How I moved my portfolio with Cash and Market Timing!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I am sure you have heard many times that market timing is bad! I have even said it on this blog several times. But recently, I did some market timing. I had to transfer my entire portfolio from one broker to another. And by the time the money was transferred, the price had increased too much. So I timed the market!

And market timing saved me about 1000 CHF. But do not take me wrong. I still would not advise this to anyone. Hell, I would not even do it again. It would have been much better to automatically transfer my portfolio from my previous broker to the new one!

In this post, I am going to detail how I switched my portfolio from DEGIRO to Interactive Brokers. I used some extra cash to help me. And I ended up timing the market to buy back my shares. You need to keep in mind that my portfolio is relatively small. I only had to transfer about 50’000 CHF worth of shares. Some of the things I did would not have been possible with a much larger portfolio. There is no solution that would fit all situations!

Moving from DEGIRO to Interactive Brokers

Recently, I decided to change my broker. Until now, I was with DEGIRO. I am still satisfied with DEGIRO as a broker. However, they chose to apply European regulations, one year in advance. The result is that I do not have access to U.S. domiciled funds anymore. And the same stands for all Swiss investors.

To be able to invest a bit longer in U.S. funds, I decided to switch to Interactive Brokers. I opened an account and transferred a little money to it. Then, I still had to transfer my existing portfolio from the old broker to the new one. There are several options to transfer portfolios. Either you use an automated portfolio transfer system, or you sell your shares and repurchase them on the new account.

It is important to note than in Switzerland capital gains are not taxed. If capital gains are taxed in your countries, and you are selling and rebuying funds, you may have a significant tax to pay. It would make a big difference. In that case, it would be much better to use the automated way to transfer securities.

1. Using extra cash

I was quite fortunate for my transfer. In February, my ESPP shares were sold. Since my company is American, my shares have been sold in USD. And I have been able to transfer the result of the operation directly to Interactive Brokers. It is about 19K USD that was transferred to my Interactive Brokers account.

You may wonder what does this has to do with transferring a portfolio? It can help quite a bit to have some extra cash. The main risk in moving a portfolio by hand is that there will be a difference between the time you sell the shares and the time you repurchase them. If you are lucky, you can make some returns. But if you are unlucky, you can lose money. We want to minimize this risk.

And having extra cash is one way to minimize this risk! For example, let’s say you have one position to sell with a total of 5000 CHF. If you have 5000 CHF cash in the new broker, you can buy them and sell them at the same time. You are significantly minimizing the risks that way.

Transferring the first two funds

Using my extra cash, I sold the first of my two funds. That way, I could sell and repurchase them almost at the same time.

The first fund I sold is the iShares Swiss Dividend ETF (CHDVD). I have 55 shares of VOO. I sold them at 116.06 CHF per share from DEGIRO. This operation cost me 4.34 in fees to sell them. I repurchased the shares at 116.05 CHF per share form Interactive Brokers. This operation cost me 7.98 CHF in fees. In total, it cost me 12.32 CHF to transfer this position. Minus the 0.55 CHF I made in profit, this is 11.78 CHF in fees. After this, I moved the cash from DEGIRO to IB to start the process again.

The second fund I had to transfer was the Vanguard S&P500 ETF (VOO). I had 25 shares of this ETF. I sold it at 258.07 per share. The very good thing is that I did not pay any fee for selling since this is one of the free ETFs from DEGIRO. I repurchased them at 257.72 CHF per share. For buying, I spent 0.35 CHF in fees. I made a profit of 8.75 with a difference. It is a net profit of 8.40 CHF after the fees. I was lucky on that one. I was not counting on this profit.

Reviewing my portfolio

I have been growing less and less convinced about the SMIM (Swiss Mid-Cap) ETF I had in my portfolio. It took me a long time, but I decided to sell it to simplify my portfolio and make it more stable. The home bias part of my portfolio is here to stabilize my portfolio, not to make more returns. Therefore, the Swiss part of the portfolio will be entirely composed of the iShares Swiss Dividends ETF for now. I am still pondering whether I should simply use the Swiss Market Index (SMI) instead. But for now, I like this choice.

