Les robo-conseillers peuvent-ils être moins chers que les courtiers ?

| Mis à jour: |

(Information: certains des liens ci-dessous peuvent être des liens d'affiliation)

My favorite way of investing is through a broker, directly in ETFs. I find this the most efficient way of investing. For many people, the alternative is using a robo-advisor.

I have always claimed that brokers are cheaper than robo-advisors. But is that really true? To find out, this article will compare multiple brokers and multiple robo-advisors and see whether robo-advisors can be cheaper than brokers.

Scenarios

To compare brokers and robo-advisors, we will compare them in multiple scenarios.

Our main scenarios will be based on varying investment amounts and varying portfolio amounts. Both parameters are essential because generally robo-advisors have no transaction fees but higher custody fees. On the other hand, brokers have transaction fees but lower (or even zero) custody fees.

I obviously cannot compare every single monthly investment value and every single portfolio value because this would make this article infinite. But I hope that by comparing some standard values, you can get an idea of where the breaking points are.

We will also consider the tax efficiency on US dividends. Not all brokers and robo-advisors are equal in that. This can make a significant difference in total fees, since you cannot always reclaim the US dividend withholding.

I also need to choose a portfolio itself. Indeed, the portfolio will make a significant difference in how much currency exchange will be necessary. And currency exchanges are often a good comparison factor between brokers. In each case, we will use two ETFs: one world ETF (either VT or VWRL, depending on the broker) and one Swiss ETF (CHSPI). The weights will be 75% world and 25% Swiss.

For the sake of simplicity, all dividends will be kept as they are received. They will not be reinvested nor converted to the base currency (CHF).

In these results, I will compare the total costs of each scenario. So, I will not only compare the fees of the brokers or robo-advisors but also the TER of the funds being used and the taxes lost to US dividends if the service is not efficient in that matter. Most people forget these when doing comparisons, but they are important because brokers often allow you to have a cheaper portfolio than a robo-advisor.

In some cases, we could also compare the case of simply holding the ETFs. This will simply compare the custody fees of the two alternatives. This is not always interesting because some brokers have zero custody fees, so they will win regardless of the amount in the portfolio. But this can give an idea of how much we can save with a broker.

I will only use my favorite brokers and robo-advisors. The reason is that a bad broker would simply look bad. If you want me to compare against other brokers or robo-advisors, please let me know in the comments below, and I will see what I can do.

With all the setup done, we can now try to answer whether robo-advisors can be cheaper than brokers.

Swissquote vs robo-advisors

Tout ce dont vous avez besoin pour commencer à investir en bourse. Créez un compte Swissquote et gagnez 100 CHF de crédits de frais avec mon code MKT_THEPOORSWISS.

- Courtier Suisse

- Facile à utiliser

We will start with Swissquote as the broker. Swissquote is the most used of the Swiss brokers, so it makes sense to include it. It is not the cheapest of them, but it is relatively affordable.

Swissquote has custody fees with both maximum and minimum. And there is an unbound custody fee for portfolios above one million CHF. The fees for the transactions are following a progressive tiered system. Since Swissquote is a Swiss broker, you will have to pay Swiss stamp duty.

For the comparison, it is important to note that Swissquote has access to US ETFs. So, it will have an advantage against robo-advisors without US ETFs.

Swissquote vs Selma

We can start our comparison with Selma, a robo-advisor mostly aimed at beginners, by being simple to use. It is not the cheapest robo-advisor, but it has reasonable fees. They have degressive custody fees that are going down rapidly; the minimum is already reached at 500,000 CHF.

Selma uses European ETFs, so we lose the US dividend withholding. Swiss stamp duty is also due on each transaction, and currency conversion is not included in the custody fee.

