January 2026 – No more life insurance 3a!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

January 2026 was very taxing for me. Overall, it was a good month with only a few events. But there was a lot going on during the week, for the blog and at work, and this is exhausting. I am looking forward to some things getting more stable.

The highlight of this month is that we are finally rid of our life insurance 3a! We sent out the letter in December and received the amount in January.

Financially, it was not a good month. We had to pay for the notary bill for the purchase of the house. This large bill plus a few significant bills meant we did not save any money this month.

January 2026

January 2026 was quite busy. My wife is doing her German course, so I am doing more driving for my son. This means less time for other projects. And I did a time-consuming collaboration with Qoqa during this month. Finally, we also started looking for solar panels, which means meetings and calls.

This is really my limit. I could not have taken anything else during the month, and it was not enjoyable. Next month will be busy but less so.

One great thing this month is that we are finally rid of our life insurance 3a! The policy was tied to our first house mortgage, and after we sold it, we could cancel it! After sending the letter, it took about a month to get our money back into Finpension 3a. I am happy that this mistake is behind us.

Financially, it was an expensive month. We spent more than usual but had a standard income.

We had a few more expenses related to the house purchase. Furthermore, we got a power inspection (mandatory when you buy a house if it was not done in the last 5 years). This cost us 345 CHF. There are a few things that need to be fixed and will probably again cost the same amount, but nothing drastic.

We also had to pay the notary for the contract. This cost us 5269 CHF. The only large expense that we have left for the house purchase is the land register, which will be much higher. We expect it in the next few months.

Because of these bills, we did not save any money this month. Since these bills are expected with the purchase of the house, we were totally prepared to save less money.

CSV transactions from Cembra / Certo

A great Swiss credit card with excellent cashback (up to 1%!), very flexible, and with a good mobile application.

- No yearly fee

- 1% cashback in three shops

It may be late, but I have great news. We can now export transactions from Cembra credit cards (like the Certo One) to a CSV file. This is really useful for people tracking expenses. Before, it was very inconvenient. I used to convert the PDF to CSV to later import. But then, the PDF was only available once a month. Now, you can export at any time you want.

This will save me time every month and will avoid errors doing manual expense tracking.

I have no idea when they added that feature. I have found it by chance. You can log in to Cembra eService. From there, you can see the list of transactions, and at the bottom, there is a button to export the transaction to CSV. And the great thing is that you can do that for either all transactions or based on a filter (like the last week).

Obviously, they could have added this a long time ago, but I am still thrilled they implemented it.

Beware of an ongoing scam

For a few months, many non-residents have been receiving emails impersonating Alpian. These scammers are promising more than 6% guaranteed returns per year to lure people in. This is obviously wrong, and Alpian itself is not even open to non-residents.

I have discussed this with Alpian and they are fighting this, but it will take time. So, meanwhile, be extra careful.

And it does not hurt to repeat a few things to check out in emails:

- Check that the domain of the sender makes sense.

- Check that the links in the email are pointing to the proper domain.

- Remember that if it is too good to be true, it is because it is not true.

- When in doubt, contact the company directly (do not reply to the email; write a new one and look up the address yourself)

If you want more tips about security, you should read our guide about online security.

Expenses

Here are the details of our expenses in January 2026:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 849 | Expected | Health insurance for three |

| Transportation | 14 | Lower than expected | Only a few buses and one parking |

| Personal | 2167 | Higher than expected | Mostly stand expenses, but with a large wood expense |

| Food | 1233 | Higher than expected | One extra trip to Aligro, more snacks out of the house than usual |

| Housing | 6890 | Expected | Notary, mortgage, OIBT, and SERAFE |

| Taxes | 5541 | Expected | Taxes at two levels only |

In total, we spent 16,697 CHF. Without taxes, this amounts to 11,155 CHF. And without notary and taxes, this amounts to 5,886 CHF.

As mentioned before, a large bill was the notary, which was expected. The OIBT inspection is also expected. We also received the SERAFE bill for the usual 335 CHF amount. We will soon have to vote for a reduction to 200 CHF. I am personally in favor of this because I do not consume any Swiss media, but this is not going to make a difference to our budget.

Another large expense on the last day of the month was buying a bunch of wood to build a strong shelf in our garage. I designed it myself. I first wanted to buy the wood in person, but they did not have anybody to help me in the store, and they were missing several pieces of lumber I needed. So I did it online. The delivery fee is a bit high (75 CHF), but I am not sure whether it would have fit into my car, so it is fine.

But the price of wood is quite insane in Switzerland. I paid about 420 CHF just for the lumber. I probably went a bit overboard on the solidity of the posts and rails, but still, this is a bit shocking to me. A large lumber project rapidly gets expensive. I am still looking forward to assembling that beast and finally getting a clean garage.

Overall, I am fine with our spending this month. Considering the exceptional bills, this is a fine result.

