VIAC vs Finpension 3a – Which is the best third pillar for 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

VIAC was unchallenged as Switzerland’s best third pillar until the end of 2020. Then came Finpension 3a, another great third-pillar offer.

I have already reviewed these two excellent services. But we also need to compare VIAC vs. Finpension 3a in detail to see which is the best third pillar in Switzerland.

In this article, I compare VIAC vs Finpension 3a in detail. We see their investing strategies, fees, and everything you need to know to choose!

|

Best Third Pillar!

|

|

|

5.0

|

4.5

|

Finpension 3a

Finpension 3a is the newest challenger in the third pillar world. They started in October 2020. But they are not a new company. Finpension is already behind the best vested benefits account there is in Switzerland.

Finpension 3a started as a mobile-only third pillar but added web support only a few months after its launch.

So what makes Finpension 3a so interesting?

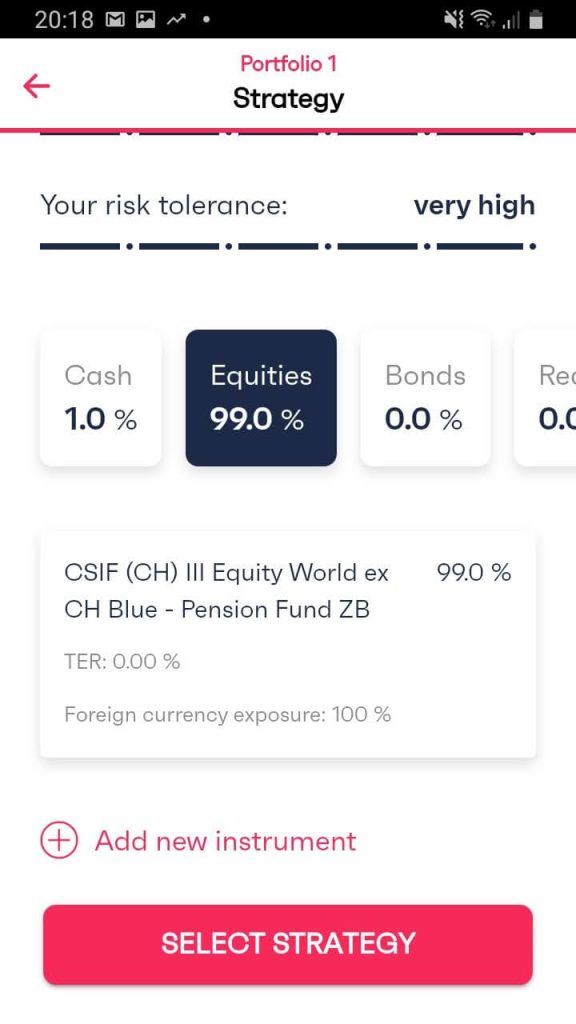

- You can invest up to 99% in stocks!

- The fees are very low, at 0.39% per year.

- You have considerable freedom in your portfolio.

So, while they are new to the third pillar world, they are already exciting. They also have extensive experience managing vested benefits accounts.

For more information, you can read my review of Finpension 3a.

VIAC

VIAC started in 2018 as the first mobile third pillar. When it started, it was the only mobile-only third pillar and started a small revolution in the third pillar world. There are now several mobile alternatives. And now, VIAC also offers a web application.

VIAC has two significant advantages:

- You can invest up to 99% in stocks. They were the first ones to offer such high allocation to stocks.

- The fees are low, at 0.41% per year, for the most interesting strategy. For the Swiss third pillars, this is as low as it gets.

On top of that, VIAC is a very transparent and honest company with clear communication.

All these advantages made it the best third pillar when they started. And they now have more than 15’000 customers.

For more information, you can read my review of VIAC.

Investing Strategies

We start by comparing the investing strategies of VIAC vs Finpension 3a.

Both third pillars invest in mutual funds. They do not use ETFs because pension companies can access much better funds than private investors. Therefore, they can access funds with close to zero (or even zero) TER. So, it is an excellent reason to invest in mutual funds instead of ETFs.

Both companies invest in passive mutual funds. These funds are index funds that minimize costs and try to replicate the market’s performance. Once again, this is a great thing.