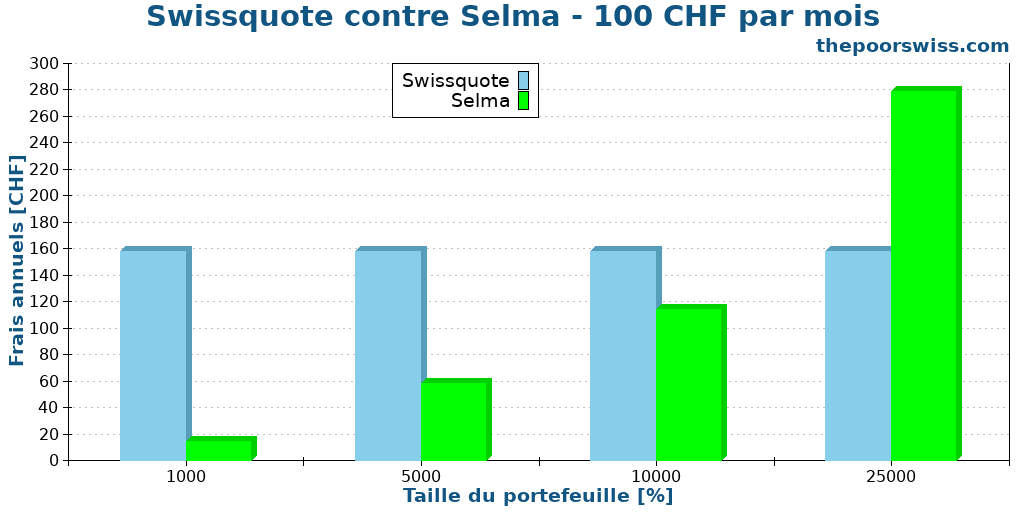

Here are the results for a 100 CHF per month investment.

For a small portfolio, Selma can be significantly cheaper than Swissquote. These results are already starting to say that robo-advisors can be cheaper than brokers. In this case, the minimum custody fees of Swissquote are weighing heavily in the balance. And for small portfolios, the transaction costs of the broker are larger than the custody fees of the robo-advisor.

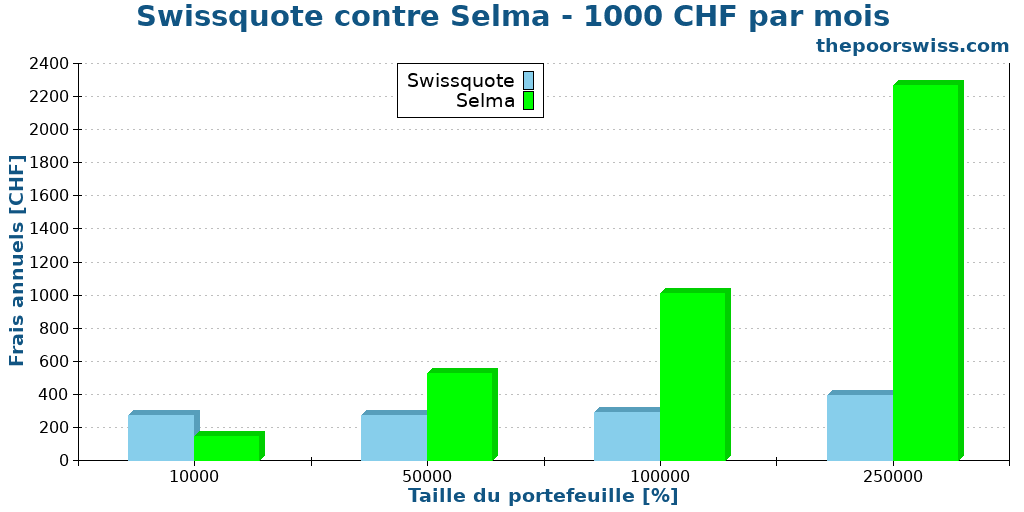

We can see what happens if we raise the monthly investment to 1000 CHF.

Again, as the portfolio grows, the advantage grows in favor of Swissquote. The reason is that custody fees of robo-advisors have no maximum, while Swissquote has a relatively good maximum. Moreover, the higher TER and lost US dividends withholding are starting to weigh on the balance.

Nevertheless, Selma still manages to be cheaper than Swissquote with a portfolio of 10,000 CHF.

