August 2025 – Tired but excited to move

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

We got the keys to our new house! In August, we managed to finalize all the necessary steps for buying the house. We are very happy to start this new chapter of our lives. We have a lot of work ahead of us for moving to it, but this will be done in a few days.

It was a trying month with a lot to do, but we made it! Financially, it was a good month because we received some extra shares. We managed to save 53% of our income, which is quite rare when we pay all taxes.

August 2025

A lot of the month was dedicated to the house, both buying and selling. At this point, we have signed the notary contract, got the new mortgage, and as you read these lines, we have also received the keys to the new house! The new house is now ours! We will move this week (with professional movers this time).

During this month, we had multiple back-and-forths with the notary and real estate agent. We also had to deal with insurance and such. It was stressful because we did not have much time to go through everything.

In parallel, we also had to start selling the “old” house. We opted for Neho for selling the house. We had to prepare the house for the professional pictures and video. This took quite a lot of time. And then, we had to prepare for the viewings and coordinate with the real estate agent. At this point, we have received one good offer, and things look good to sell the house by the end of the year.

Overall, we have reached a great state for both buying and selling, so we are thrilled.

Finally, we also had to deal with my wife doing German courses every morning of the month. Usually this would not have been an issue, but this happened during the daycare and kindergarten holidays, so it was quite difficult to juggle everything. I took many days off, and we also asked our family to help.

I am pleased about the new house, but I am also exhausted. Indeed, I have not been so exhausted in a while (not as bad as when my son was born). The workload will significantly go down once we are in the new house. But I am looking forward to having sold the current house as well.

Other than that, we had nice times with our family and friends.

Financially, it was a good month. We had extra income in the form of shares this month. This helped a lot in increasing our savings rate, which is typically not that high when we pay full taxes. Overall, we saved 53% of our income this month.

Expenses

Here are the details of our expenses in August 2025:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 831 | Average | Health insurance for three |

| Transportation | 336 | Higher than average | Half-price plan, Fribourg TPF plan, and a few train and bus tickets |

| Personal | 2346 | Higher than average | A new table, more than usual trips, some doctor bills |

| Food | 871 | Average | Usual groceries, more eating out than usual |

| Housing | 425 | Average | Heating and mortgage and the new building insurance |

| Taxes | 7757 | Average | Usual three levels of taxes |

In total, we spent 13524 CHF this month. Without taxes, this amounts to 5767 CHF, which is a great result considering the building insurance, which is yearly!

We had more health bills than usual this month. I did a checkup recently, and my wife did a gynecological checkup as well. Adding to that some pharmacy bills, and we have a significantly higher than average health bill this month.

As you can notice, we did not have huge bills yet despite buying a new house. But do not worry, these bills will come in the next few months. We do not expect to save much money by the end of the year. One new thing is that we took out new building insurance with the new house, so we have paid the first yearly bill.

One thing we bought for the new house is a new table. We wanted a strong table for once and spent about 1100 CHF on a table. But so far, this is the only piece of furniture that we are buying for the new house. We know we will have to buy a new closet for our son. And I am sure we have forgotten some things.

We did a minor improvement to our current house by replacing the shower and redoing the joints in the shower cabin. We will have to pay for that next month.

Furthermore, we are starting to think about how our expenses will look next year. We know a few things will change:

- The heating bill will disappear.

- The power bill will increase.

- The mortgage will increase.

- The water bill will increase.

- The taxes should go down (better municipality).

But we will have to wait and see to know exactly the details of these changes.

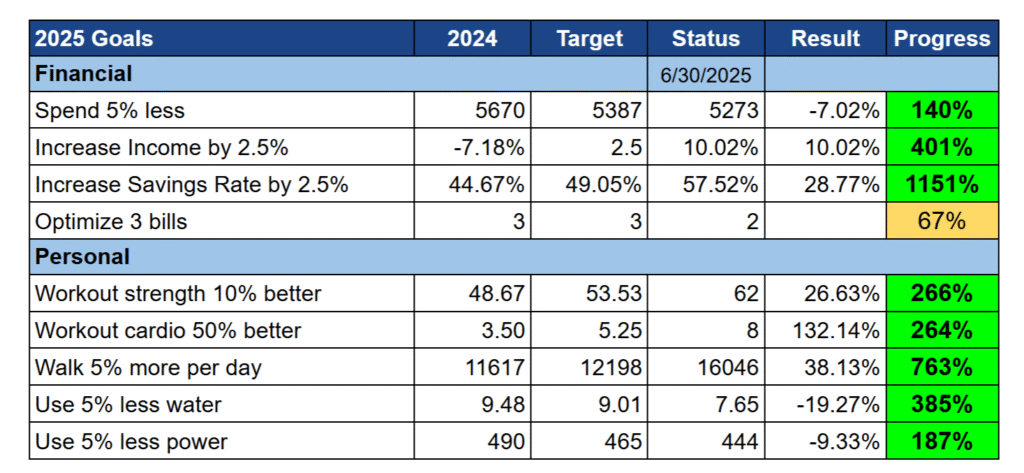

2025 Goals

Here is the status of our goals by the end of August 2025:

Our goals are still doing well, but they are almost all worse than last month. Indeed, our spending has increased, and our savings rate has gone down. On the other hand, our average income went up slightly, thanks to the extra income of the month.

Of course, our new house is hitting our FI ratio goal quite hard. But our other financial goals are still doing well.

