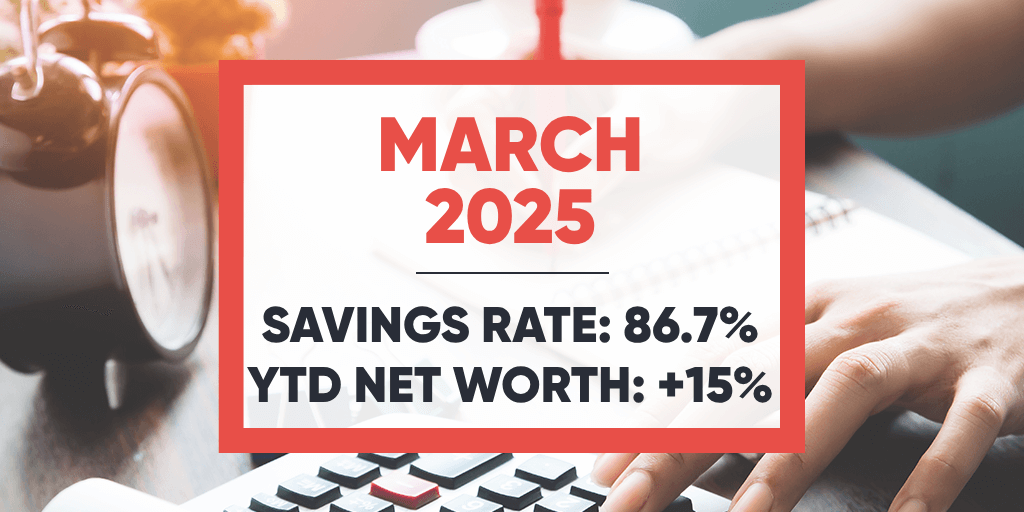

March 2025 – Bonus and splurging (a little)

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

March was a nice month with days of nice weather again. It was great to enjoy some time outside again. We also saw some friends and family.

During the month, I received my bonus, resulting in a significant increase in income. I splurged a little of that income, but only a small portion. As a result, we could save a very high portion of our income. In fact, we realized a record savings rate of 86.50% this month.

March 2025

March was a good month. We welcomed the return of the warmer days and could enjoy some time outside. I even took to work a little outside when the weather and my planning permitted it. We again saw multiple friends and members of the family this month. This was a nice balance between time for us and time with other people.

Our sons’ sleep pattern went back to normal after the disruptions because of the jet lag from China. I am glad he does not wake up anymore during the night.

As usual, March is the month with the highest income of the year. In March, I receive my bonus (based on performance) and it is usually twice more than a standard month’s salary. It means that March income is typically three times the income of a standard month.

Additionally, we do not pay taxes in March. This results in the month with the highest savings rate of the year, usually, by a large margin. We even managed to reach a record high savings rate of 86.50%.

Expenses

Here are the details of our expenses in March 2025:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 831 | Expected | Health insurance for three |

| Transportation | 88 | Higher than expected | Bus and parking |

| Communications | 20 | Expected | Phone plan |

| Personal | 3414 | Higher than expected | LEGO, kindergarten, daycare, and many small items |

| Food | 1524 | Higher than expected | A lot of dining out, groceries and Aligro |

| Housing | 881 | Expected | Mortgage, heating, housing insurance and power |

| Taxes | 0 | Expected | No taxes in March |

In total, we spent 6759 CHF in March 2025. Since we have not paid any taxes during the month, this amount is already tax-free. It is unfortunately significantly above our spending goal.

Since this is the month with the highest income of the year, I allow myself a little splurge every year. Last year, I bought an outstanding espresso machine (still thrilled about it, using it every day). This year, I decided to buy a new LEGO set. I bought the Barad-Dûr set (from Lords of the Rings). I had a lot of fun building it, and my son even helped (although he prefers by far the figurines than the bricks). This set is the best I have assembled.