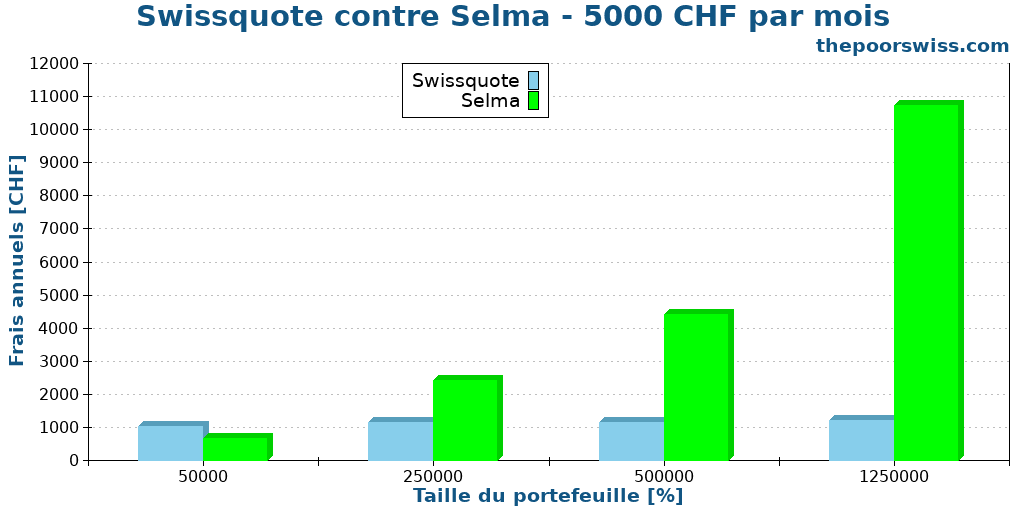

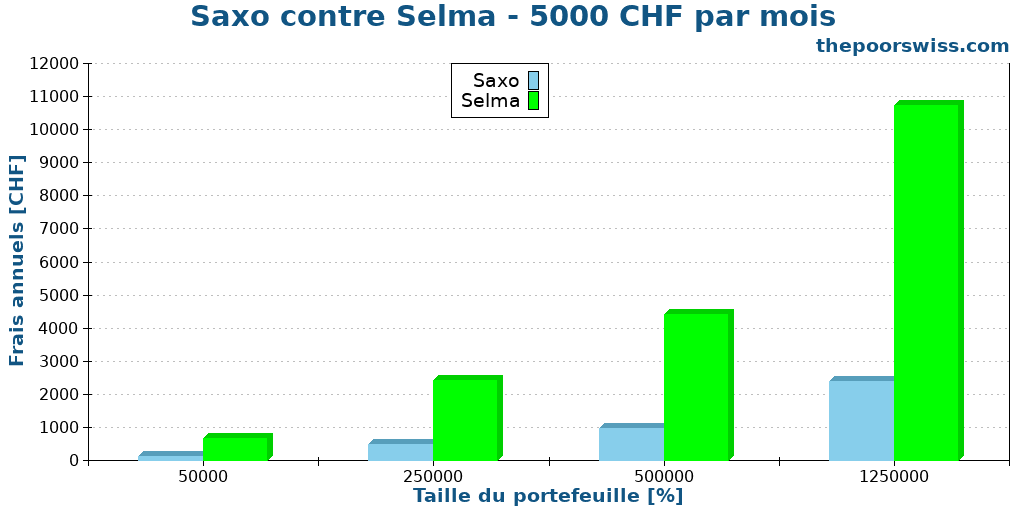

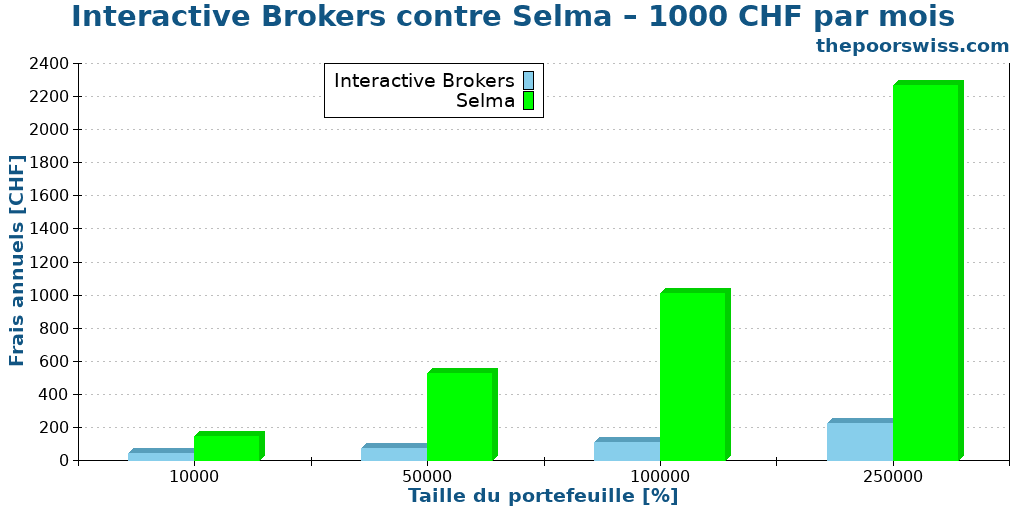

Finally, we can raise the investment to 5000 CHF per month.

Even at this level of investment, Selma can be cheaper than Swissquote at 50,000 CHF. This is mostly because of the high currency conversion of Swissquote, which adds high fees.

However, after this, the differences can become quite significant. For the biggest portfolio, you could save 8000 CHF per year.

So, overall, Selma can be cheaper than Swissquote if you do not have a large portfolio. If you want to invest low amounts and do not plan to reach a large portfolio, it may be best to opt for Selma. But for a large portfolio, Swissquote may be much cheaper. This already paints a picture that robo-advisors can be cheaper than brokers with small portfolios but become expensive as the portfolio grows.