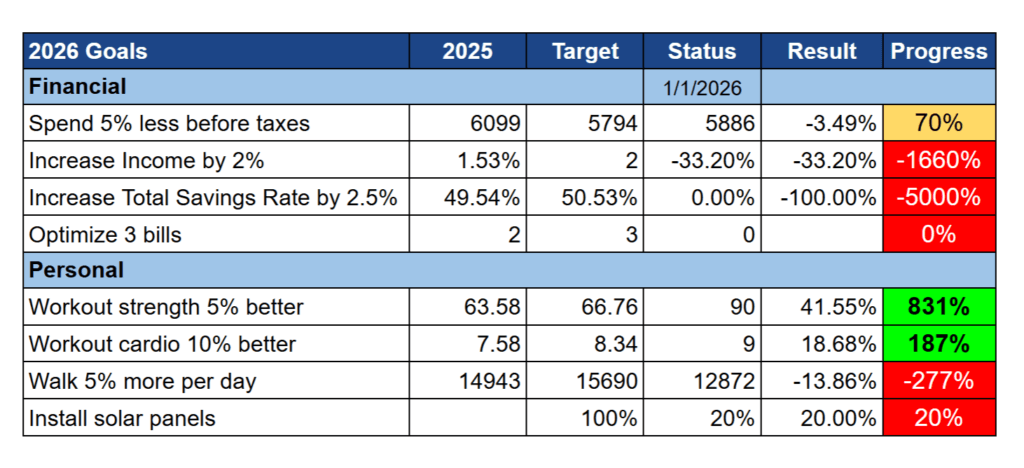

2026 Goals

Here is the status of our goals by the end of January 2026:

With only one month in, the goals are a bit hectic. Obviously, since we did not save any money this month, our savings rate goal is not great. Our income goal is based on average, so it will only pick up in March with my bonus.

We have made some progress towards solar panels this month. This also took quite a lot of my time. Currently, we have contacted people from five different companies. One of them ghosted us after saying twice that they would contact us soon. And we could get the other four to our house. As I am writing this article, we have received three offers. Once we have the last one, we plan to decide early next month.

I started the year very well with workouts. Even when I am going to the office, I manage to go regularly to the gym. On the other hand, my daily steps are lower than I would like. When I go to the office, I almost do not walk. But I do not see what I could do about it.

Overall, given it is the first month of the year, I am fine with our progress. It will take a few months to see whether we go in the right direction.

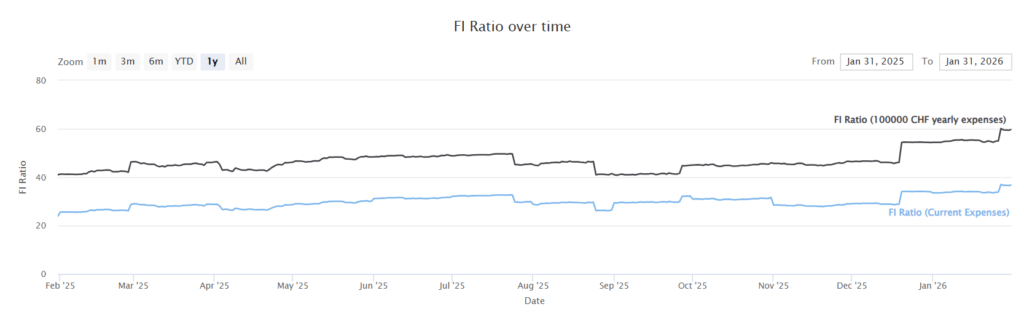

FI Ratio

Here is the progress of our FI ratio as of January 2026:

We made nice progress this month, but also not much. Let me explain.

In January, we usually receive a large payment on the blog. This is because one of our partners pays up once a year only. So, this increases our net worth (since we account for company assets).

On the other hand, we lost money on our investments. Our ETFs went up a bit in USD, but we lost money in CHF. So, overall, our investments are not doing very well. Our second pillar paid up a very nice interest rate this year, with 5% on the mandatory part and 6% on the extra-mandatory part. This makes a nice increase to our second pillar assets.

Overall, this is all part of the process, so I am happy about it.

The blog – Improvements to FI plannner

Overall, I have not had much time for the blog this month.

I did a collaboration with Qoqa where I would answer questions on their blog. I think it was a nice experience, but it took a lot of time. The timing was not great since there was plenty going on this month.

I updated some old articles for consistency with the blog. This is something I should do more, but I do not have that much time to do it, unfortunately.

Last month, I introduced the FI planner. After some feedback, I have a few improvements. And I am now working on a next version that will be much more complete with features such as:

- Handle two persons

- Handle second and third pillars

- Handle growing incomes

Please let me know in the comments below if you have other suggestions.

Next month, I will not have more time for the blog, I feel. My goal is to keep up with the usual daily tasks and write my four articles.

Next Month – February 2026

Next month will also be busy. My wife is still doing her course, so that means a lot of driving my son and less time for other activities. Hopefully, we will be able to order our solar panel project already.

