February 2026 – Another busy month

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

February was a busy month again, but a bit less than last month. I did not see so much out of balance as last month. And next month should be better.

Financially, it was a mixed month. It was supposed to be an outstanding month for savings rate with low expenses and high income, but it ended up being an average month because of a very unexpected expense. In the end, we saved 45% of our income.

February 2026

February 2026 was quite busy, but at least it was less so than the previous month. This will be the last full month when my wife has her German courses. Next month is the final test. After that, we will go back to our more usual routine until she starts school again in September.

We have had some work left to do with solar panels as well this month, but most of the heavy lifting is done. So, next month, we will have a bit more breathing room.

I built a new shelf in the garage. This makes the garage much more tidy and saves us a lot of space. Next month, I will probably order the wood to build the second one (we have a double garage). This project was a lot of fun, as are all the DIY wood projects. I made a few mistakes, but I learned a lot and used new tools.

I will not go into any detail, but we had to help a family member in need this month. This already cost us 12,000 CHF and may cost us more. So we will cut down some of the projects other than solar this year.

Fortunately, I received a significant amount of shares for about 13,000 CHF this month. And we did not pay any taxes this month. This month was supposed to have a huge savings rate, but at least it indeed has a good savings rate.

Now that we got rid of our horrible life insurance 3a, we took out pure risk life insurance, as we planned. Since I am currently the main earner of the family and since we are not yet financially independent, I still want to protect my family. We took out a SquareLife policy through SafeSide. I wanted a 10-year policy, but my wife preferred a longer one, and we ended up with 20 years, which is not too expensive at 25 CHF per month for 250,000 CHF coverage. So, our coverage is much higher than before, we pay lower fees, and our retirement assets are growing with Finpension instead of rotting away.

In theory, this month should have been great for our savings rate, but the 12K expense weighed us down. We still saved 45% of our income, thanks for the extra income.

Expenses

Here are the details of our expenses in February 2026:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 875 | Expected | Health insurance and life insurance |

| Transportation | 124 | Expected | Few buses and renewal of bus plan |

| Personal | 13564 | Much higher than expected | The big family help and reasonable expenses |

| Food | 719 | Expected | Groceries and higher than usual meals out |

| Housing | 1021 | Expected | Mortgage for the house |

| Taxes | 0 | Expected | No taxes this month |

In total, we spent 16305 CHF, which is much more than we want to spend in a month. If we remove the 12K, we only spent 4305 CHF, which is actually great.

Overall, our expenses are good this month. We renewed a domain we use for our family for almost 200 CHF. And I bought a miter saw for the garage projects and future projects as well.

Our food budget is slightly inflated because my wife had lunches multiple times with her German-course classmates. But our budget is still well within reason.

Overall, once we look past the elephant in the room, our expenses are quite decent.

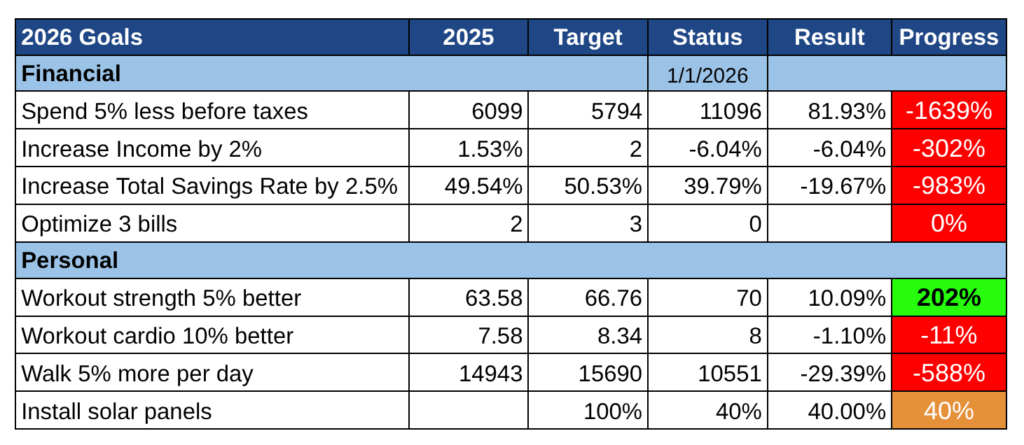

2026 Goals

Here is the status of our goals by the end of February 2026:

Overall, our goals do not look too good.

I now realize that my savings rate goal was a bit dumb. Even without the money we lost this month, it is not reasonable to expect we would save much money this year with solar panels and land register bills. For that reason, I will not count expenses for the notary, the land register, and solar panels in the savings rate for the goal (I will still count them in our monthly updates). We will still fall short of our goal, but it feels like the goal is more reasonable that way.

We made good progress towards our solar panels this month. Indeed, we have selected an offer out of four we received. It was not easy to choose because not all offers were truly comparable, but eventually, we had a good feeling about this choice. We have informed the municipality about the installation, and they confirmed that we can go ahead. Now we are awaiting information about the start of the work. I am expecting to pay the advance payment early next month.

As for my health goals, they did not go as well as planned. I had to switch over multiple office days and ended up not having the time to complete them. I am still doing well, but my goals are meant for my regular routine, not a new, busier variation.

Overall, I am not pleased with our progress this month. But given the current situation, I do not see either how I could have done better.