Finpension 3a and VIAC let you choose between Credit Suisse and Swisscanto index funds. On top of that, Finpension 3a also provides you with access to UBS, making it a small advantage for Finpension.

Both companies let you invest up to 99% in stocks.

Both companies differ in what they do with the money not invested in stocks. At Finpension, only 1% is kept in cash. The rest is invested in bonds. With VIAC, you can decide between keeping it in bonds or cash. Some people dislike bonds because they yield negative interest for a few years. However, bonds are currently earning more than cash again, so it is a matter of timing. Nevertheless, it is good that VIAC lets you hold cash should you wish to. However, with Finpension, you can invest in a money market fund. A money market fund is similar to cash and would yield the same.

Both companies let you do a 100% cash 3a. For people that do not want to invest right now, this is a great option. Finpension currently offers -0.49% (as of September 2025) on cash accounts.

Overall, both third pillar providers have a great investing strategy! But Finpension 3a is better for investors.

Custom Strategies

Looking at what advanced investors can do with custom strategies is always good. So, we compare VIAC vs Finpension 3a on that point.

Both third pillars let you choose a custom strategy.

With VIAC, there are some limits to what you can do with a custom strategy:

- You can only invest up to 90% in Swiss Stocks.

- VIAC will prevent you from having too much in a single company (this impacts only the SMI)

- They will prevent having more than 20% in Emerging Markets.

These limitations are not that bad. All the other limitations make sense, and I would not want to overcome them. Until August 2024, VIAC was limited the foreign exposure limit to 60%, but this limit is now gone.

With Finpension 3a, you also have some limits:

- Maximum of 20% in precious metals

- Maximum of 50% in Real Estate

And that is about it for the limits. You can have 99% in foreign currencies (1% needs to stay in cash). And you can have 99% in a single World fund, for instance.

And you can even optimize for having 0% TER:

So, Finpension 3a is significantly more flexible regarding custom investing strategies than VIAC. But VIAC still offers great custom strategies. It is still worth mentioning that it took VIAC three years to reach the level of Finpension 3a.

Fees

In the long term, it is essential to consider the investing fees. You will pay these fees for a very long time. And you will pay regardless of the market conditions. So, we need to compare the fees of VIAC vs Finpension 3a.

VIAC charges a base administration fee of 0.52% on the invested assets, with a total administration fee cap of 0.40%. You also pay some fees for the funds themselves.

So, the fees will depend on which strategy you are using. Using the standard Global 100 portfolio (99% in stocks, globally diversified), you will pay 0.41% in fees per year.

You also pay fees for currency conversion, which are 0.75% per conversion. However, this is optimized by netting conversions together. VIAC estimates the annual average to be 0.05%. It is difficult to say if this is accurate. I think it is likely to be slightly higher.

Finally, the index funds used by VIAC also have some subscription and redemption fees. These are almost negligible in the long term since you only buy and sell once, so we can ignore them for now.

This gives a fee of about 0.46% per year for a fully invested and well-diversified portfolio at VIAC.

We can examine Finpension 3a now. The base fee is 0.39% annually and includes VAT and product costs.

Finally, the funds also have some subscription and redemption fees, just like for VIAC. They are mostly using the same funds. The foreign exchange fee is 0.05%. With netting, this will be negligible on average.

This gives us a total fee of about 0.39% for Finpension 3a for an excellent portfolio.

When we compare VIAC vs Finpension 3a, Finpension 3a is cheaper than VIAC. You may think this is not a significant difference, but a 0.39% fee is about 5% cheaper than a 0.41% fee!

There is another advantage to Finpension 3a: its tax domicile. If you are withdrawing your third pillar abroad if you have left Switzerland, the tax domicile of the pension will be important for the taxes. Finpension 3a is domiciled in Schwyz, the canton with the lowest taxes for pension withdrawals! This could make a significant difference for people withdrawing from outside Switzerland.

On top of that, you can save money on fees with both products by recommending the service to friends and families.

If you have 100’000 CHF in your third pillar, you will save 20 CHF per year with Finpension 3a.