My health goals have been impacted significantly this month. Since we had weird organization in the mornings, I mostly did not have time or was on PTO. Since I work out at home, I need to be home and have time to work out for both strength and cardio. In theory, next month should be better, but since I have to be back in the office two days a week, I have not yet figured out the logistics for that. For both workouts and strength, this was the worst month since winter.

September is not going to improve any of these goals. But I hope to get back to a routine in October at least for the health goals.

Overall, given the situation, I am fine with the state of our goals.

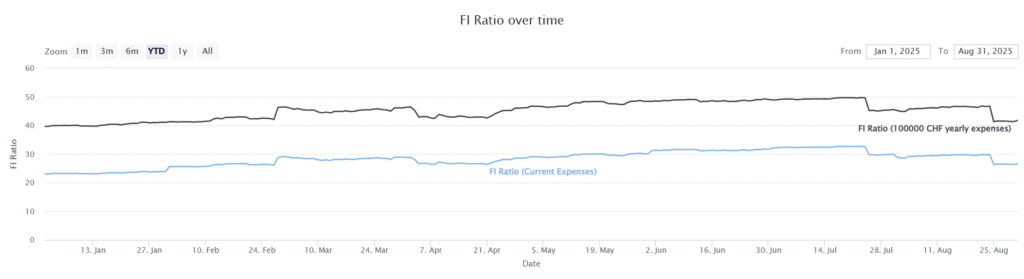

FI Ratio

Here is the progress of our FI ratio as of August 2025:

This month, our FI ratio is now down to 26%.

Our FI ratio has taken another hit this month. We have transferred the second 10% to the notary. Effectively, this means we have a larger part in real estate. This will get slightly better when we sell the current house because this will free some money that is currently locked in real estate as well. But then, we also have to expect to pay massive fees for the land register. So, our FI net worth is not expected to grow much by the end of the year. We hope to get back to growth next year.

Our remaining stocks did rather well this month. Furthermore, our net worth also recovered slightly from the previous month’s loss of USD. However, we are still far from the previous levels of USD/CHF.

Overall, I am pleased with our FI ratio. We are obviously not making progress, but it could have been worse. We will see how we finance the projects we have for the house, but we will balance costs and retirement.

The blog – security and new calculator

Fortunately, I wrote multiple articles in advance in July. This meant I did not have much pressure to write articles in August. This may be an issue for September, but we will have to wait and see for that.

At some point, I realized that our network infrastructure was a bit less secure than I thought. After talking about security with a friend, I decided to dig a little more into it and found a few weaknesses. The status was not bad; it was probably better than average already. I am not a security expert myself, but I am security conscious and prudent about that. I have taken quite a lot of time to fix the weaknesses I could identify. And I will continue after the move with the second phase. I will not go into details, but this is an important task if I want this blog to live for a while. None of these things make any difference to readers; all these changes are under the hood.

This month, I had time (I still wonder how) to write a new calculator for the blog: a pension or lump sum calculator. I should have written this earlier, but it is a nice addition to our calculators. I have already received some feedback and will update with a few things in the following months.

Next month, I probably will not have much time for the blog. At least, I do not have any projects planned. But I have some significant projects for the blog that will likely start next year.

Next Month – September 2025

September 2025 will be mostly about setting ourselves up. We do not have everything figured out. We may have to buy a few more pieces of furniture, but we have nothing urgent. Most larger projects will wait until next year. And of course, we will also have to do a few things for selling the house.

Financially, next month should be standard. Except for the renovation work we did, I do not think we will have any large expenses for the houses yet.

What about you? How was August 2025?

More reading

May 2019 – Finally a cheaper month!

Find out how we saved about 58% of our income in May 2019! We kept out expenses very low and invested all our savings for future returns!

April 2022 – A good month

April 2022 was a good month, with pleasant events with friends and family. The finances were great, with more than 70% of our income saved!

July 2025 – Buying a new house

In July 2025, we signed the contract for buying a new house. Other than that, we did not save much money and had little time for ourselves.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste

Thanks for the update. And congratulations on the new house. All the best!

Very impressive how you have set this monthly tracking up. I have a question – what elements do you include in Savings (53% for August)? Is it what you invest/park in cash on a monthly basis? Or do you also consider amortisation of the mortgage as savings, as an example?

BR

Tarun

Hi tarun,

Thanks, Tarun!

My savings rate is simply (Income – Expenses) / Income. So the savings part (Income – Expenses) can go to any of my buckets. These days, it goes to cash since we will need more of it to cover the future expenses for the house. The 53% of our income is what I have left at the end of the month.

Amortization is not an expense for me indeed since it’s just moving money from one bucket to another. But the interest on my mortgage is an expense since it’s lost.

Hi Baptiste

Thanks for your prompt response.

Okay, understood. So that means whatever you put aside for future expenses in the year (yearly payments, travel etc.) will show up as savings, until the real expense materialises. Which is when it will be recorded as an expense. Correct?

BR

Tarun

Yes, this will show as saving. I don’t count expenses in advance, only when they are paid.

Plein de bonheur dans votre maison !

Thanks, Sophie!

Yay! You finally got your own place. That’s fantastic! Congratulations. Once settled, it may be a good idea to host a small welcome party and invite your neighbours. Break the ice… so to speak?

Thanks, Celine!

That’s a good idea! We will definitely introduce ourselves to the neighborhood.

Congratulations!!!

So happy for you!!

Thanks, Victoria!