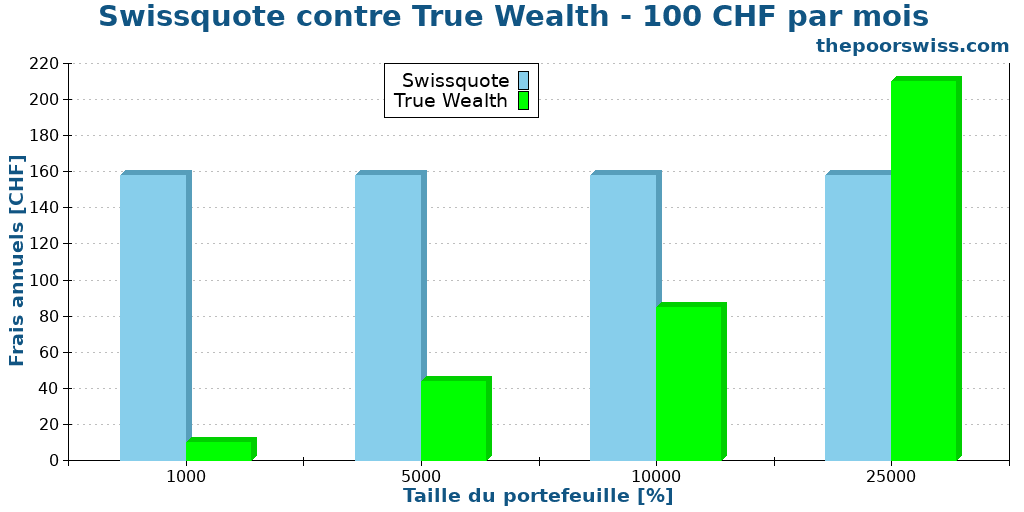

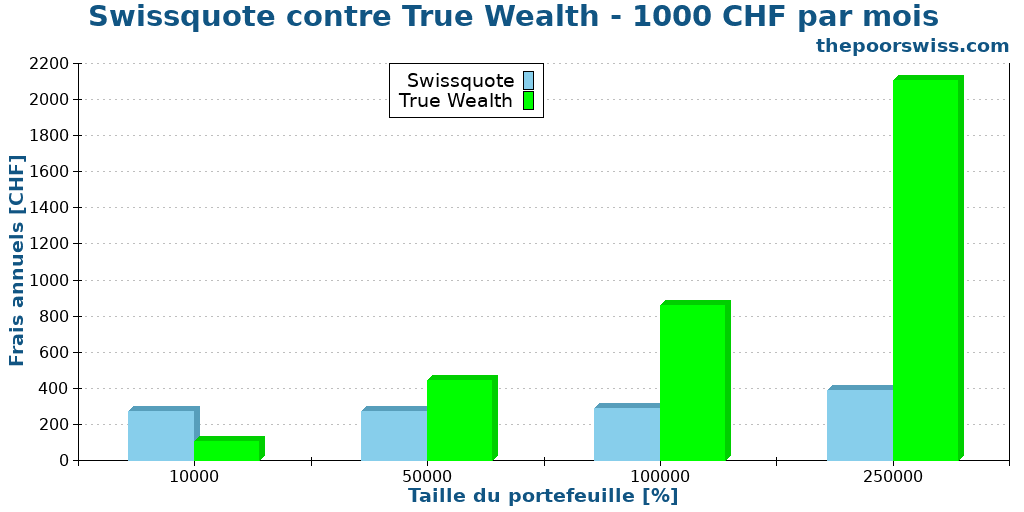

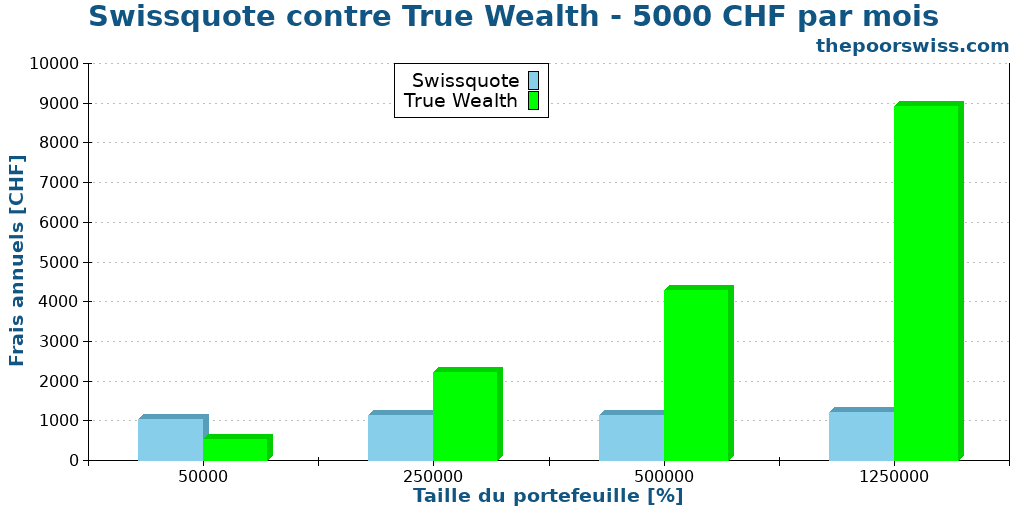

Swissquote vs True Wealth

TrueWealth est un excellent Robo-Advisor, à un prix très abordable. C'est le Robo-Advisor le plus adapté pour les investisseurs sérieux.

Utilisez le code SWISS100 pour recevoir un crédit de frais de 100 CHF.

We can continue our comparison with True Wealth. It is the most mature Swiss robo-advisor. It has very affordable fees, a high level of customization, and a good level of features. True Wealth has degressive fees, but they decrease very slowly. You would need 8’000’000 CHF in your portfolio to reach the minimum fees.

Since True Wealth uses European ETFs, you cannot get back the US dividend withholding. Furthermore, since it is Swiss, you will pay Swiss stamp duty (not included in the custody fee). The currency exchange fee is also not included.