Extra Fees

Both of these third pillars have some extra fees that we should also consider.

First, VIAC will charge you 300 CHF if you withdraw your third pillar to buy a house.

Finpension will charge 250 CHF for a withdrawal and 200 CHF for a pledge for real estate, which is slightly cheaper than VIAC.

However, Finpension has some extra fees. If you transfer your 3a out of Finpension less than a year after creating it, you will pay 150 CHF. And if you withdraw abroad, you will pay 250 CHF (750 CHF if that happens during your first year).

So, overall, VIAC has a slight advantage for extra fees since they do not charge any fees for withdrawing abroad. However, Finpension 3a is slightly cheaper for withdrawing for real estate.

Extra features – Insurance

We can also look at the extra features that these two great services offer. It is pretty simple, since only VIAC has an extra feature, and it is the only one.

Indeed, VIAC started offering life or disability insurance in its package. For each 10’000 CHF invested in securities, you will get free protection of 2500 CHF. You have to choose yourself if you want life or disability insurance. You cannot choose both.

We should try to quantify the value of such insurance. In Switzerland, men have a 6% chance of dying before retirement as of 2021. If you have 100’000 CHF invested in your portfolio, you get 25’000 CHF insurance. Based on the probability of dying before retirement, we can put a value of 1500 CHF for your investments’ entire duration.

If you invest for 30 years, you will get a life insurance value of:

- 50 CHF per year if you invest 100’000 CHF in your third pillar

- 100 CHF per year if you invest 200’0000 CHF in your third pillar

- 200 CHF per year if you invest 400’000 CHF in your third pillar

For disability, about 2% of people in Switzerland are concerned with disability insurance as of 2021. So, we will take 2% as the probability of being disabled.

If you invest for 30 years, you will get a life insurance value of:

- 16.66 CHF per year if you invest 100’000 CHF in your third pillar

- 33.33 CHF per year if you invest 200’0000 CHF in your third pillar

- 66.66 CHF per year if you invest 400’000 CHF in your third pillar

These are only rough estimates. But you need a lot of money invested for this insurance to be interesting. And even then, the amounts are relatively low. I prefer paying lower fees and being optimistic. But, for people already customers of VIAC, it is an attractive, although minimal, advantage.

Security

We should compare the security of VIAC vs Finpension 3a.

Both applications are technically secure, and both companies have a strong security record. I have not heard of any leaks or breaches in these two companies.

With Finpension 3a, you can configure the second factor of authentication (SMS or a good authenticator). This helps with security since this will require your phone. This is better than VIAC (only SMS second factor). However, you cannot do much from these two applications since the money is blocked until you can use it.

Both services let you identify yourself with your identity documents. This makes sure that nobody can open an account in your name. At Finpension, you can choose to do that while it is mandatory at VIAC.

From a safety point of view, both third pillars are equivalent. VIAC and Finpension 3a manage the assets, but they are held in a pension foundation’s balance sheets. The assets are saved in a custody bank in both cases. So, in cases of VIAC or Finpension 3a going bankrupt, the foundation must find a new manager.

Overall, I feel like the security of both third pillars is good. But Finpension 3a has the advantage of a true second factor of authentication. So, I would say Finpension 3a is very slightly safer.

Reputation

Finally, we look at the reputation of VIAC vs Finpension 3a.

Both companies are young, and finding many reviews about them is challenging. I have never heard any public bad news about either of them. And both companies seem to have an excellent reputation.

VIAC has 82 reviews on Google and got an average score of 5 out of 5 stars. It is a really impressive score. There are only two reviews with less than five stars, and none point out a real issue. Now, most reviews are advertising codes for their referral programs. So, I would probably not pay attention to most of these reviews.

On the App Store, VIAC got 152 notes and an average score of 4.7 out of 5 stars. On the Play Store, VIAC got 239 reviews for an average 4.8 out of 5 stars.

Finpension 3a has no reviews on Google. They have ten reviews on the Play Store with an average score of 5 out of 5. And they have no reviews on the App Store.

Both companies have the same good reputation. VIAC has slightly more experience with third pillars. But Finpension has more experience with second pillars (1e and vested benefits). So, overall, I have high trust in both of them!

