May 2025 – A nice month

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

After a relatively painful month of April, May 2025 was a much better month. We got some nice weather and a good balance of things and events. We could see our friends and family a few times and also had some time for ourselves.

Financially, it was also a very nice month. We only had standard expenses but higher than average income. As a result, we saved more than two thirds of our income.

May 2025

May 2025 was a nice month. We had both very nice and very bad weather. But we were lucky in having good weather during the weekend and could have nice time outside.

It was great that this month was much more balanced than the previous month. We did not have any great events on the blog that took time to handle. It was quite business as usual. And with that, we could focus on everything properly and plan articles in advance. So, we are back to normal where the blog can be handled on the side and does not intervene with other priorities.

As for our expenses, we went back to our average spending. And we had extra income through shares that vested from my company. As a result, we could save 67% of our income this month. A very nice result for a month of May.

Neon new fees

Since, I have received many questions and comments about Neon new fees, I want to spend a little time for sharing my thoughts.

Starting May 12th 2025, Neon introduced a new pricing structure with four account tiers. The main difference is that the free tier is not that free anymore. Indeed, two things became pricier:

- No more free withdrawals

- An extra 0.35% fee on payments abroad and in foreign currencies

Before, we got the cheapest account possible in most cases. But there are now some cheaper alternatives like Alpian, WIR Bank Top and the Valiant Lilac set which I plan to review soon.

There are some higher account tier, but I am not sure if they make a lot of sense because they are pricier than alternatives.

The extra 0.35% surcharge should not be a big deal for most people. We do not buy that much in foreign currencies these days, maybe a few hundreds per month on average. But we still have to withdraw money from time to time, probably every other month.

I have not yet reached a decision, but I want to optimize our banking accounts again. Since the base account is not that free anymore, I do not feel like paying for the duo accounts makes a lot of sense. So, I am currently looking at either a new joint account with a card with interbank exchange rate or simply moving back to Migros Bank and then using a secondary account for payments. Since we still have our Migros Bank account, I think the simplest solution is to go back to Migros. And then, I will choose a secondary account for payments abroad.

For a while, I had wanted to give Revolut a second chance. And I was thinking that with the conversion to the new IBAN system, they would be interesting. My account got converted this month to the new individual Swiss IBAN. Unfortunately, this was mostly marketing. The IBANs are indeed unique, but they are still in the name of Revolut UBS. So, you still need to put the real beneficiary in the message. So, nothing has changed and I do not plan to use them.

I will keep you informed in the next update. Please let me know in the comments below what you think of doing.

E-tax statements for IBKR

Another thing I want to mention first is the possibility to get e-tax statements for Interactive Brokers account in the future.

I have been collaborating with Datalevel AG to generate e-tax statements for Interactive Brokers account. They are currently looking for more testers. The goal is to get the system ready to deliver e-tax statements (for a fee, not yet known) in 2026.

If you are interested, take a look at the post on our forums.

Expenses

Here are the details of our expenses in May 2025:

| Category | Total | Details |

|---|---|---|

| Insurances | 831 | Health insurance for three |

| Transportation | 89 | Buses and parking |

| Personal | 2179 | Daycare, holidays, courses, books, gifts, … |

| Food | 1363 | Groceries, some snacks and a special lunch |

| Housing | 920 | Mortgage, heating and a new mailbox |

| Taxes | 2793 | Cantonal taxes only |

In total, we spent 8177 CHF in May 2025. Without taxes, this comes up to 5383 CHF. As usual, we are slightly above our target, but not that much. Considering we had to pay for a new mailbox for the house our expenses this month are quite decent.

Overall, there are not many interesting expenses this month. We changed the mailboxes in all the buildings around us and this cost about 460 CHF. Since the mailboxes were 30 years old, this is a normal change. Other than that, our expenses are the usual bunch, kindergarten, insurance, heating, mortgage and many small expenses.

Our food budget is higher than usual. We had a large BBQ with many friends and this made a large difference, but this was well worth it.

We have started to pay taxes again this month. So far, we only paid cantonal taxes in May. Next month, we will pay the municipality taxes as well, and I expect the federal taxes to come up as well.

Overall, I am happy about the state of our expenses this month. We have reached some kind of equilibrium.

