Should you pay your bills early in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

A widespread question I hear is whether we should pay some bills early to get a rebate. Some people always pay their bills, and others never pay them early.

So, we will delve deep into this subject and answer this important question in this article.

What can you pay early?

First, we see what we can pay early.

In Switzerland, there are a few things you can pay early to get a reduction:

- Your health insurance bills. Many insurance companies give a small deduction if you pay annually or quarterly instead of monthly.

- Your taxes. In some cantons (depending on the time), you can get a small rebate if you pay all your taxes at once at the beginning of the year instead of using the monthly bills.

There are probably other bills of which I am not aware, but these are the big ones. These are also very significant bills that people must pay, so it makes sense that they are the most interested in paying early.

It is essential to mention that when you pay bills early, you should never use your emergency fund. Paying your bills early is not an emergency; it is an optimization, and your emergency fund is only here for emergencies!

How much reduction can we get?

So, how much of a reduction can you get by paying early?

For health insurance, it will depend on each provider. For instance, several providers give 2% if you pay once yearly: Assura, Visana, Atupri, or Sympany. Others, like CSS, give you a much lower deduction of 0.25%. Finally, some companies like Groupe Mutuel will not even give you a deduction.

For taxes, it will depend on each canton. In the past (in the time of high interest rates), it was a significant reduction. The best I could find these days is Appenzell Innerrhoden and Zurich with a 1% reduction. Schwytz has an interesting deduction of 0.50% as well. But most other cantons are around 0.25%, like Uri. And finally, some cantons have entirely removed the deduction, like Fribourg or Zug.

So, we can save money on these bills by paying them early. Therefore, if we have the money, we should always pay them early, right? It depends.

Opportunity cost

You can invest your money if you are in an excellent financial situation. This means that all your available money will yield some expected returns.

In these cases, we have an opportunity cost for everything we pay. For instance, if we expect 5% returns, paying 1000 CHF now means an extra cost of 50 CHF because this 1000 CHF is not invested. This cost is called the opportunity cost.

You have an opportunity cost even if your money is in an interest-yielding bank account. Indeed, the money you get out of your bank account will not yield any money.

So, whenever we think about paying things early, we should be careful about the opportunity cost.

Examples

We can run through a few examples to get an idea of how much could be saved with opportunity cost.

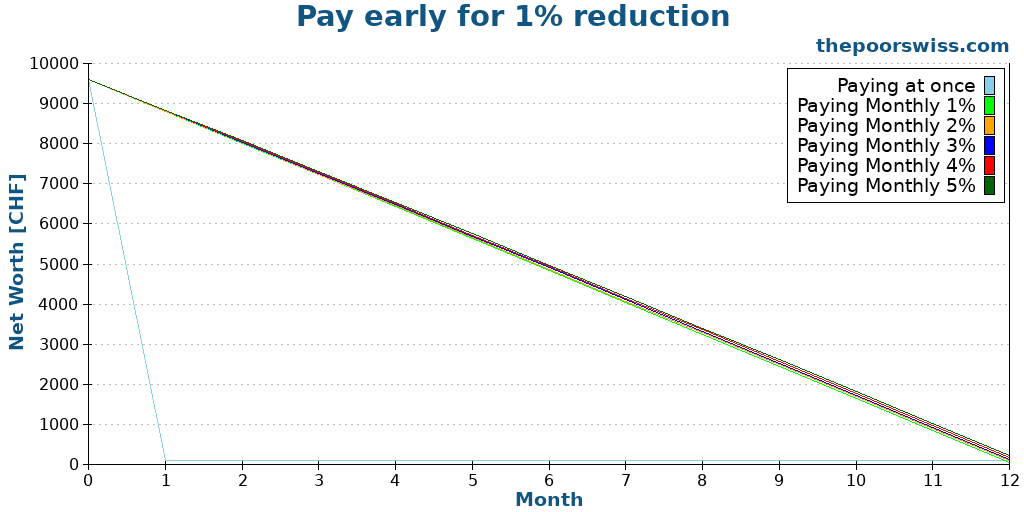

First, we can assume a monthly health insurance bill of 800 CHF. If paid annually, this would be a 1% reduction (9504 CHF instead of 9600 CHF). We assume you have 9’600 CHF at the beginning of the year. And we use different yearly returns to see different opportunity costs.