Applications

I do not care about the applications, especially for the third pillar. It is unimportant because you rarely use it and have to do very little with it.

But some people consider this essential. I would much rather invest in a terrible app (with good security!) and low fees than in a beautiful app with higher fees. However it is up to you to decide what you want to prioritize. So, we compare VIAC vs Finpension 3a in terms of their applications.

VIAC offers a mobile and a web application. Both applications are pretty good. They look good and are very easy to use. They did a great job of polishing them.

Finpension 3a is also available as a mobile application and a web application. The mobile application could use some extra polishing, and VIAC is a little better.

On the criteria of applications, VIAC is slightly better than Finpension 3a. Their mobile application feels a little better, but nothing significant.

Summary – VIAC vs Finpension 3a

We can draw a table summary of our findings:

|

Best Third Pillar!

|

Good Third Pillar

|

|

5.0

|

4.5

|

|

|

|

|

|

0.44

|

0.50

|

|

Good

|

Good

|

- Invest 99% in stocks

- Leads the innovation

- Great investing strategy

- Outstanding fees

- Great customization

- Does not let you invest in cash

- Invest 99% in stocks

- Great investing strategy

- Good fees

- Not great for aggressive investors

We can draw a few conclusions from this summary:

- Finpension 3a is better for aggressive investors

- Better expected returns in the long term with Finpension 3a

- Both offer 100% cash 3a

- Finpension 3a is leading the innovation and VIAC is following

- VIAC applications are a little more polished than Finpension 3a

- VIAC offers life or disability insurance coverage

VIAC vs Finpension 3a – Conclusion

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

We are now done comparing VIAC vs Finpension 3a. The first important point to note is that both are great third pillars. They are the two best third pillars available in Switzerland.

But we have to choose a better one! Finpension 3a has advantages over VIAC for long-term investing! Being able to invest 99% in stocks is good. And reducing the fees by about 10% is a great thing.

Considering that custom strategies can lower fees and maximize foreign exposure, I think Finpension is an excellent third pillar!

In 2021, I contributed to Finpension instead of VIAC. Given my long-term horizon and aggressive investing, it fits me best. I think it is the better option for most people who will retire soon. As of 2024, I now have all my 3a accounts at Finpension 3a.

And since you can also do a 100% cash account with Finpension, Finpension is also great for conservative investors.

If you open a Finpension 3a account, please use my code FEYKV5. This code will give you a fee credit of 25 CHF (if you deposit 1000 CHF in the first 12 months) and will help my blog as well.

Which of VIAC vs Finpension 3a do you think is the best? Which third pillar provider are you using?

More reading

Selma 3a Review 2026 – Pros & Cons

Selma already offers an interesting Robo-Advisor and they now offer a Selma 3a account. So, we see if you should invest in this third pillar account.

Liberty Vested Benefits Review 2026 – Pros & Cons

Our honest review of the Liberty vested benefits account. Is this traditional giant worth it, or should you choose a cheaper alternative?

How to Open a VIAC Third Pillar in a Few Easy Steps

Find out how to open a VIAC third pillar in a few easy steps and how to transfer your existing third pillar to your new account.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Dear Baptiste,

IMHO your information about VIAC is slightly outdated. In the meantime VIAC offer funds either from CréditSuisse or Swisscanto. When you opt to Swisscanto, the fees are even slightly slower.

Also the stock quota is now also as high as 99%.

Have a look at https://viac.ch/en/pillar-3a/strategies/?remainder=cash&custody=cs

Regards

André

Thanks, I will update my VIAC articles to reflect that!

Thanks for the article!

Is there any insurance scheme (for ex as we have for banks) if VIAC or Finnpension3a go bankrupt and close their offices? What happens in that case for our investments?

Hi Anon,

I have covered this a little in this article: https://thepoorswiss.com/swiss-deposit-insurance/

The cash is insured as the cash in a bank. On the other hand, the securities are not insured. It is expected (and guaranteed by FINMA) that these securities are held in your name in a separate custody account. So in case of bankruptcy, these should not be at risk.

They are at risk of fraud though.