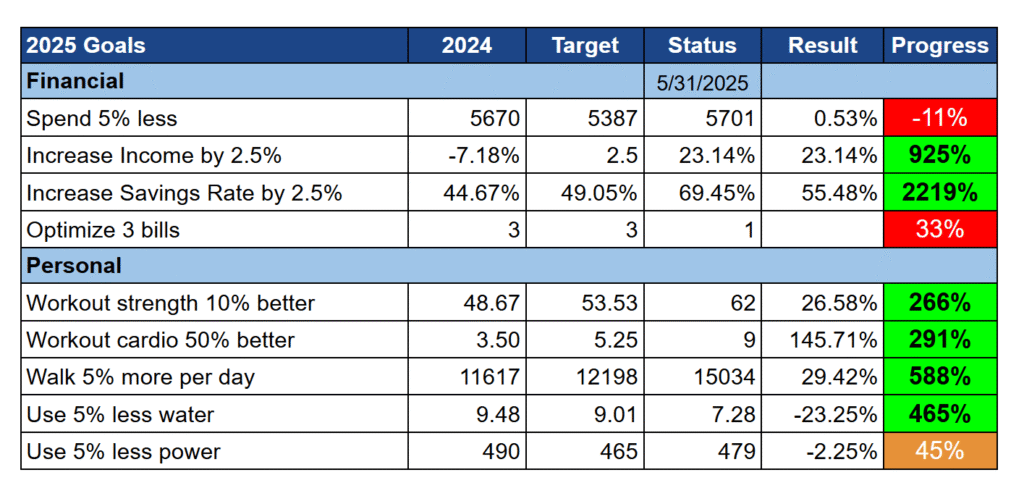

2025 Goals

Here is the status of our goals by the end of May 2025:

Overall, our goals are doing well. As usual, the worst of our goals if the expense goal. But we have made tiny progress on that one. If we manage to do one more good month like this month, we will be back below the average of 2024. Both of our income and savings rates goals are doing well, but they will go down over time since the best months area already gone.

I finally got around to optimizing one bill this month. We have canceled all our complementary health insurance from Assura and renewed only a few of them at Concordia. This may not be the cheapest for complementary, but I did not want to have them separated from the base anymore (I chose simple over cheap). But overall, this will save us 60 CHF per month starting next year.

I had to go to the office more than usual this month. As a result, I missed multiple days of my workouts and cardio trainings. This is expected to happen occasionally and should stabilize again in the following months. Nevertheless, my health goals are doing fine. And this month, I walked the most I ever did in a month.

Consumption-wise, our water consumption went up this month. This makes sense because of the heat, we played outside more and used more water for the garden and the plants. Our power consumption also went up but only slightly. Since I had to bring back servers for monitoring, we are very unlikely to reach a better level.

Overall, I am happy about the progress we made on our goals this month.

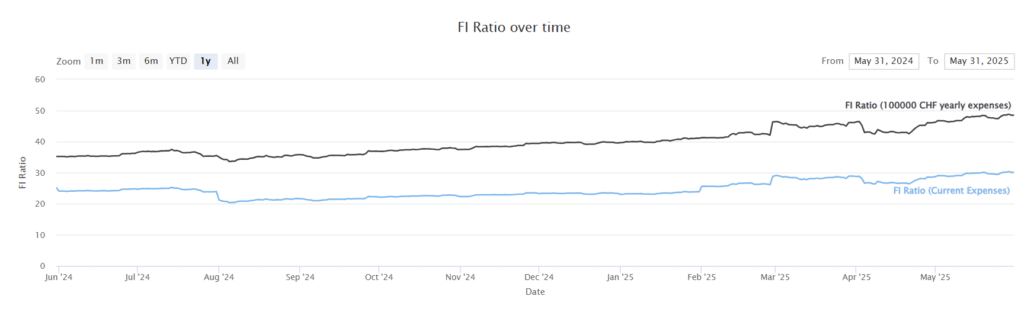

FI Ratio

Here is the progress of our FI ratio as of May 2025:

This month, our FI ratio increased slightly from about 28% to 30%. This is a nice increase given the current status of the world economy.

In May 2025, the stock market was a bit more hesitant than the recovery from April. But we still recouped a part of the losses (at least in USD). VT went back up to an all-time high. CHSPI is not far from its all-time high, either. Overall, our net worth increased well again.

