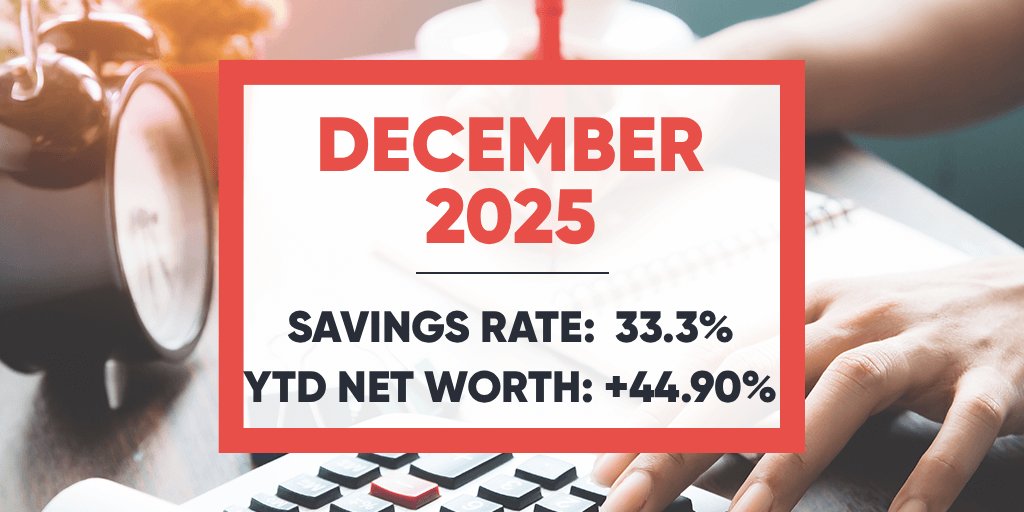

December 2025 – The house is sold and gone

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

December 2025 was a bit tiring, but a good month nonetheless. We had the usual Christmas celebrations with our family. We could do multiple family activities. In parallel, we gave the keys to our old house to the new owner. I am glad this is behind us since it was weighing on my mind.

Financially, it was a good month. We spent a little too much but still managed to save some money. And since we sold the old house at a higher price than we bought it, we got a nice increase in our net worth.

December 2025

December was both a standard December month and an exceptional one. We had the usual holiday parties with our family. We even did a small party for New Year’s Eve, which is something we do not do often. Everything went fine.

My wife and son went for a small trip in Ticino. I stayed home to work a bit on late projects. We will not have much time in the coming months, so we are doing some things in advance.

Except for the holiday parties, the highlight of the month is that we gave out the keys to our old house. We are owners of only a single house, which is great. We hired a company to do the cleaning because we simply did not have the energy to do it ourselves, especially with our son.

The day after the keys were given back, the notary sent us the remainder of the money. It now means we have cash again. This increases our FI net worth since this cash was before blocked into real estate. Additionally, this also increases our net worth because of the capital gains we made. We will look at investing this money again early in 2026.

Another advantage of selling our house was that we got back our life insurance 3a policy. This means we can finally cancel it. We have already sent out the letter to cancel this insurance. I hope it will not take too long. I am really looking forward to having this investment mistake behind us.

Overall, it was a good month. I am happy to start a new year on solid foundations.

Expenses

Here are the details of our expenses in December 2025:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 849 | Expected | Life insurance for 3 people |

| Transportation | 162 | Expected | Mostly buses and a few tickets on holidays |

| Personal | 2267 | Higher than expected | We paid for the trip to Ticino and already booked a hotel for next year |

| Food | 1243 | Higher than expected | Usual groceries and many meals out of the house on holiday |

| Housing | 2545 | Expected | Mortgage and a cleaning bill for the old house |

| Taxes | 7757 | Expected | Taxes at the three usual levels |

In total, we spent 14,825 CHF this month. Without taxes, this amounts to 7068 CHF. If we remove the 1300 CHF from the house cleaning, we spent less than 5500 CHF this month, which is a decent result, although not great.

The most exceptional item on our expenses is the cleaning bill for the old house. We paid 1300 CHF to get it fully clean. It is definitely not frugal, but we would simply not have had the time to clean it up, so I am perfectly happy with this expense.

Other than that, we paid for a hotel in Ticino and a hotel next year for a weekend with our family. While my wife and son were in Lugano and Milan, they mostly ate out, which adds a significant amount to our food budget. All other expenses are pretty standard.

Overall, I am happy with our level of spending for this month.