Financially, I expect February 2026 to be good. We have few taxes to pay in February, and income should be normal. The only exception is if we receive the bill from the land register.

What about you? How was January 2026?

More reading

November 2019 – Flights to China

In November, we could save a lot of of our income and spent some days in Berlin and Zurich.

October 2017 Update

In October 2017, we saved very little money, mostly due to some unexpected large bills.

September 2025 – We moved in

In September 2025, we moved into our new house! We are thrilled about that. We also spent too much money, but we will get back to saving later.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste, thanks for your update. You mentioned you lost money on the investments, is that because the increase in value of your USD-ETFs was lower than the increase of the CHF compared to the USD?

If so, would you advise against investing in ETFs based on USD or do you think the return will be bigger some day in the future than the loss of the US-currency compared to the CHF?

Many thanks, Stephan

Hi Stephan

Yes, it mostly because of a loss in USD.

I think in the long run, it does not matter much. In the short-term, hedging can win, but it will not protect us enough in the long term to be worth its cost.

But, if you need hedging to feel relaxed about your portfolio, it’s a great tool!

Hi Baptiste,

Great returns on the 2nd pillar there! Is that your employer’s 2nd pillar or are you on a self-employed contract and have it with VIAC/Finpension?

I wonder how you managed to get such a good result on that, considering it is usually capped around 1.5%/year.

Looking forward to your comments!

Hi Xanoso

This is my employer’s. It performed quite well these last few years. My employer is using AXA.

Do you know exactly which fund/product it is? I am also with AXA, and for me it was 1.5% and 2.25% in 2025.

This is something that bothers me the most. As an employee, you have little influence on the second pillar. And it’s also incredibly difficult to compare them.

Even though we’re both with AXA, we have different products. But which ones they are and how they differ -> good luck with that… At least i don’t see a product description or similar on my available documents

Hi mcd

We are in the AXA Romandie Foundation for the French-speaking part. They are quite transparent: https://www.axa.ch/fr/aproposdaxa/entreprise/fondations/fondation-lpp-suisse-romande/chiffres-cles-actualites.html

But AXA seems to have multiple entities, and if you have a large company, you may have your own foundation, managed by AXA.

Hi Baptiste,

Happy to hear that you are out of 3a life insurance. Was it difficult to finally get rid ? Would appreciate some details, tips and tricks as usually. I also have it in mind (currently with Swisslife).

Thanks,

We just did the same, from Swiss Life -> Finpension.

We didn’t ask the existing providers – no change to cause trouble. We just setup Finpension, downloaded the transfer forms, and send them to Swiss Life.

They actioned it, money arrived 2-3 weeks later.

They’re legally obliged to allow it, so all good. HAPPY to be rid of that cr*p!

No, it was trivial. We sent a letter (registered), saying we want to cancel that policy and where to send the money. After about 2 weeks, they tried to convince us to stay and one week later sent us the money and a confirmation.

As Matt said, since it’s the 3a, there is nothing they can do but try to convince you.

Sounds simple :-)

I was more wondering if moving money will imply some penalty; did they return every penny you invested + interests accumulated over years ?

Thanks,

They returned the current value. It’s far from everything I invested. You will never get back (even at term) everything you have invested with a life insurance 3a because a significant portion will go towards the risk insurance and that part is not invested. I have lost about 12,000 CHF over 9 years with this policy.

Hello Baptiste and happy new year! Januar is always tough! LOL

I wish you a very good start though!

Anyway, I haven’t checked Finpension 3a yet but I’ll definitely have a go… However, I’m planning to transfer my 3a from Swiss Life to Yuh — don’t you think YUH could offer you almost half a million CHF after retirement with a pre-30k investment and 50k of payroll per year? Hadn’t you calculated it with the Yuh calculator if it was worth it to you? E.g. NEON isn’t a good one…

Many thanks in advance!

Hi,

I am not sure I follow since you mention 50k of payroll. You can only invest 7’258 per year in your 3a. If you want to reach one million after 30 years, you would need to get 7.5% annual interest, which is quite optimistic in CHF.

In my tests, Yuh 3a is worse than Neon 3a.

You can check out our third pillar comparison tool

I’m sorry wood is so expensive there!

We have a shed full of nice wood out back that we’ve been trying to give away.

Wish we could give it to YOU!!

Hi Baptiste,

You mentioned SERAFE bill bill and possibility for reduction? How does this happen? I also do not consume Swiss media and challenged this when I first arrived, but they said if you have a car with a radio (which I do) then you have to pay. :(.

Can you please elaborate?

Thanks for all you do, I really enjoy your blog!

Hi Jason

Currently, there is no possibility. But we will have to vote soon (in March) on a reduction to 200 CHF. So, if Swiss people vote yes, this bill will be reduced to 200 CHF per year.

Yes, currently, there is no way to opt out. Even if you don’t have a car and only have internet, you have to pay.