how the US taxes dividends of US companies.

By default, the US government will tax 30% of the dividends emitted by US companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for US investors. And moreover, we can reclaim the 15% left on our tax declaration.

But when we use an ETF in Europe, the dividends will be withheld before reaching the fund. For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!

This advantage is essential since US stocks make up 50% of the entire world stock market. Saving on the dividends of these stocks is very important.

The second-best domicile for ETFs after the US is Ireland. So, if you do not have access to US ETFs, Ireland (IE) ETFs are the next best thing.

Overall, how much you save will depend on the yield of the ETFs you are using. For a 2% yield, you will save 15% of 2%, which is 0.3%. So, by using US ETFs, you can save up to 0.3% in fees every year! On a 100’000 CHF portfolio, you can save 300 CHF per year!

However, it is critical to know that this deduction can only be claimed when it reaches 100 CHF. Below 100 CHF, taxes will reject this deduction. So you will need about 33’000 CHF in US ETFs before you can claim it.

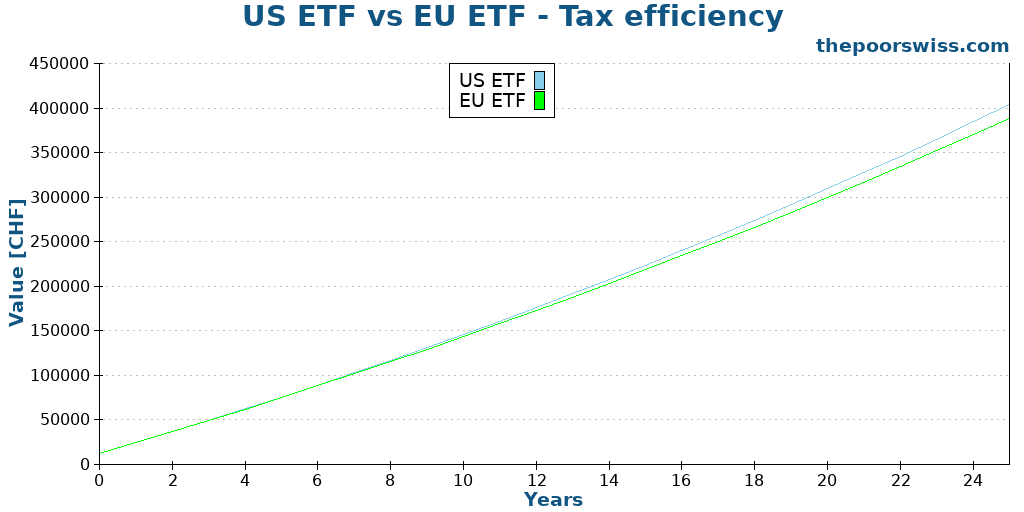

If you are wondering whether this is significant, you can take a look at the following graph. In this example, we are investing 1000 CHF per month over 25 years and the only difference is that we lose 15% of the dividends with

US ETFs are larger

A small advantage is that US ETFs are larger and more liquid. By large, I mean that they are managing more money. Generally, this is exposed as the Assets Under Management (AUM) metric.

A larger ETF has a few advantages over a smaller one:

- It shows more popularity. Larger funds are generally large because they are very popular (people put their money in them).

- It has a lower chance of being closed.

- A larger ETF has a higher trading volume. This has the advantage of the ETF being easier to sell. Generally, they also have a lower spread, which gives you better buying and selling prices.

- A larger ETF can better replicate the index since it will include more small companies than a smaller ETF.

For these reasons, large ETFs are generally better than small ETFs. But this should not be the primary argument in choosing an ETF.

US ETFs are cheaper to trade

The last advantage is that US ETFs are cheaper to trade (with a good broker) than European ETFs.

This is not directly due to the fund itself, but rather to the stock exchange they use.