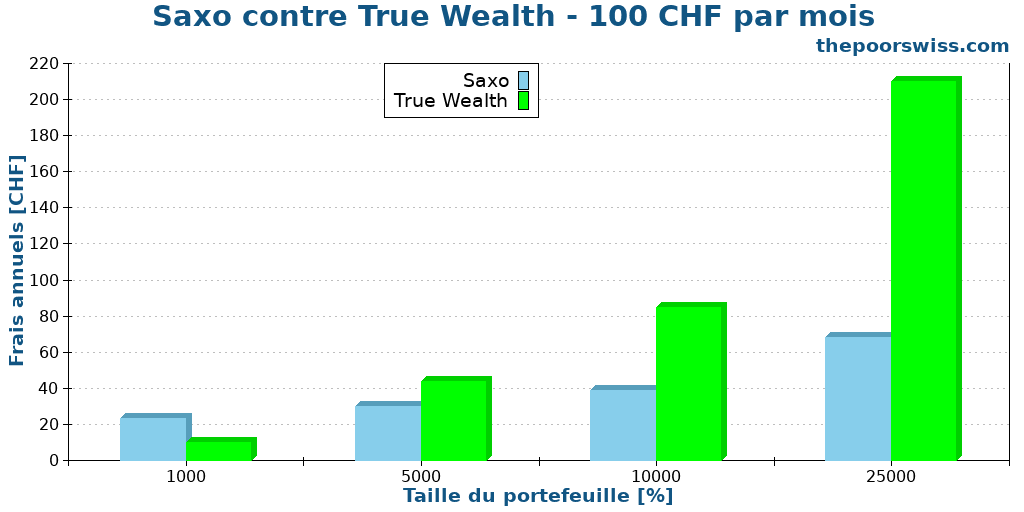

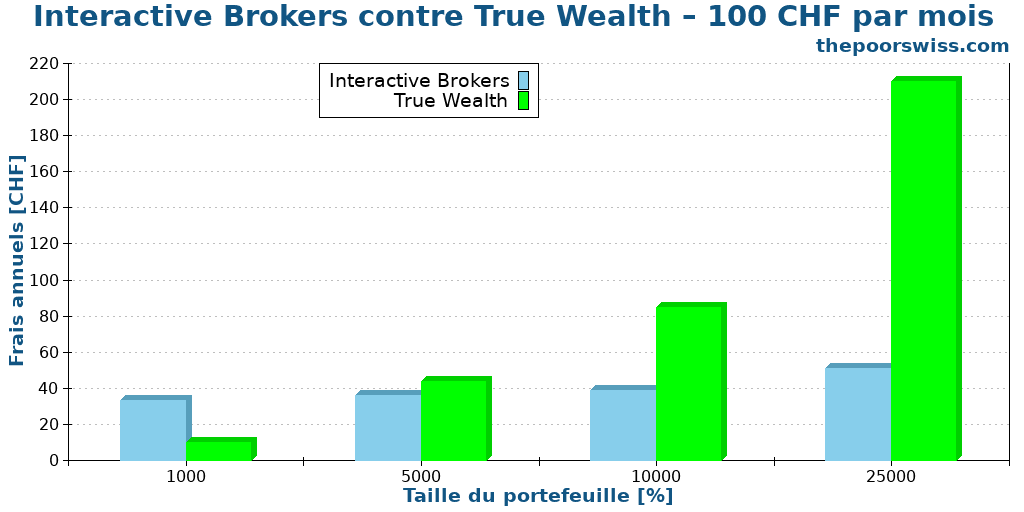

Here are the results for a 100 CHF per month investment.

We can see that True Wealth can be significantly cheaper than Swissquote up to 25,000 CHF in portfolio. And even at that level, both are relatively comparable. For a tiny portfolio, True Wealth can be more than 10 times cheaper.