Unfortunately, the graph is unclear on the differences between the different strategies. So, here are the terminal values for each of the scenarios:

- Paying at once: 96 CHF

- Paying monthly with 1% annual returns: 44 CHF

- Paying monthly with 2% annual returns: 89 CHF

- Paying monthly with 3% annual returns: 134 CHF

- Paying monthly with 4% annual returns: 180 CHF

- Paying monthly with 5% annual returns: 227 CHF

Some people will find these results confusing. Indeed, many would expect 1% yearly returns and 1% immediate rebate to be the same. But they are very different for two different reasons.

First, the 1% returns do not apply to the entire 9600 CHF. Indeed, we have invested less each month, so there are lower returns. Then, if you reduce something by 1%, you need more than 1% to increase it back to where it was before. This explains why you need more than 2% returns to be as good as a 1% instant reduction.

If you get a 2% reduction, you would save 192 CHF at the end. So, you would need 5% returns to get better returns with investing.

So, overall, you should pay your bills early only if you get an excellent deduction or if you get low returns on your investments.

Since getting more than a 2% reduction on yearly bills is rare, most people should not pay their bills early.

Should you pay bills late?

Should you pay bills late if you do not pay them early?

No. There are too many disadvantages to paying bills late even to consider it. If you delay a bill once, you will generally pay a fee for late payment. This is typically a small amount, but added to the original payment, this penalty may make a significant difference.

For instance, consider a dentist bill of 200 CHF. If you delay it by 30 days, you may get a 20 CHF fee. This is a 10% increase in a month! You would need your investments to return around 120% annually to justify this against the opportunity cost.

If you delay even further, you will generally be charged a second late payment fee, which may be more expensive.

Finally, you must deal with the debt collection register if you do not pay after the two general reminders. This means that the other party will ask the debt collection office to get back the money from you. There are many ways for them to do that, but this will enter the debt into your personal information.

You need a clean debt bill to rent an apartment. If you need a job in some companies, this may also come up. Finally, this may compromise your chances of getting a good mortgage.

So, paying your bills on time is very important.

Conclusion

Paying your bills early is rarely worth it if you invest your money. Indeed, paying your bills early means your money is invested for a shorter time, yielding less returns.

If you do not invest your money, paying your bills early is interesting because it is an easy way to save money.

Of course, you have no choice if you do not have the money to pay your bills upfront. In this case, it is more important to improve your financial situation to reach a point where this choice matters to you.

In the past, I used to pay most things early (especially taxes and health insurance), but these days, I have stopped doing that. Since we invest money aggressively, I do not want to forego investing to pay my health insurance at once. Also, we now pay a large amount of taxes, and paying it at once is too much.

What about you? Do you pay your bills early?

More reading

8 Money Management Tips That Will Free Up Time

Even though it is a scary thing for people, you need to have a good money management strategy. Here are a few tips to help you be prepared!

Cars are not always bad for finance

Are cars really money pits? I argue why owning a car in Switzerland is not always a financial mistake and how to minimize the costs of driving.

A few ways to simplify our life

Live simpler. Discover how we simplified our life to reduce stress, save money, and focus on our true priorities.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

I disagree with this conclusion, or at least the analysis for two reasons:

a) You ignore wealth tax. If you pay the bill by December it’s not part of your fortune; and

b) If you pay monthly, effectively you average paying the bill in the middle of the year. So it’s not paying it a year early, but 6 months. So 1% annual interest is effectively 2% over 6 months.

So if you are saving 1% and (say) 0.5% on wealth tax, that’s like getting a guaranteed 3% in cash on an annual basis. Thats decent for a guaranteed return.

Hi Joe

Wealth tax is a good point. I ignored it because the immense majority of people do not pay wealth tax. And people paying 0.5% on wealth are even fewer. A 0.5% wealth tax implies a huge net worth. And in this case, I would not expect any bill to make any difference.

I always set the payment date to the workday after the 25th, so that I have a clear situation on the 1st of the following month about the balance available.

Gives me better control for budgeting.

That’s a good point. I pay everything on the 25th of the month to have a clean picture on the 1st as well.

It’s not very clear to me how the interest rate works in the early tax payment, does it work like a discount as far as you pay before the year ends or as an interest rate applied to the amount of months you deposited the money before the end of the year?

Meaning, is there any difference between an early payment mid-year or in December?

Thanks!

Hi Tomas

Normally, you only get rebate if you pay everything at once in the first month where you received your taxes. There is a date on the tax summary that should tell you how long you have for that.