For instance, my primary ETF, Vanguard Total World (VT), is traded on the New York Stock Exchange (NYSE). To buy or sell shares with Interactive Brokers costs me about 0.35 USD. I can buy many shares and still pay less than a dollar for the transaction.

On the other hand, buying 10’000 CHF of my Swiss ETF, iShares Core SPI ETF (CHSPI) on the Swiss Stock Exchange (SWX), cost me 10 CHF! That is about 30 times more expensive than my US ETFs.

And European ETFs are about in the middle of Swiss ETFs and US ETFs. To my knowledge, US ETFs are the cheapest to trade. Now, this may change if you use a service with free transactions. But there are very few good services like this available in Switzerland yet.

Risks: What about the US Estate Tax?

Many believe we should not invest in US ETFs because of the US Estate Tax. And in some cases, this is true. But in practice, for Swiss investors, there is almost no extra risk in investing in US ETFs.

The US estate tax law states that the inheritance of US ETFs is subject to a 40% inheritance tax. Nonresident aliens (basically, foreigners outside the United States) are exempted from this tax for assets up to 60,000 USD. After this, foreigners will have to pay a 40% tax.

This means that if you have many US assets, they could lose much value when you pass away, and your assets go through inheritance. You do not want this to happen to your estate.

However, many people miss that Switzerland has an estate tax treaty with the United States. And this treaty greatly increases the part exempted from this estate tax!

With this estate tax treaty, Swiss investors are exempted from the US estate tax for up to 11.18 million dollars, prorated to the proportion of US assets in your net worth. For instance, if US ETFs represent 10% of your estate, 1.118 million dollars (10% * 11.18 million) will be exempted from US Estate Tax!

So, in most cases, Swiss investors do not have to worry about the US estate tax! However, it is true that it may complicate your estate. If you have US ETFs, you will need to deal with the IRS.

If you want all the details and many more examples, you can read my in-depth article about the US Estate Tax law. This article also explains how to deal with US estate tax, in the specific case of Interactive Brokers.

What if you cannot use US ETFs?

Unfortunately, many people do not have access to these great US ETFs.

For these people, investing in European ETFs is still an excellent option. Using US ETFs is the best way to invest. However, it is an optimization over European ETFs. There is nothing wrong with investing in European ETFs!

If you want to be optimal, you must go with US ETFs. Now, it could be difficult (or even impossible) to use these ETFs. Even for Swiss investors, few brokers let us access them. If you do not want to go the extra mile and want to invest in good ETFs with lower effort, European ETFs are great!

What matters most is investing, not investing optimally!

What about mutual funds?

In this article, I have talked very specifically about US ETFs, but what about funds?

US mutual funds are also great. But it is interesting to know that Swiss mutual funds can also save you dividends. Indeed, funds are very different from ETFs in how they are held.

With a fund, each investor goes indirectly. With an ETF, you go through a broker who holds the shares in your name.

This allows the fund to be more efficient, directly depending on the treaty. So, a Swiss-domiciled mutual fund is as tax-efficient as a US-domiciled ETF. Of course, the Swiss mutual funds will likely have some other disadvantages (smaller and more expensive, mostly), but it is good to know that the main tax disadvantage of European ETFs is not present in Swiss mutual funds.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

As you can see, there are many strong reasons to invest in US ETFs instead of European ETFs! These ETFs will let you save a significant amount of money in fees and taxes.

80% of my portfolio is invested in Vanguard Total World (VT), a US ETF. The rest is invested in a Swiss ETF for my home bias portion. So, I invest a considerable portion of my money into US ETFs. This is because I consider these ETFs to be the best available for Swiss investors.

However, these ETFs are more difficult to use. Investors from the European Union cannot invest in them anymore, and in Switzerland, only a few brokers let you use them.

As I mentioned, US ETFs are an optimization over European ETFs, but they are not a revolution. If you cannot (or do not want to) invest in US ETFs, investing in European ETFs will be a great way to invest!