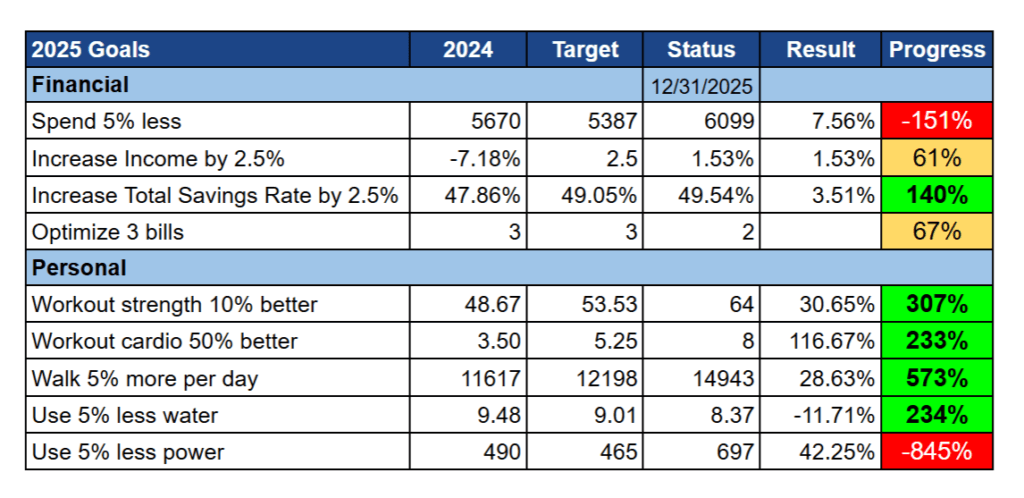

2025 Goals

Here is the status of our goals by the end of December 2025:

I do not want to delve too much into our goals this month. In January, I will do a full yearly review of our goals and present the 2026 goals.

Overall, I would say we had decent progress this month. We spent too much again, but this was to be expected given we had to pay to clean the old house. Income is entirely average, as expected in December. Overall, we have failed three of our financial goals (ironic on a financial blog).

My workout energy was a bit low this month, so I did not do as much as I would have wanted. And as already explained, the power and water goals do not really make sense anymore with the new house. We made good progress on the old house for that, but now we will have to start fresh.

Overall, I am satisfied with our progress this month.

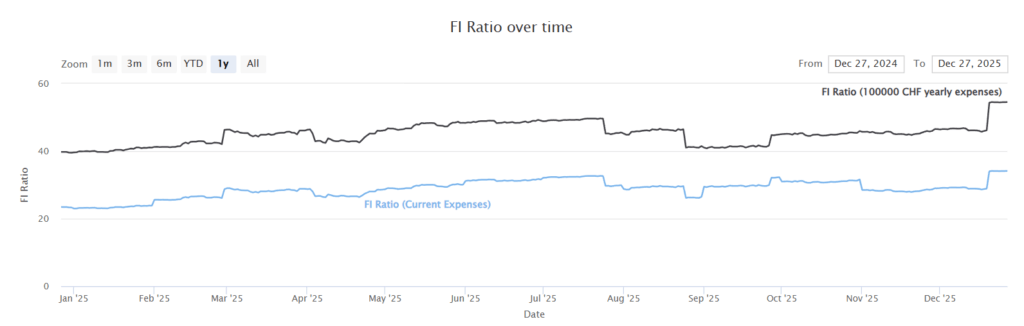

FI Ratio

Here is the progress of our FI ratio as of December 2025:

Our FI ratio did an impressive jump to 54%. This is the first time we crossed the 50% line.

The major change in our FI ratio this month is the effective sale of our house. The money that was stuck in real estate (not in our FI net worth) is now available in cash. Additionally, we made nice capital gains (about 150K CHF) from this operation. We will delay these capital gains into the new house, so we will not pay taxes on it (yet). But together, this significantly increases our net worth.

We know that some of these gains will disappear next year. We have not yet paid the land register for the purchase of the house. And we are planning solar panels next year.

I am entirely happy with our progress towards financial independence. It will take a few years to stabilize, but we are on the proper track.

The blog – New prototype calculator

As usual, I took a 2-week break over Christmas. This helps reduce the pressure on publishing articles and avoid scheduling articles that will have very few readers since people are in holiday mode already.

With some of the members of The Poor Swiss forums, we had a nice lunch meetup in Fribourg. It was nice to see some new heads as well as some known ones. We had nice discussions and touched on many subjects.

I developed a new calculator: an FI planner. The idea is to plan the progress to financial independence and then how retirement will look like financially. If you want to take a look and discuss it, you can check out my post on the forum. You can also comment here, of course, if you have ideas.

While working on an article, I also added a new feature to SWR code: support for extra income in retirement. I have added this feature in the advanced FIRE calculator if you are interested.

Other than that, not much happened. I have not yet had time to start new projects, but that is alright.