The month was a bit insane for our food budget. There are multiple reasons for that. First, we went back to Aligro to restock our reserves. Additionally, we had a record number of lunch and dinners outside of home. My wife and son went quite a few times for lunch outside. And I had dinner in a restaurant with a colleague as well. Overall, this is fine and this should not repeat in this way. And of course, we had the groceries additionally, and they are getting pricier.

Additionally, I also bought a few more things for espresso, but nothing as big as an espresso machine like last year.

But apart from these two categories, there was really nothing special in the other categories.

Since this was the month of the bonus, and we allowed ourselves a little more splurge than usual, this is a totally reasonable result.

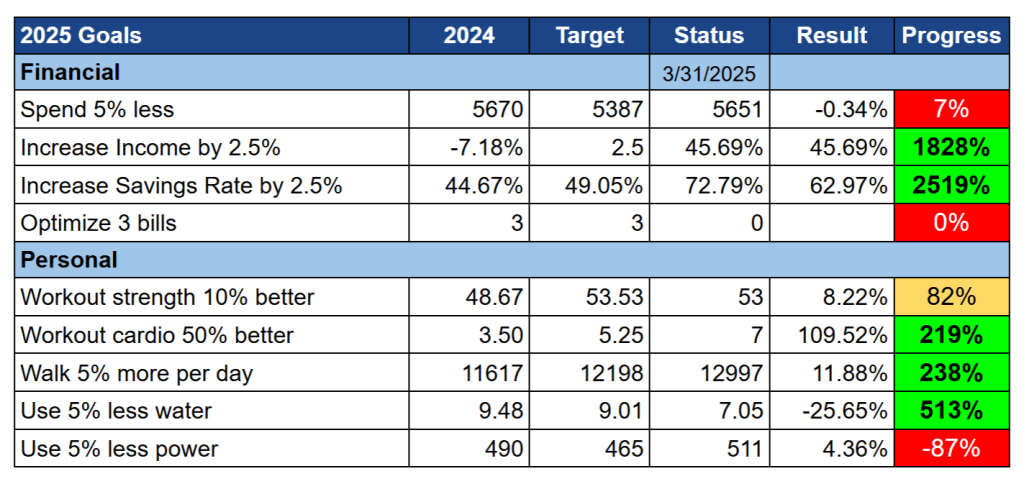

2025 Goals

Here is the status of our goals by the end of March 2025:

Our expenses are obviously not great this month. However, our average expenses are still lower than last year. So, if we manage to get a few standard months, we should be going in the good direction. The average income is also fine, but considering the month of the bonus is also skewing the average. The same is exactly true for the savings rate. These two metrics will go down by the end of the year.

Overall, my strength workouts are doing well. I have significantly improved my numbers this month. And my program is now in a state I want to continue for multiple months. I missed more than I thought, but the average is excellent. My main obstacle is when I have to go to the office. I am happy with the results. I can still improve my cardio workouts, but it is already much better than last year, and I am starting to see progress.

On the other hand. I am starting to have some issues with my under-desk treadmill. There are a few crashes of the app that prevent me from having all the numbers properly. And occasionally, the treadmill abruptly stops, and I also lose the stats (and it is a little dangerous). I am not sure if it will last much longer. This treadmill may not have been made to walk 1800 kilometers in a year.

My power consumption goal is not doing well. We are consuming more than last year and I have no idea why. Each month, we are using more power than we did last year. And we did not change anything significant in terms of power. I am thinking it may be the water boiler, but I have no proof yet. I will try a new mode on it and see if it makes any difference. If I have time, I will see if the consumption moves when everything it turned off.

Our water consumption is lower than last year, but this month was no better than January (I ignore February because we in China). I was expecting a higher impact because of changing shower heads. But it did not make much of a difference.

Overall, our goals are doing well. We need to focus on stabilizing expenses and figure out what is happening to our power consumption.