If you want to start trading US ETFs, I recommend using Interactive Brokers. It is an excellent broker that lets you trade US ETFs with very low transaction fees. I have a guide on investing with Interactive Brokers.

Are you investing in US ETFs?

More reading

The 4% Rule for Swiss Stocks – Can you retire early?

FIRE with Swiss stocks? We test if the 4% rule works for a portfolio invested entirely in Swiss stocks and bonds versus a global portfolio.

Who is Warren Buffett ? The Man and His Investments

Who is the Oracle of Omaha? Learn about Warren Buffett, his investment philosophy, and how his strategies can help you become a better investor.

What is long-term investing?

Long-term investing allows us to invest more aggressively than shorter terms. But why is that? We study many asset classes over multiple periods.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Reading your blog fills me with nationality envy.

We are kind of lucky indeed :)

hi Mr Poor Swiss. Another great article, thank you. I have a question or two and I see this is not only my concern. Any chance you could write a detailed guideline how to do it (can be Fribourg).

1/ The thing with deividends from US stocks or ETFs. How this exactly works (including how it works in Switzerland – is this deducted? treated as income?).

2/ More important – how to fill in DA-1 form. I am based in Geneva and this scares me, my French is not so fluent. It is probably simple, but the document is very cryptic to me.

3/ Third – if possible, and maybe you know. How to do the same (DA-1) for other countries? For example, there are 2-3 great stocks in countries such as Danemark or Norway, which I want to buy at good price. But each country has different agreement with Switzerland, so I do not know if DA-1 is enough for other countries? I think so, but the data there must be different, different % of base tax in these countries etc.

I guess without points 2 and later 3 explaiend, I will ahve to get personal tax advisor (in case I buy more assets in US or in other countries)

Hi hess,

Since this has been requested many times, I will try to plan to do a guide on how to do it.

1) Dividends are always taxed as income in Switzerland, regardless of where they come from.

2) You have to declare the total dividends for each of your U.S. ETFs in the DA-1 form. You enter the total amount of dividends that you received for each of them. In the colonne about taxes that are not reclaimable, you put 0 and in the other column, you put 15% of the amount.

3) You can use the same form for other countries. I believe it’s enough for each county, but I have never done it for other countries. Yes the percentage will be different in each case. And I can’t research each country to get the percentage.

Thanks for stopping by!

Thank you. I think it would be very useful to have an article, with screenshots how to fill in DA-1 form etc. ANd it doesnt matter if this is Fribourg or not :) I will investigate it deeper when I have to declare my dividends next year, so far my portfolio is small. But next year for sure there will be some dividends and I would love to learn it once for good (it is probably very simple..)

Great post!

I got a question about the currency risk between $ and CHF.

Is it still worth it to invest in US ETFs while CHF increases in value compared to $?

I had this discussion with my parents about investing in US ETFs and I couldn’t give an argument about why they should invest in US ETFs.

Hi Kim,

The point in this article is just about the efficient of U.S. ETFs compared to European ETFs, not about the difference in currency.

Even if you invest in European ETFs, you will be likely to be exposed to the dollar. For instance, one of the most used European ETF VWRL invests in the whole world and holds USD. So investing in VT (U.S.) or VWRL (EU) makes no difference in USD exposure.

You cannot avoid exposure to USD. Even if you buy Swiss stocks, they will do business in USD and you will be indirectly exposed to the dollar.

Now, if you want more details about currency and how to protect against variations, I have an article about currency hedging.

Great article – congrats!

Do you know a good ETF search website for US ETFs?

I am looking for something similar like justetf.com, but for US ETFs. Any suggestions?

All the best

Thanks Beluno :)

I am using the https://etfdb.com/ website to look for U.S. ETFs information.

Thanks for an interesting reading. Do you know whether for the matter of Switzerland-USA tax treaty the “Swiss investors” must be Swiss citizens or being a Swiss tax resident with an EU-country citizenship (ie without the Swiss citizenship) is sufficient?

Dan

Hi Dan,

Good question.