By sheer luck, our Bitcoin, and Ethereum did exceptionally well. However, since we invested a small portion of our wealth, it should not make any difference. We invested to test Swissborg when doing our Swissborg Review. The response to this article was good, so I may do another article about cryptocurrencies in the future. But I want to repeat that people should be careful about investing too much in crypto. It is an alternative investment that is not for everybody. At this point, we do not intend to invest more in cryptocurrencies.

Currently, my forecast is that I should be financially independent in 11 years at 48 years old. So, this is aligned with my goal of financial independence at 50 years old.

The Blog

Overall, not much happened on the blog this month.

I made one small change on the blog. All articles are now showing their featured images at the beginning of the article. Now that I have good featured images for all my articles, I feel it look better with this image being shown more.

I also finished the rehaul of the graphs of the blog, which I started last month. I am now using the same system for each graph on the blog. Unfortunately, I got bitten again by the horrible translation plugin I am using (WPML). And after I redid all the graphs, I realized that none of the translations were updated. And when I configured the plugin to update the translations, it broke most of the graphs. So, I had to redo my code in a very specific way that WPML would handle. And that meant modifying each graph again to use the new system. That was not a high point of the month.

Other than that, I only made minor changes to articles and the usual updates to my articles to keep them fresh. Looking at the statistics, the visits are pretty much stable. I am thinking about ways to increase the traffic, but I do not really know where to start.

Next Month – June 2025

June 2025 should be a fairly straightforward month. We have our usually family weekend planned for June and some nice events with friends and family.

Financially, June should be good but since we will pay again all taxes, it will not be as good as May.

What about you? How was May 2025?

More reading

July 2018 – Getting back up to speed

In July, we started saving more money again and went on a nice trip to Orléans, in France, a very nice city.

August 2019 – Another expensive month

In August, we spent too much, but still achieved a nice savings rate, thanks to extra income.

Eighth year of blogging – Summary

The eighth year of blogging was less active than usual, but the blog is still doing well. Here is everything that happened to it in this last year.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Just curious with your I assume rather big portfolio by now: How much of your net worth at start of the year have you approximately lost in USD:CHF exchange rate change since the start of the year?

Because it already fucks me how I have investments that are up in USD but down actually in CHF compared to what it cost me in CHF to buy.

There is a huge difference this year for us as well. Our VT positions grew from 350K USD to 420K USD (including investments) in USD, but it only grew from 315K CHF to 335K CHF in CHF. So it makes a huge difference for us as well.

Does that make you rethink your current investment strategy? Maybe focus more on buying SPICHA until the dollar stabilises?

Not really, because I am not aware of any better strategy. We cannot forecast the future, so we have to accept that we are going to have lower returns in Switzerland than in the US.

But if you are worried about that, increasing your home bias position makes a lot of sense.

Do you still compute the savings rate by keeping taxes in the expenses?

Yes, my savings rate is always with taxes. This month, we paid little taxes only but should go back to “normal” following months.

Just wanted to mention that Revolut did the same thing here in Romania, but both our personal and joint accounts appear in our name now.

Thanks for sharing, Robert!

I hope this is the next logical step for Revolut in Switzerland. Otherwise, they have done all of this for nothing.

Hi Baptiste,

A big thanks to your monthly review.

However, this may be inappropiate…but did you know that through VISANA you can spare up to 100 to 200 CHF per year just by uploading your workouts with STRAVA or Health. The points, which you earn from your workouts or daily steps, are being converted to CHF and transferred to your UBS or Postfinance account.

Have a nice night.

P.S.: it’s a pity that NEON has changed and applied fees. Yet the abroad draws too…

I used to pay for food with NEON and drinks and big stuff with crypto.com.

Yes, it’s definitely a pity. It remains good, but not as good as before.

Hi Tym

No, I did not know that. But since I am not at VISANA, I am not going to save much by doing that. And I am not sure I would like to share even more with my insurance company.

P.S. It’s best to avoid sharing emails in the comments, this may get you spam.

Note a confusing typo on your e-tax document sentence.

Is it FEE or FREE ? One “r” can make all the difference :)

Thanks, Will!

It’s a dumb typo. It’s for a fee (no r). I will fix this.

Another great article. Love reading your updates regularly. Keep up the good work. Very inspiring :)

Hi Johannes

Thanks, I am glad you like my updates :)