December 2024 – A month sick and horrible expenses

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Even though we got a lot of snow (and a white Christmas!), December was not as good as it usually is. I was sick for almost the entire month (and still is now). So, I could not really enjoy the snow as much as I wanted. And my wife and son also got sick.

Nevertheless, I managed to write two new calculators for the blog. Other than that, I could not do much on the blog end. And financially, we spent far too much money this month. We only saved 20% of our income.

So, let’s delve into the details of the month.

December 2024

We had three nice family events this month. It was good to see everybody again and to celebrate the holidays with them. We also had a nice end of the year dinner from my employer.

I was again sick for most of the month. I do not think I was ever sick for that long. It started with a standard cold, which turned into something like a sinus infection. I went to the doctor, and he prescribed several small medicine. And then, when this first phase passed, I got a cold again and ended up with an ear infection. My wife and son also got coughing and my son got conjunctivitis. So, that part of the month was not fun. As of writing this article, I am still sick.

The only good thing is that the timing of the two sick phases was good. In between the two sick phases, we had my employer’s end of year dinner and a meetup for the blog. And I was not too sick for Christmas celebrations (my wife missed one of them, unfortunately).

Financially, our spending was out of control this month. I was thinking we would not spend that much, but we ended up finishing the month on a sad note. We still managed to save 20% of our income, but given how much we spent on avoidable expenses, I think this is a bad result.

Expenses

Here are the details of our expenses in December 2024:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 831 | Expected | Health insurance for three |

| Transportation | 127 | More than expected | Many more buses than usual |

| Communications | 20 | Expected | Phone plan for Mrs. The Poor Swiss |

| Personal | 3839 | Out of control | A lot of shopping, a short holiday in Lucerne, some gifts |

| Food | 845 | Expected | Groceries and a few lunches out |

| Housing | 425 | Expected | Heating and mortgage |

| Taxes | 6542 | Expected | Taxes at the three levels |

In total, we spent 12631 CHF. Without taxes, this is 6088 CHF. This is one of the worst months of the year. I was expecting a result slightly above average, but this is not slightly above, this is highly above average. I am very disappointed in our expenses. All our categories are well managed, but the Personal category is just an excuse for buying everything.

Of course, some expenses cannot be avoided. We had to pay for daycare, and we had to pay for the kindergarten. There were also some subscriptions coming at the end of the year. And we paid several hundreds CHF at pharmacies this month. And we can expect some gifts around Christmas.

On the other hand, my wife did a ton of shopping this month. I also bought a new hat and a new video game. We also bought probably too many firecrackers for New Year’s Eve.

We will have to drastically change our spending habits in 2025. Our expenses are not sustainable at all, that way. I keep seeing this pattern where we simply do not count anymore and this is not healthy. Continuing that route would entirely jeopardize any chance at becoming financially independent.

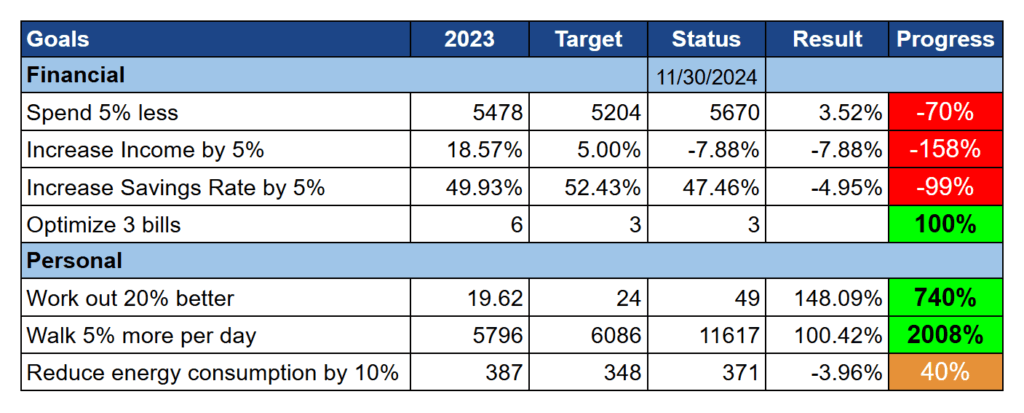

2024 Goals

Here is the status of our goals by the end of December 2024:

This is the last update on our goals for this year. And this result is quite mixed. Our financial goals are in disarray:

- We wanted to spend less, but we spent more

- We wanted to earn more, but we earned less

- We wanted to save more of our income, but we saved less of it

On the other hand, our final personal goals are not too bad.

This month was a bit hectic for my schedule. I had to spend some days in the office where I cannot work or walk on my treadmill. I also spend one day a week at my mom who takes care of my son, and again I have no equipment there. Some days, I was simply too sick to work out. And finally, there were multiple holidays (a good thing) and I do not have any routine on days off, so no working out either. As a result, I worked out less than I should and walked much less than I should.