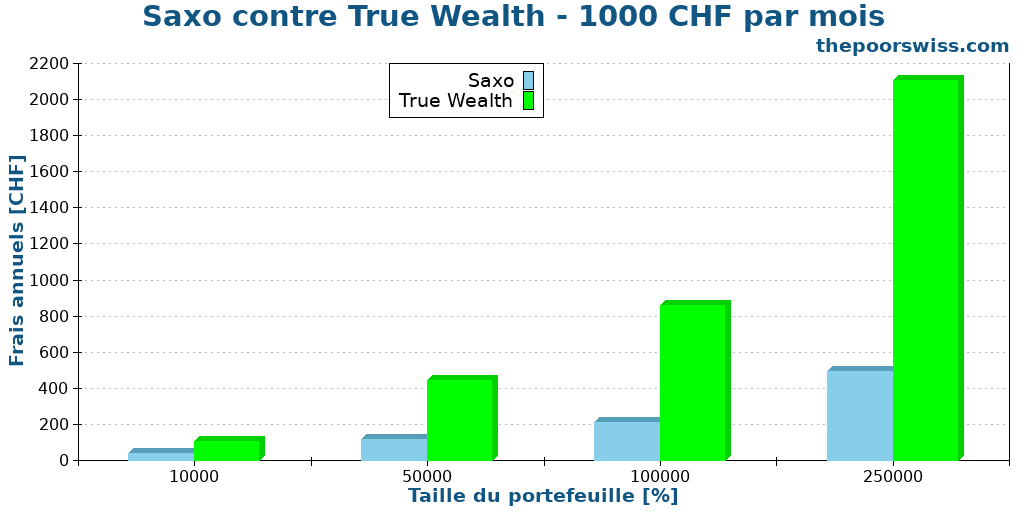

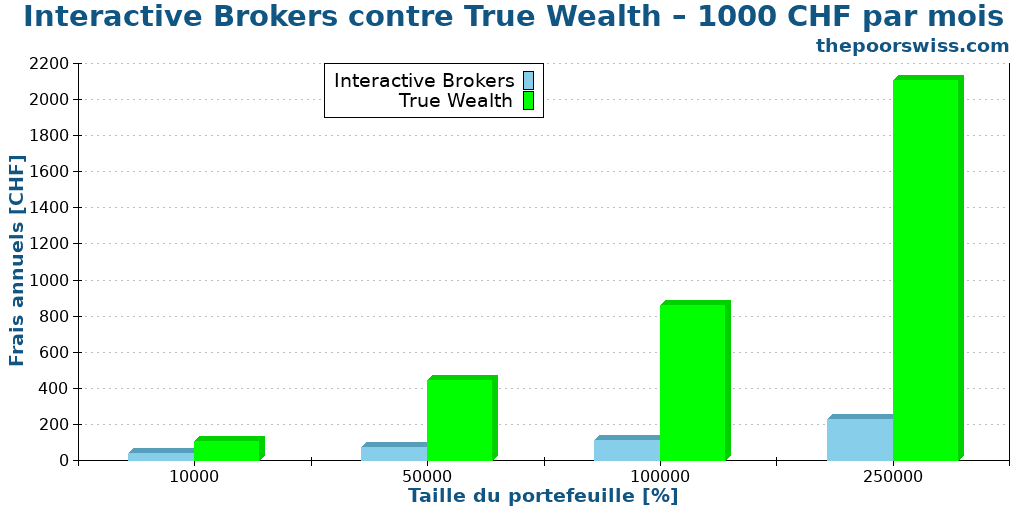

Here are the results for a 1000 CHF per month investment.

Again, we can see that as the portfolio gets bigger, Swissquote gets a strong advantage. At the biggest portfolio, Swissquote can be almost four times cheaper than True Wealth.