I have a different view. Paying early is paying respect to the service provider. Like your phone company – you have used their services and you decide to pay when you get the invoice is a value of life. It is an attitude like keeping the door open for the person behind you. Payment morale is poor enough as yearly surveys show. I know people that when the salary is not paid on the 25th they already call payroll. But when they have to pay their bills they wait for the last moment?

It’s a choice.

I am not talking about paying early or late in the standard duration of 30 days (sometimes 10). I am talking about paying in advance, to get a bonus, which is quite different.

I agree with your that paying bills on time is simply a good practice. I have never paid any bill late and would never recommend anyone in doing so. There should not be much difference for the service provider to receive the bill one day after you receive it or 30 days later.

As for respect to service providers, it depends. I have no respect for health insurance companies in Switzerland, should I always pay them late?

In the previous years, I used to pay our annual health insurance bill (~10k for family of 3 in my canton) at the end December. The reason was not an early payment discount, rather easing my life from an administrative perspective (less time to review/approve invoices despite E-bill approvals set-up) and the second reason was to decrease wealth tax of the previous year. E.g. for Basel wealth tax is almost 5 pro mille / 0.5 % ! In other words, 50 CHF per 10K annual bill.

This year I did some math and turns out that I’d rather get the 1% interest from Yuh and pay monthly, rather than paying in advance. However, I’m not sure about investing the entire amount, I prefer to keep the money in my account instead of investing them, because I feel that transferring back and forth to IBKR is a tedious process.

Hi Sol

Convenience is also a good point, you only need to pay 3 bills instead of 36 if you are three people.

The point is that you should not need to keep 10K in your account. You only need to keep 10K/12 in your account and you can invest the rest each month. The main idea of this article applies if you are investing monthly already.

If I have understood correctly, you propose to not pay the invoices early to get these discounts.

I don’t understand this, especially your example. There you would have to invest the money with at least 2.2% return to be slightly better than paying at the beginning of the year. Where do you invest this money to get 2.2% return while having 1) the money available every month and 2) enough security, i.e. no volatility?

Investing money (and by that I don’t mean a savings account) that is needed in the short term doesn’t really make sense to me.

So for me: I pay health insurance premium in advance (have 1% – 2% discount) and only have to check the bill once a year. I pay all other bills on the due date. Paying taxes in advance is not attractive for me at the moment, as the bank interest rate is significantly higher than the prepayment interest rate in my canton (and i don’t invest this money either!).

And another thing: you don’t have to pay tax on this 1% – 2% discount, but you do have to pay tax on the return on your investment – but it probably doesn’t matter (much) :-)

And something else: craftsman’s invoices sometimes have a discount (skonto), this makes sense to take advantage of this.

Yes, I propose it’s not useful if you invest aggressively.

But I think you may have misunderstood the example. It’s not about short-term investing, it’s about long-term investing. It’s not about investing the money to pay the bill, it’s about keeping the money invested. If you need to pay a large sum in cash in advance, this sum must not be invested and this is where it becomes expensive to keep it in cash instead of keeping it in stocks and pay the bills each month out of the salary.

In the past in Switzerland one could pay the bills right away deducing a couple of % “Skonto” (was a common practice). See -> https://de.wikipedia.org/wiki/Skonto

I don’t think there are many cases left (other than the few I have mentioned) where you can a premium, unfortunately.

Very good article thanks !

With taxes, you can have a double optimization when you pay in advance. Let’s imagine you pay in advance your 2024 taxes in December 2023 :

1) You have a reduction for in advance payment

2) The amount paid in advance will not be in your fortune at the end of the year, so less taxes.

My 2 cents.

Hi Tux

That’s a good point. If you pay wealth tax, it good to limit your wealth at the 31.12 mark.

I always pay in time. When I pay the bill I set the date to the date it is due. I know it is not a lot a save. But since you get interest in your account you can make a few CHF a year by not paying instantly you receive the bill.

I also pay my health insurance monthly since interests have returned.

I was thinking about paying bills by credit card with cashback. But the costs are higher than the return.

Hi Daniel,

Interesting, I never thought of that. I always set the data to the earliest possible :)

If we could pay by credit card without fees, it would be great indeed.

Thanks for sharing your strategy!

I also put in the due date usually. Not so much regarding the additional interest (which is nice though), but regarding the increased liquidity I have during the month.

If for some reason an emergency happens, it’s for sure better if the money is still on my account.

Regarding emergency, I am not sure this is a fair point, because paying your bills should not come out of your emergency fund, so it should not change.

But I agree that money is better in your hands as long as possible compared to putting it in the hands of others too early.