So I sold all my shares of this ETF. Unfortunately, I sold at a loss. But since this money will be invested in what I believe is better stocks, I think it will be a good loss in the long-term. I paid 4 CHF fees for this operation. This money was reinvested into my Swiss ETF to have a correct allocation.

Having to sell your shares and repurchasing them anyway is an excellent opportunity for some rebalancing and cleaning of the portfolio.

2. Market Timing

At that point, I only had one ETF left to transfer, the largest allocation of my portfolio: Vanguard Total World (VT). And this is where it began to become complicated.

Transfer my last ETF: VT

I have 500 shares of the VT ETF. These shares are worth about 36K CHF. This amount is more than the cash I had available in Interactive Brokers. So I could not use the technique I used for the first two ETFs. I can see three ways of doing the transfer:

- Sell everything, transfer the money, and repurchase everything. This technique is the most straightforward. However, this is the riskiest of the three depending on the market. But it is the cheapest in terms of fees and the fastest.

- Use extra cash, little by little. Sell some shares, repurchase them directly with cash on IB, and then transfer the money. Rinse and repeat once the money arrives on IB. However, this can incur hefty fees on IB since there will be many transactions instead of one.

- Sell little by little, month after month. I transfer some money to IB every month. Once this cash arrives, I can buy new shares of VT and sell the same number of shares from DEGIRO. After a few months, everything should be sold. This technique has no risk of market timing, but there are still some transaction costs. The problem is that this will reduce the investments in the first months and make a significant investment after that.

The third technique is a bit too convoluted and slow for me. Even though it may be riskier, I decided to go with the first option. I sold all my shares at 71.26 USD per share. Directly after I sold, the price started to go up, I already started to sweat!

Timing the market

It took several days for the money to be transferred. It took one day for the withdrawal to go through from DEGIRO and then two more days for it to reach my bank. When the money was available in my Interactive Brokers account, the price had reached 73.55. That is more than a 1000 CHF loss compared to the amount I sold for!

So I decided to wait and time the market. Now, I know market timing is a terrible idea. But I still decided on it for a few reasons. First, the market was not in great shape already with the first talk of trade wars and the incoming yield curve inversion. And the market was already close to its all-time high. Moreover, I did not need the market to go down a lot to recoup my loss.

I still had to wait much longer than I thought. The market took two months and a half to go back to the level I needed. I ended up buying back my shares 71.16 CHF per share. This operation makes a small profit of 50 CHF. But since I also did not buy shares during this time, it makes my cost basis for VT lower than it would have been if I had not waited.

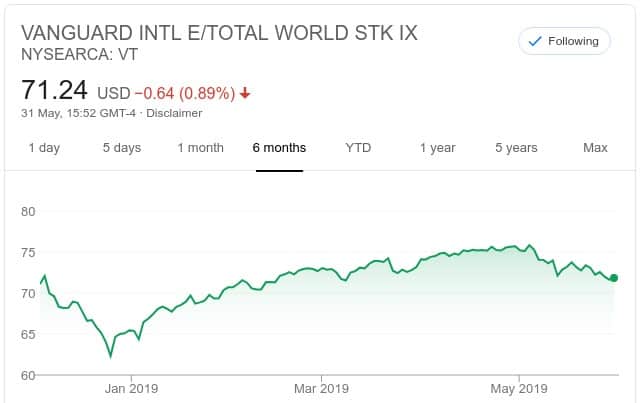

For reference, here is VT during the last six months. I sold at the lowest point of March and had to wait until the end of May for it to go back to this level.

In the end, I was lucky. Luck is all it comes down to! The trade war could have ended the day after I decided to wait, and the market could have gone 10% in a week! I could have had to wait for a year or forever before I could reinvest.

Lessons Learned

I have learned three main lessons while transferring my portfolio from one broker to another.