We did not manage to save 10% power, only 4%. It is not too bad, I think. For some unknown reason, December is also the month with the highest power consumption of this year.

Overall, I do not want to go too much in details over our goals since I will soon do a full review and present the new goals for 2025.

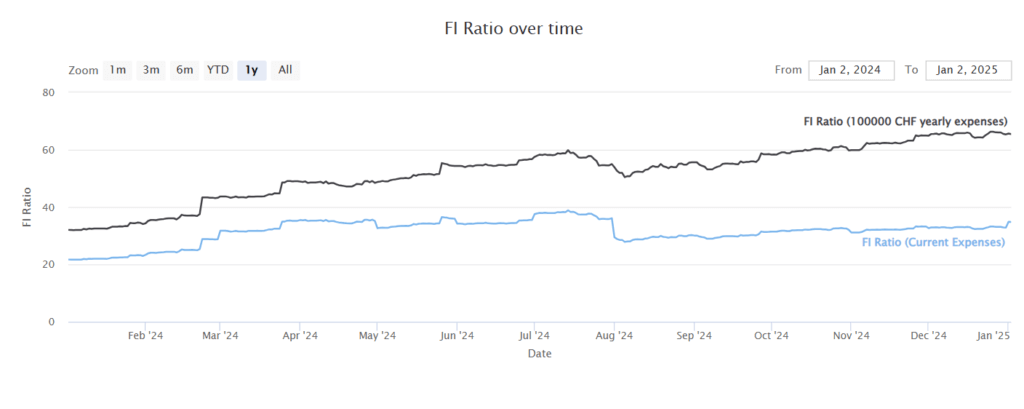

FI Ratio

Here is the progress of our FI Ratio as of December 2024:

Our net worth did not move much in December. The stock market started the month strong, but then declined to end up slightly lower than when it started.

Strangely, our FI ratio still went up. The reason is that we replaced a more expensive month by a slightly less expensive month in our 12 months average (used to estimate our current expenses, for our final target). I am bit torn about that because December was terrible, but compared to the average, it was not too bad.

Overall, given everything else, I am happy about our progress towards FI, even though I feel like we did not do anything to reach it.

The Blog – Meetup and new comparison tools

In the middle of the month, we had a small meetup, organized through the forums. Even though not many people could join, it was nice to see people and discuss money subjects. I did not organize it very well, but it will be better next year. I hope to organize again something in early 2025.

Early in the month, I wrote a new comparison tool for the blog: a credit card comparison tool. The idea is to be able to find the cheapest credit card for your exact needs. This comparison tool is simple, but it fits perfectly within all my comparison tools. I have also upgraded the design of all my comparison tools to make it look better. And later in the month, I was able to write a bank comparison tool as well. I may continue that route in the future for third pillars if people use these new comparison tools.

On a very minor note, I also upgraded the forum to PHP 8.3. This should not make any difference, apart from using a more recent version of PHP. The transition went very smoothly. I hope to be able to do the same for the blog next year.

Other than that, I did very little for the blog this month. I was not very motivated to work on the blog. Hopefully, my motivation will rise next year. And at the end of the year, I was simply too sick to do much.

For the second month in a row, the traffic on the blog is still 30% below last year’s level. Even though traffic is not the most important metric, this is slightly concerning, and this decline can also be seen in the blog results.

Next Month – January 2025

At the end of next month, we will go back to China. This will be the first time our son goes to China and meets the other part of the family (also the first time with such a long flight). This will likely mean I will not be able to access the blog for a while. I intend to try a VPN, but my last experience with VPNs in China was awful.

Financially, it should be a decent month. We will likely pay for the hotels at this point, so that may weigh a lot in the balance.

What about you? How was December 2024?

More reading

June 2025 – E-Book is now available in French

In June 2025, we spent reasonably and had time to translate our e-book in French. Overall, it was a good, although hot, month.

April 2021 – A quiet month

In April 2021, we managed to save 77% of our expenses, with very low expenses and normal income. Find out all the details!

Our trip to Orléans, France – Beautiful City

Planning a trip to France? Read about our visit to the beautiful city of Orléans, including sightseeing tips and travel recommendations.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Is it really worth it to sacrifice 20 years of your “youth” spending as little as possible to stop working earlier?

Which is in most cases not going to happen anyway?

I find that saving 30% of my income while still enjoying life and not feeling guilty about expenses is a more rational approach.

Sacrifice is not worth it, no. But smart spending is worth it. I wish we would stop buying things that are useful for a month or less for instance. Or that we would not need 9 pair of shoes.

Our goal is 50%, which seems reasonable given our high income and relatively frugal (at least in the past) lifestyle.

Hi Baptiste,

Firstly, get well soon. So many people I know have or are sick so best to you for a swift recovery in 2025.

Secondly, This is the single most valuable source of information and discussion out there for us on Swiss finance. It is totally invaluable and I have referred my young adult children to it as well .. so it transcends generations and is very much appreciated. And yes, I purchased the hardback book.