Hi Baptiste, first of all let me thank you for sharing all your knowledge with us on this site, I really enjoy reading your articles as you always answer the questions which I am looking for! : )

Did you see that the Handelszeitung has just published an article saying that frankly is now 1st, VIAC 2nd and finpension only 7th!?

https://www.handelszeitung.ch/geld/das-sind-die-besten-3a-fonds-2022

I do not have access to this article, but could you imagine what have changed in the meantime that we such different ranking now?

PS: I have two finpension (Global 100 and Individual) and one VIAC (Global 100) portfolio right now and wanted to open an Individual one in VIAC next, but if frankly is the new number one I might open my next portfolio there…?

THX and best regards,

Nemeswiss

Hi Nemeswiss

I don’t have access to this article either.

They have lowered their fees since my review, from 0.47% to 0.45%. However, this is still higher than Finpension 3a at 0.44%. On top of that, Frankly “only” lets you invest up to 95% in stocks, compared to 99% for Finpension 3a.

And on top of that, Frankly uses currency hedging which is, in my opinion, not a good tool in the long term.

Therefore, I still believe Finpension 3a is still ahead of Frankly. In fact, even VIAC is ahead of Frankly for me.

hi Babtiste,

i have a question if in any of 3a i can invest in shorts? (when markets collapse for example)

Hi,

I am not aware of any 3a letting you invest through shorts. 3a is supposed to be long-term investing, not speculation.

Hi Nemeswiss & Baptiste,

you can read the article here:

https://www.heg-fr.ch/media/4z3agrqv/3a-fonds_mai2022.pdf

( PDF-source: https://www.heg-fr.ch/de/medien-und-offentlichkeit/news/das-sind-die-besten-3a-fonds-2022/ )

and sometimes the online-article is/was accessible with this link:

http://www.handelszeitung.ch/fondsvergleich

but why it sometimes works/worked to read the full article & sometimes not is a mistery to me … just as why frankly got elected to be the #1 (????)

(sorry for my (perhaps) poor English ;-) it’s not my native language)

Thanks a lot for sharing!

Reading that, it seems non-sensical to me. They are trying to compare things that should not be compared and make a global ranking. They don’t even have Frankly in their final comparison table for the highest amount of actions. And frankly is never first in their comparison table as well, so how come it makes first place?

This article simply does not make any sense to me.

Hello!

I have a question for finpension :

Since it is not a robo-advisor, ans admitting I am a noob in matter of investment and finance..

Does the app autonomously handles the portfolio strategy or do I need necessarily to custom it heavily?

And second question :does it make sense to open 3d pillar on finpension (or viac) and having for instance a true wealth account?

Thank you, I hope I was clear enough

Hi J,

It acts like a robo-advisor, but for the third pillar. There is nothing to be done manually. Your investments will be balanced by Finpension, all automatically.

And yes, it does make sense to have both a 3rd pillar and TW. First, I recommend maxing out the third pillar since there are tax benefits. And then, if you can save even more money (great!), you can start saving it in True Wealth if you want (or other Robo-advisors, or DIY).

VIAC has Nasdaq 100 and iShares Global Clean Energy Equity funds.

Also in VIAC I can change my strategy weekly if need so.

The above 2 are reasons I keep my funds in VIAC.

Regarding your second point, Finpension also rebalances weekly now :)

However, I don’t think that’s a good advantage, most people should never change their strategy.

But VIAC remains a great service!

Thanks for sharing!

Used your Code for finpension today :)

Thank you :)

Hi,

Great article thanks. I’m starting my new job in CH next month and I was looking for a 3rd pillar. Over the course of 30 years it is better to be more aggressive and Finpension with 99% stocks and 10% less fees is better. Is it still the case if you contribute for only 15 years ? How agressive should my strategy be ? Still 99% stock or less ? If less, is it better going for VIAC ?

Thanks a lot

Hi,

VIAC is only going to be cheaper if you opt for bonds.

As for how aggressive you should be, it depends on your situation. If you have a long-term horizon, you can be more aggressive. But you need to be able to withstand the virtual loss without changing your strategy. Can you not touch your account and continue investing, if your portfolio is down 50%? If you can and have 30 years horizon, then, go for 99%.