Next Month – January 2026

We have very little planned for January. My wife is starting her German course again, which means I will have less time for the blog, but this is a good opportunity for her. Other than that, we do not have much planned for next month. We will ask for estimates for solar panels already.

Financially, it should be a fine month. We do not have any planned expenses or income. We should pay lower taxes than this month since we are done paying federal taxes.

What about you? How was December 2025?

More reading

My 2019 Goals – More Ambitious and Original

For 2019, I have tried to set myself more ambitious and original goals, after goals that were too easy in 2018.

January 2019 – Off to a good start!

January 2019 started the year really well with a good stock market recovery and some nice savings rate.

March 2026 – The bonus goes into the roof

In March 2026, most of our yearly bonus went into the solar roof advance payment. It was a nice and relatively quiet month.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

Since you sold your previous house some months after purchasing your new one, I was wondering how that worked from a mortgage perspective.

Many people see the down payment as the main constraint when buying a property, but in my case the real bottleneck is affordability. With affordability calculation including virtual interest rate of 5%, plus 1% amortization and 1% maintenance, increasing savings for a down payment feels much easier than increasing income.

That made me curious about your experience, so I had a couple of questions:

• When the bank assessed affordability, did they take into account the mortgage on your old house?

• Did the bank require any written commitment to sell your existing primary residence before approving the mortgage for the new one?

Thanks in advance for sharing your experience.

Hi Hur

That’s a good question

* They did take into account the mortgage of the old house. One bank gave us 6 months to sell the old house and the other banks was fine with two mortgages if we sold the old one

* The bank we chose put into the contract that we had to sell the house in 6 months. It was part of the mortgage contract.

Hi Baptiste,

Thank you for your response. That makes sense. With the affordability criteria it seems like you need to make around half a million per year to be able to get a total mortgage of 2.5M so buying a second property while keeping the previous one (even if rented) seems out of reach for most people.

Hi Hur

Yes, a 2.5M mortgage is far-fetched for the vast majority of people.

But if you rent one of them, keep in mind that the rental income is taken into account as extra revenue.

Congrats on the FI ratio jump, this is impressive. I think I recall one of your previous posts where your FIRE number was somewhere around 2+M, which is similar to Marc Pittet’s number. Are you targeting 4M NW or I got all of this wrong?

Hi Nik

Thanks!

Currently, my target is about 2.6M, Marc is much closer than its (2.1M) than me since he is at 90% FI Ratio.

Hi Baptiste, happy New Year and congratulations on the house sale! And DOUBLE congratulations on getting your money back from the notary a day after key transfer. Please do tell how you managed that feat 🤔 !! It has never happened to us before. We have always had to chase 😉 . Liz

Hi Liz

Thanks!

Actually, we did not do anything special. I guess we had a good notary. For the house we bought, the notary also said they would pay the day after the key transfer, so I was thinking it was normal.

How long did it take you to get the money back?

It took us weeks ( 4 or 5?) when we sold our first property (family home) in 2019 and we were not given the 10% deposit until the actual key transfer. We did not have anything lined up to buy directly after but I was quite surprised that I actually had to call the notary office several times before it arrived in our account.

Our current (second) sale was provisionally signed on 17 September with key transfer planned for 30 January. This time we did receive the 10% (minus Neho fee) but only on 23 October after I called several times!

I will keep you posted in January to see how long the final payment takes!

Wow, that’s an impressive difference with our case. We got the deposit a day after the signature as well. I was thinking it would be standard procedure, but apparently we were lucky.

Please keep us posted; this is interesting data!

Sounds like your notary is cheating you since the buyer most definitely has to deposit that or before each milestone? I’d be interested to know if the notary is playing with that money himself for a while aka making profit of it. Sounds like you should consider taking your business elsewhere.

Sali Baptiste

„I am really looking forward to having this investment mistake behind us“

Is it really a terrible idea to have a Life Insurance? What if God-Forbid something happened!

Hi Alex

No, a pure risk life insurance can be a great thing. But a 3a life insurance is usually a bad investment.

Hi Baptiste! Have you done the calculation regarding investing in solar panels and if it’s worth it, compared to investing the amount in equity ETFs?

Hi Dan

I have done it only partially. Financially, solar panels are a good move, and I believe they make sense from an ecological standpoint as well.

We have not yet have offers, but we estimate it will cost us about 50k CHF and it will save us about 2500 CHF a year. We will be able to deduct that, to save at least 10k CHF in taxes and should receive about 5k in cashback for solar. This should give us about 35K net expense, that will take more than 10 years to be financially even.

So, I would say it’s very unlikely that solar investment is better than stocks.

Not everything should be optimized for your own profit, thinking of the environment a little is called for and roofs are just empty space begging to be used for solar power.