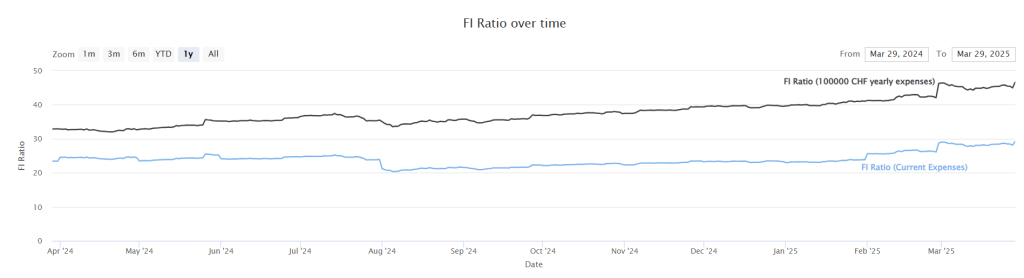

FI Ratio

Here is the progress of our FI ratio as of March 2025:

We had a small progress this month, from 29.02% to 29.20%.

Stocks have not been great during this month, amid all the uncertainties. During this month, we have lost money from our portfolio. On the other hand, the extra savings from this month’s bonus helped alleviate the drop in stock prices.

Our expenses have also gone down (very) slightly. So this will reduce our target starting with next month. But since this month is special (no taxes and splurge), it is not very representative.

We have not invested in stocks this month, but contributed to our second pillar. I plan to start investing in stocks again next month. I just used my bonus to top up our second pillar to save on taxes.

Overall, I am fine with our progress. I wish the large bonus could increase our ratio slightly more, but there is nothing we can do about the state of the stock market.

The Blog

A few things happened on the blog this month.

While I was in China, there was an incident with a lot of traffic going to the blog. This turned out to be an issue with bots doing a bad request and this request not being cached by Cloudflare (most traffic stops there). Unfortunately, I was quite late when coming back, so it took me two weeks to realize this was happening. I was able to mitigate the issue, but it probably made the website much slower for almost a month. I have improved the system so that it should not happen again, but I will need to be careful about these incidents in the future, showing that I most likely do too many things. I also have to up my game in terms of monitoring.

Last month, I mentioned that the traffic had become much lower on the blog. And this month is even worse. In March 2025, the blog had twice fewer visitors than in March 2024. This may be the beginning of the end of the blog. We will see how this continues in the new few months.

On a brighter note, I have released a new calculator to compute whether contributions to second pillar are worth it. I should have done that a long time. I was prompted by a colleague (thanks Florent) who did something similar. Furthermore, I also did the same for the third pillar here, which is almost the same. I hope these calculators are useful.

After having moved some money to our Swissquote account for the blog. I also decided to create an IB account for the blog. I could create it entirely online in less than 5 days. When I compare this to Swissquote where it took me more than two months, I am shocked at how bad Swiss banks are compared to the competition. The fees will be much lower with IB, and it was simpler to open a corporate account.

I also took some time to fill up the blog taxes for last year. There was nothing special on this account.

Early in April, we will have a meetup with some readers of the blog. This was organized through the forums. I am looking forward to it.

Next Month – April 2025

In April, we have a few more things planned, but not too much either, it should be a good month. I hope we will have some more nice weather to enjoy the outdoors.

Financially, it should be back to a normal month. Since it is my birthday, I usually buy myself something (I am thinking about another LEGO), but it should not weight that much in the balance.

What about you? How was March 2025?

More reading

June 2024 – A good month

June 2024 was a nice month, with nice family events but weird weather. Financially, it was a strong standard month with a 43% savings rate.

June 2025 – E-Book is now available in French

In June 2025, we spent reasonably and had time to translate our e-book in French. Overall, it was a good, although hot, month.

April 2022 – A good month

April 2022 was a good month, with pleasant events with friends and family. The finances were great, with more than 70% of our income saved!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello,

I’ve got a question regarding the current situation about the dollar depreciating.

I feel confident about just DCA buying stocks also in a market correction or crash, just the valuation changes and long term debt of the USA makes me nervous about the dollar. I would feel more secure being all in Swiss Franks.

The Zurich Kantonal Bank says that currency hedging is quite costly

https://www.zkb.ch/en/blog/asset-management/2022/hedging-fx-investments.html

Why does truewealth say the costs are minimal, are they lying to lure customers by not informing about the real costs?

https://www.truewealth.ch/blog/improve-your-long-term-returns-with-currency-hedging

My current Portfolio is 70% VEVE (Developed World) and 30% CHSPI. Thank you for the cool website.