For all of us out there, promote the website/information if you find it useful and share it with your children so they can grow up more informed than we were growing up …….

and buy the ‘Free by 40 in Switzerland’ book .. it’s excellent … so much great, easily to understand information. Takes you on a step by step journey of understanding where you are and how to set yourself up for success in the future. Highly recommended.

Keep up all the invaluable work Baptiste and best for 2025.

Thanks, Richard!

I am glad you refer that to young adult children, I am not sure that blog is talking to them since it’s only a written media whereas I think they are more on video and short videos.

While I have no problem with you advertising it, don’t forget that “Free By 40 in Switzerland” is Marc’s book, not mine ;)

Hi batiste, I enjoyed your blog & I can recommend a good esim which works perfect in china. Even google apps. Send me your email or WhatsApp. I get discount on recommendation.

Which part of china are you going? I did not have issue at all.

Hi Selina

Thanks. Ideally, I would rather avoid an esim, but this is a good idea. My contact information are on the imprint page.

We will be south center china. Last time I tried NordVPN which was highly recommended for China and could not get a single connection working.

This time, I opted for Let’s VPN, we will see how it goes.

Get well, health is the most important thing!

I’ve been reading your blog for a while and find it very intersting and helpful, appreciate your time and effort.

Is there any recomendation for me to to encourage my wife spend less 🙂? How are you alignining your saving with your wife?

We are a single income, 1 kid family, but we spend way too much on groceries and ad-hoc shopping. Last year I managed to save around 25% of the income and I consider that to be a very low amount. I’m not planning to retire early but at this rate we won’t accumulate anything.

Thanks!

Hi David

Thanks!

No, no recommendation on that. We both have some bad spending habits although in different categories (my issue is tech and my wife’s is clothing/accessories). Other than, we are quite frugal for the big tickets. It’s for the accumulation of the “small” tickets that we get bad.

25% on a single income with one kid is not too bad. It also depends on how much income (keep in mind that we have a very large income of 200k+).

For groceries, what I recommend is make sure you are using the proper shop and then if that’s good, then really look at your spending habits (keep the tickets for one month) and see what pops out.

Maybe take a look at this article: 9 Great Frugal Tips to Keep Your Food Budget Low

Thanks, Baptiste!

Oh, unfortunately we are used to certain level of comfort in our life that we’ve maintained for many years and it’s super hard to cut the costs without arguying, especially when it comes to the groceries. That’s why I thought that maybe you have a magic phrase to motivate the partner to spend less 😂

No, I am pretty bad with magic phrases ;)

Groceries has always been easy for us: we eat no processed food, only raw products that we cook ourselves and we still allow ourselves a lot of meat (we eat mostly pork and chicken, occasionally beef) and some nuts as snacks.

So, simply choosing Lidl for us was the biggest optimization. If you are still shopping at Coop or Migros, I would strongly encourage to try at least one week to go Lidl or Aldi, the difference is major.

Really enjoy your blog, please don’t get discouraged by traffic reduction.

And also … what jumped out at me was “YTD Net Worth +52%”. I think you should be very proud and find great comfort in that figure alone. Confirmation that you are on a good path!

I don’t really worry about the traffic reduction. Either it does pick up or it does not, will not change much.

It’s true that the YTD net worth is quite good, but it was also aided nicely by stock market returns. It could have been better with more savings, but indeed, 52% is amazing!

You’re the third person I hear that was sick the entire December, starting with a normal cold and then some kind of sinus infection. And I had it exactly the same – still not entirely recovered – it’s just scary to hear same things from random people so I had to leave this here.

Hi Dan

Yes, this year seems quite crazy.

In my case, it turned out to be pneumonia (diagnosed yesterday only), antibiotics seem to start to kick in now. It’s probably worth going back to the doctor.

Hi,

not all medications are really effective nor evidence based, even if prescribed by a doctor.

Maybe there would have been a way to ‘spend’ less, particularly those without needed med-prescription ?

bye,

Frankie

HI Frankie

On the health side, we could have saved a little indeed on some things. In most cases, we accept quite blindly what is prescribed. And we should be a bit more critical and think about what work for us.

don’t worry about overspending, that was only temporary.

I’m more concerned about your health, you must be so rundown.

Hi Victoria

It’s actually not temporary, it’s been a trend these last few months.

But you are right, that health is more concerning, quite rundown indeed. But getting better with antibiotics now.

how do you manage to get a monthly mortgage of only chf 425

We have a 0.64% mortgage.

Hi, dear Baptiste,

Get well soon !

Selfcritical reflection is always a good thing.

But do not forget to ‘live’.

You and your family can draw fulfilment from

the holidays, f.ex., even if the stay was more expensive

than planned (as it often is). Some time out, anywhere, could also be good for the back pain.

bye, good luck,

frankie

Thanks Frankie

That’s a fair point. In this case, I am not too worried about the holidays, we are relatively reasonable. It’s more about all the “stuff” we buy.