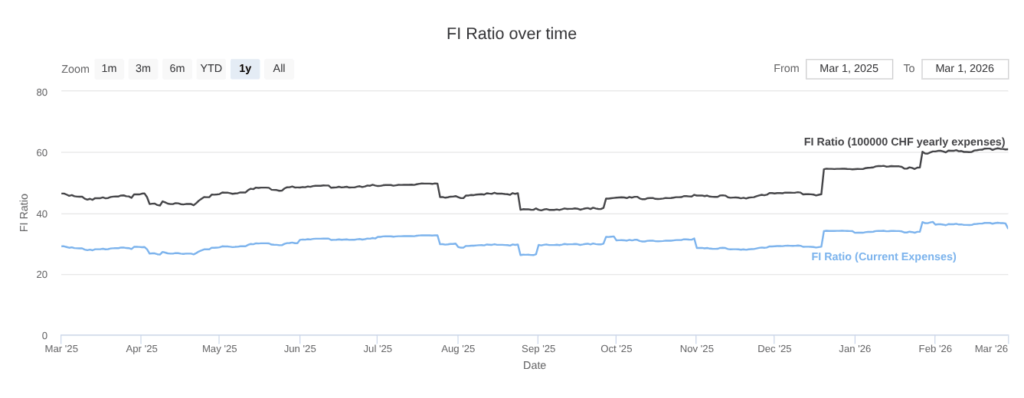

FI Ratio

Here is the progress of our FI ratio as of February 2026:

At least, our FI ratio is doing well. We are hovering over 60% of our financial independence target.

Our progress this month is mostly due to our savings. Some of our investments increased, but not significantly so.

Given the high expenses that are coming, our FI net worth will go down. Therefore, I will be happy at the end of the year if we are still at the same place.

Overall, I am happy about our progress towards financial independence.

The blog – Updated FI planner

Overall, there is only one thing that changed on the blog this month. I have finalized the changes I wanted to make to the FI planner. The tool is now much more complete, with features such as:

- Support for the third pillar

- Support for the second pillar

- Support for two persons with different ages

- And more

The simulations are now much closer to reality. I hope this is helpful to help people plan their financial independence journey. I am open to suggestions to improve it further.

Other than that, I have not had the opportunity to do any other significant changes on the blog this month.

I have started working on the translation of the e-book to German. This has been requested multiple times already. Since this is the last of my resources that is not translated, it makes sense to get it done. I will need to get someone to fully proofread it because I cannot do it myself. So, I will hopefully have the German ebook next month.

Next Month – March 2026

In March 2026, we hope to have more time to ourselves. It should be less busy. We hope to get a start date for the solar panel installation as well.

Financially, we will have a large income since I get my bonus in March. However, if the land register bill arrives already or if we have to pay the advance payment for the solar panels, our savings will not be great. But these two expenses are expected, so it is fine.

What about you? How was February 2026?

More reading

May 2025 – A nice month

May 2025 was a nice and balanced month, with good weather! Financially, it was also good with extra income and low expenses.

April 2020 – A month at home

In April 2020, we saved more than 75% of our income. Because of the isolation, we spend very little money this month at home.

November 2019 – Flights to China

In November, we could save a lot of of our income and spent some days in Berlin and Zurich.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

This is yet another test comment

Did you buy life insurance just in case of death or also capital in case of disability?

We were looking for coverage in death only.

what was your reasoning there? I always feel like death is already better insured than the loss of your income if disability strikes. If you die, your wife will get a widow’s pension, she’ll get access to your 3a… all while costs are reduced by what it costs to supply one person. But if you become IV, you get first pillar pension, if you want the same from your second pillar you give up the right to withdraw your planned lump sum at retirement, and you might have increased costs, depending on what is the cause of your disability.

How did you choose the amount? Is that what your wife would need to pay off the mortgage or is it to offset the half your child would inherit so she can pay them out and keep full ownership of the property? That’s what a friend of mine did, calculated with expected value increase of the property, what the child’s part of the estate would be and they bought life insurance over that amount so the spouse would be able to give the child the inheritance in cash and keep full ownership over the apartment.

Hi

The main reason for me is that disability would not necessarily mean loss of income. It would take a very major disability for me to not be able to do my job or my blog. I am not saying I could do 100%, of course, and in extreme cases, I would have no income indeed.

We choose the amount to be about 3 years of expenses. This would help her kickstart again and then likely pay off some of the mortgage.

Doesn’t your wife have a pretty good coverage with your Pillar 2 already? Spouse pension in case of death is generally 60-80% of your annual income, so wondering why an additional life insurance is necessary.

We do have decent coverage in my second pillar indeed. But this help as a lump sum next to that.

In our case, we are well covered with the second pillar, but be careful that second pillars can offer very different widow pension:

* Sometimes, it’s based on accrued assets, sometimes on insured salary

* Sometimes, it’s based on the mandatory part only (the 90k insured salary)

Hey Baptiste, who did you choose for solar panels in the end? We will soon b3 moving into a house and this is one of my priorities before 2028. Appreciate any info and recommendations, or does it vary so much canton to canton ?

Hi will

We are going with Groupe E Connect. They had the most well-rounded offer. They were not the cheapest nor the most expensive, and we had a good feeling about their offer and their answers to our questions.

It will vary a lot because some providers are only in some cantons.

I would recommend getting at least 3 offers for such a project.