Kind regards,

Jimmy

Hi Jimmy

Unfortunately, currency hedging is something where many people disagree. My take on it is that it is a good tool for the short and medium terms, but should not be used for the very long term, because it will incur costs. I wrote an article about that: Should you use currency hedging in your portfolio?

I don’t think TW is trying to lure customers. They have an option to disable hedging.

Here are two videos on the subject I quite liked:

* https://youtu.be/YLIlzdDDDiE?si=-eO7WQc_fVHzvTOM

* https://youtu.be/K3flJjh00gA?si=cqHrek1cdgaRB48d

Thank you very much about the reply. Yes it’s a hard subject i’m tending not to hedge because i already have a home bias and i likely won’t retire in Switserland.

I just wonder if it will still be worth hedging because the Franc always seems to appreciate to other currency’s long term? We have much lower debt and inflation then the USA and Euro-countries? What is your opinion on this? This would make it usefull for anyone to hedge to CHF, even if you not live here?

Another question i have is: in the current situation its only attractive to invest in real estate, domestic stocks and international stocks (vt or another etf). Gold is an alternative investment and already skyrocket. There are no high yield swiss saving account or good bond returns, and it makes no sense to hedge them.

Are you building a secure part of your portfolio? Like instead of a high yield account just building your % of cash position over time? Or do you keep a fixed emergency fond for 6 months no mather how big your portfolio is?

Kind regards,

Jimmy

Hi Jimmy

I already think it’s probably not useful for somebody living in Switzerland. But it’s definitely not useful for a person not living in Switzerland.

I have a small emergency fund for two months of expenses. If I need something safer, I can use my second pillar to fill its gap which I do once a year. But other than that, we only invest in stocks.

Hey Baptiste,

Thanks for your blog! I wonder if you have any thoughts on investments during this economically volatile time? :) Especially regarding the recently announced US tariffs. How can we save our portfolios? What is best to do in Switzerland? I don’t know – maybe it would be enough even for a new blog post?

Thanks!

Hi Alex

My strategy never changes: Keep investing no matter what and ignore the noise :)

In the long term, just keep buying is a great strategy.

Hello. What is the espresso machine that you bought last year? I need to replace mine and am looking for suggestions :)

Congrats on the great content of your blog.

Hi Pedro

I bought a Profitec Pro 700. It is probably overkill, but I am very happy about.

Thanks!

Hey. March was very good for me as well. After receiving a bonus, I am “struggling” with investment decisions (yeah, first world “problems”). I wonder how deep the stocks will tank due to Trumponomics and other factors. It seems to be a good moment for a bullish investor now.

BTW, happy birthday : )

Hi Päuli

Thanks! And congratulations on your great month of March as well.

It’s indeed a good problem to have. Take your time and try to think about the long-term view and not the short-term one.

The almost sudden fall of readers seems a bit strange, as an avid Reader I obviously like reading your Blog and don’t see an obvious reason why people would be less interested now. I will definitely miss the Blog if you would decide to stop.

Hi Josh

I am not planning to stop at this time. I don’t know either why it would drop so much. It may even be due to reporting at this point, but I don’t really have the time to do much digging. We will see how that develops!

Hey, Baptiste,

Thanks for the update!

You mentioned that you decided to top up your 2nd pillar instead of stocks to reduce the taxes, however, considering >5 years till retirement, it usually is more attractive to purchase stocks over 2nd pillar, right?

Additionally, taking into account good correction on the stock market in the recent months, it is even more profitable (in the long-term), to invest in stocks now – you can buy more for the same $ investment.

I wonder what your thoughts are on this one…

Cheers!

Hi Mikolaj

My thoughts are mostly that I am planning for early retirement and investing medium sums (we aim for 30K per year) seems to make sense for us. It reduces our tax burden significantly (Fribourg is awful for this).

I would not invest all in the second pillar.