Hey, thanks for this nice article. I wanted to ask you – how exactly you select your investment in these 3rd pillar providers? I mean – do you have to select their pre-prepared plans or you can choose many mutual funds personally? For example, on VIAC page I see they have some strategies, like Global 100 etc. But down below on the page, there is Asset list and there are multiple funds or whatever it is, for example: CSIF Europe or iShares Global Clean Energy + their TER< ISIN etc. Can you choose these directly or must use strageries only? Many thanks.

Hi small_potato,

For both, you can do either:

* use an existing portfolio

* create a custom portfolio

And with Finpension 3a, you have almost no limits to the customization you can make.

hi there , thank you! But then, the cost is what? This is always maximum 0.44% (or around) or that can grow much higher if you customize your own portfolio?

This can grow slightly higher, but not much. And this is very transparent in the app or website if you do your own portfolio.

Hi! Thanks very much for the answer. Yes, it was quite clear for me that it’s not the cheapest way to do 3a pillars but well as i wasn’t adviced other way at that time i did it. Now they are more then 5 years old but i think it is not bound to my mortgage – as I don’t have my mortgage from the same place. They were talking about using later the 3a pillar money for amortization of the mortgage but as i understood it is only available after arround 8 or 10 years and of course only a smaller amount of money (like 10k?) Which doesn’t make a huge difference when we talk about high amounts of money as mortgages in Switzerland are high because of the very high prices of the real estates. I think i will leave it like it is as it got too complicated and i really don’t have time to deal with this now. On the other hand we want to keep the life insurance anyway. But thanks again! All the best and keep up the great work with this blog!

If you want to keep life insurance, it’s fine indeed. But keep in mind that the longer you wait, the more expensive it’s going to be to cancel it.

And if you want to cancel it, just check with your bank, even if it’s not the same place, you may have pledged it and then it kind of belongs to the bank.

Dear Mr. Poor Swiss!

First of all I’d like to thank you very much for your great blog! I have had till now around 4 or 5 agents and i was never so clearly adviced as from your blog! I first read about Credit Cards then about the neo-digital banks (to which i changed from PF) and now about 3a pillar. Currently i have three different 3rd pillars, for the tax-progression made them in three different years, and i pay for the three together the yearly max. tax deductible 6850? Fr. One of them is a 3a at SwissLife (Flex Save Duo with life insurance), the second one is a Generali (GA: gemischte Versicherung Fondsgebunden with life insurance) and a Mobiliar 3a pillar (where i pay yearly 2351 fr., And some 145 fr yearly as an insurance if i lose my job; they are the only from the three who clearly write that they have a yearly fee of 70 Fr for this)

Now, i did the life insurance and the job insurance mainly because of my family (4 kids and wife has no income) and because of the fact that usually most banks took me more seriously when i was trying to get a mortgage. If you have read till here – THANKS! My question is: do you know how much the generali and the swisslife “charge” for the 3a pillar in %? And would you advise me to change to viac or to Finpension from my 3rd pillars?! And is it possible at all?! Is there a fee or do i loose some money? Or is it not possible as it’s a “gebundene” (tied) 3a pillar? Or is it not possible because of the integrated life and job insurances? Sorry, it got a bit long… If you could give me an advice on this, i would appreciate it a lot! Thanks! And congrats again for the great blog! M.

Hi,

I do not know how much they charge because this depends on how your funds are invested. With most 3a life insurance, you can choose to invest your assets (or not). And the fees depending on your investing profile. But it’s usually between 1% and 2% per year on the assets. This is on top of the premium you pay for the life insurance itself.

3a life insurance policies can be canceled, but this is not cheap. The problem is that the first yeras, most of what you pay goes into insurance. So if you cancel in the first 1-2 years, you generally get nothing. And even later, a lot of the money is lost.

Now, if you just did one of them, you could cancel it and you would not lose much money. But then, you have to consider whether you want life insurance, in which case, you could either keep it or get a non-3a life insurance.

Finally, if you have pledged your life insurance for indirect amortization, I have no idea how to cancel, it’s probably possible, but you may have to renegotiate your mortgage.