The original tax treaty says “a citizen of or domiciled in Switzerland”. So I believe that being a Swiss resident should be enough. But I am no lawyer, this is just my interpretation of this document.

I started investing with IB and buying VT at the beginning of this year. I was always a little fearful of the tax situation. I’d love to find a guide on how to claim the withholding tax but I’ve only found people talking about it but no real guide. Do you have any plans on writing a guide? Might be difficult since every canton has it’s own program but I’d be very grateful!

Hi rollerstroller,

I could make a guide with the Fribourg tool, but indeed it would be different from any other state.

Now, the basics are the same. In each Swiss tax declaration, you will find a DA-1 form. And you can fill this DA-1 form for each of your U.S. ETFs in order to claim the dividends.

It’s really easy, at least in Fribourg.

I’ll think of writing an article on that to make it more step by step.

Thanks for stopping by!

That would be great! Thanks for sharing all this information, it is really helpful to find the advice from someone that lives in CH!

Hi Mr. The Poor Swiss

I am a 23 years old and i am really happy to have found your blog so early. I started investing regularly in VT monthly a few months back as my long term goal (and take advantage of compound interest as young as possible). Many thanks for all the information and knowledge you are providing.

I maybe would add that the minimum commission of IBKR is CHF 10/monthly, CHF 120/yearly but yet another advantage for young people under 25 the minimum commission is only CHF 3/monthly, CHF 36/yearly.

Of course this only applies if you haven’t invested CHF 100’000 like me ahah but i think you still have to take in consideration when you are a beginner like me 👍

Hi The Young Swiss!

Congratulations on starting to invest so early! I wish I started earlier :)

That’s a good point, I actually forgot they had a price for people younger than 25. But the 10 CHF per month custody fee is mentioned in my review of IB. I see it as a nice goal to get to 100K :)

Thanks for stopping by!

Quite a few advantages there with US ETFs. I did not invest in them cause i was concerned that i will not be able to invest in them after ’22; guess it was even rumored that it will stop at the end of ’20. And also the hassle with tax forms.

What are your plans for the post ’22 time? Where will you invest in? Will you keep the US positions you already habe? Is there info by IB in how they will handle it?

Hi Michael,

If we knew for sure we could not use them after 2022, I would maybe not recommend them anymore. But since I still do not have a clear answer on that, I still recommend investing in them.

The hassle with tax forms is really not that bad, at least in Fribourg, maybe other states are worse.

If we can’t invest in them anymore in 2022, I will keep them and start investing in a portfolio of European ETFs at this stage. Normally, they should simply not let you buy more but you will be allowed to hold your positions and should not be forced to sell.

Thanks for stopping by!

Hi Mr. The Poor Swiss. Great blog, thanks to you I learned about potential issue with investing in S&P500 from 2022 onwards, which is a pity, as we invest monthly for our retirement and for also to secure our little daughter financially when she becomes an adult.

I was wondering if you heard any news about it and whether this will actually apply to IB and Swiss residence from 2022. Thanks in advance

Currently, nothing changed. The latest conjecture is that, we will not lose access to these ETFs in 2022 with IB. But I am not a law expert and the regulations are too complicated for me to be sure. I am just waiting at this time :)

Just a question, for those who may end up back in the UK, are there US ETF tax or estate tax issues vs when resident in Switzerland?

Sorry, I have no idea :)

I have never been to the UK, so I have never read about the taxes in the UK, it’s complex enough to learn about the ones in Switzerland.

Great article Mr PS and very timely for me in fact.

Myself a fan of US ETFs, the point i would be interested to get your view on is whether you waive the currency factor and invest in USD or go for hedged ETFs? I’ve lost significant value on some due to dollar devaluation…

Hi PaulC,

I currently do not hedge against USD variations. I believe that in the long-term, hedging is not necessary.

But I have 20% of my portfolio in CHF. So that is a form of hedge.

I have an article about currency hedging if you want to learn more.