First, having extra cash to make the transfer much faster is very convenient. This extra cash helped me a lot to transfer my first funds. It may take a little more time that way. Indeed, you have to do several roundtrips with money. But it is safer than letting the market moves between the sell and when the money arrives at the new broker.

Second, and more importantly, the market can move very quickly in a few days. I had underestimated that. That means that between the time you sell your shares, and the time the money transfer gets to your new broker, the price of the shares may have changed a lot. If it went down, you are lucky. But if it went up, and the market generally does go up, you are losing money. It is not a real loss. But you will have fewer shares than before. And this is important!

If it takes three days for the money transfer to go through entirely, the market can have gone up several percentage points. All of this is a loss for you. And it is quickly much more than what you would have paid for the automated transfer of your shares.

And third and foremost, market timing is highly stressful. When I was investing, I was not watching my portfolio very often, maybe once a week. When I was waiting for the market to dip, I was looking at the value of VT several times a day! It is not enjoyable. Even though it helped me avoid a significant loss, it would have been better only using a standard transfer system.

Another small thing I learned is that it is not always possible to move as much cash as you want. In March, I have reached the limit of 50’000 CHF going out of my bank account. Since DEGIRO only allows me to send money to one bank account, I had to send it to my bank account and then to IB. Not only is that slow, but it is also inconvenient because of the limits.

Finally, transferring money is not fast. It took a minimum of two days, sometimes more, to transfer money from DEGIRO to IB. And we have seen that things can evolve very fast in the stock market. It was probably not a good idea to transfer my portfolio like this.

Conclusion

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Overall, I made a small profit of about 40 CHF by transferring all my shares by hand from DEGIRO to Interactive Brokers. However, it took some extra cash and some market timing to make it work!

Given all the downsides of having it done so, I would not recommend this technique to anyone! It was highly stressful, and it is not worth it! I was lucky. It could have been much more difficult. The best technique to transfer a portfolio is to use the automatic transfer system offered by all brokers.

If I had a more substantial portfolio, I would probably have used the automated transfer in the first place. But I did not want to pay for it. So instead of waiting maybe two weeks, I waited two months and a half for the full transfer. Not good, right?

I am hoping that this will be my only experience with market timing.

How would have transferred your portfolio? Would you have used market timing?

More reading

Should Swiss investors worry about the US Estate Tax in 2026?

Avoid the tax trap. Learn about the US Estate Tax for Swiss investors and how holding US assets could expose your heirs to high taxes.

What is Currency Inflation? How to Fight it?

Protect your wealth. Understand the relationship between currency and inflation and how to hedge your portfolio against purchasing power loss.

Broker Bankruptcy: What happens to your investments?

Is your money safe? Learn exactly what happens if your broker goes bankrupt, how Swiss deposit protection works, and if your shares are safe.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Very insightful! Could you please elaborate on how you transferred your money from Europe to IBKR? I am trying to figure out the best way to do so but the fees are just overwhelming, no matter what currency I use. Unfortunately, I don’t have a US-based bank account.

In DEGIRO, you have to liquidate everything in your base currency, so CHF for me. So, I liquidated everything in CHF, transferred everything to my Swiss bank and then transferred everything to IBKR directly. It was slow, but cheap. But I am not sure that answers your question, does it?

Hi Baptiste,

Thanks again for all your great articles!

Do you have experience transferring securities directly (without selling them) from one broker to another? Do you have a rough idea of what the fees could look like?

I opened an account on SQ and they offer 500CHF reduction for transferring securities. What could be interesting to me would be to transfer some US ETFs from IB to SQ and then buy more US ETFs on IB but stay below the amount I’m comfortable having on IB. I’d be happy to hear your thoughts on this.

Hi Eric

I do not have experience with it, no.

However, the fees are easy to find out. Each broker has different fees. There can be fees for transfers in and fees for transfers out. So, each pair of broker may produce different fees.

From IB to SQ, it would be free for instance. I know that several people are doing that. If it help you feel better about your finances, it’s all good!

Thank you Baptiste! I’ll look into it and can report my findings in case anyone is interested.