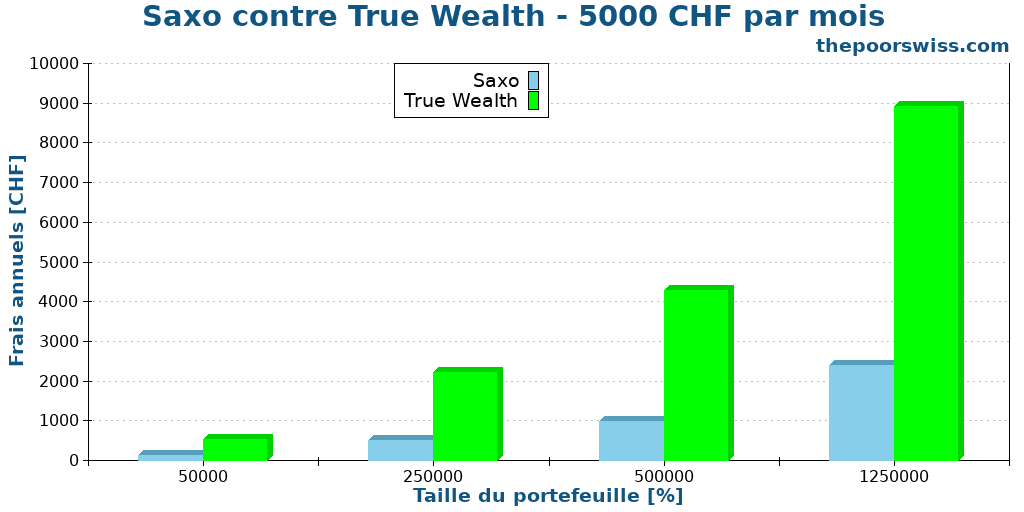

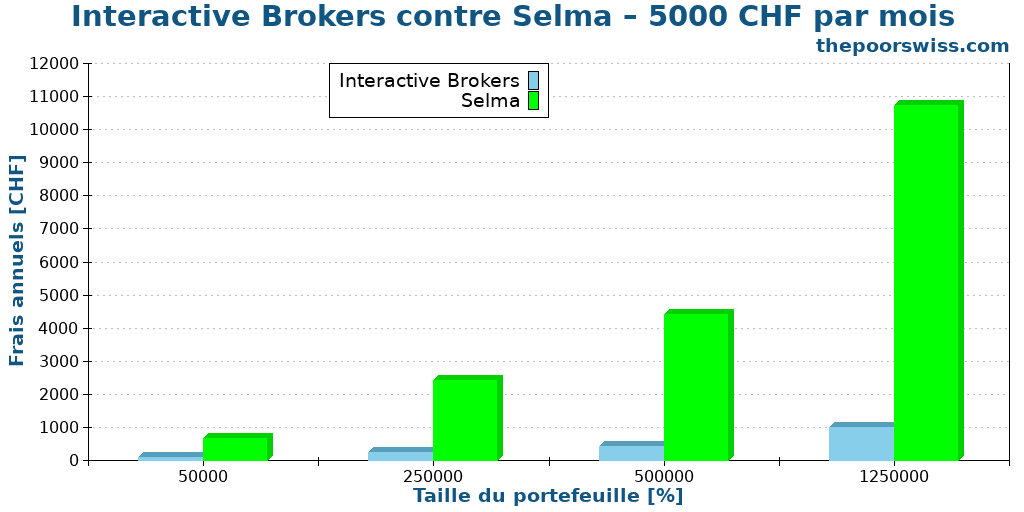

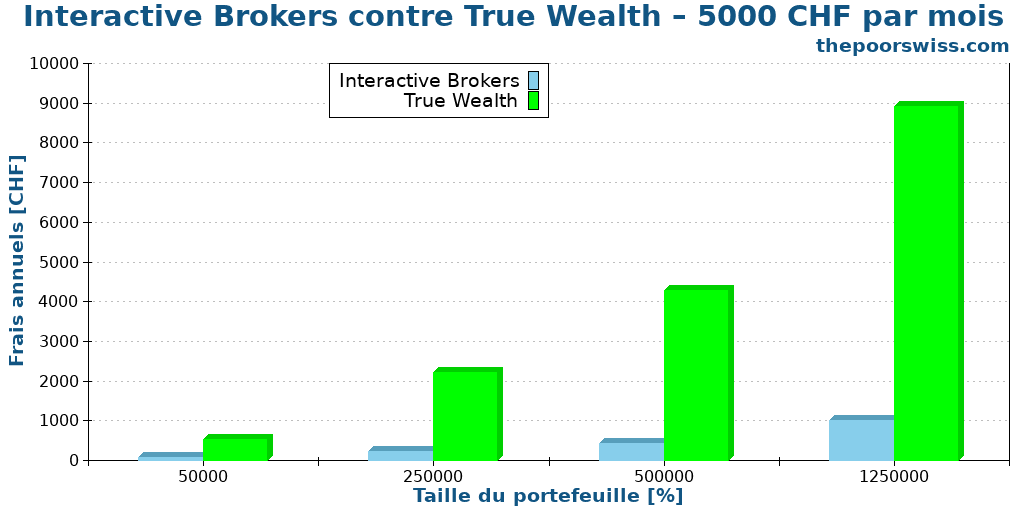

Finally, here are the results for a 5000 CHF per month investment.

In this case, True Wealth still manages to be competitive on the first two levels of portfolios. However, at the highest levels of portfolios, the difference in fees is considerable. With the maximum portfolio, you would pay 6900 CHF per year more at True Wealth than at Swissquote.

True Wealth can be cheaper than Swissquote for small and medium portfolios. It may be an interesting option if you do not have high financial goals. But for a large portfolio, you would pay a very significant premium for using True Wealth.

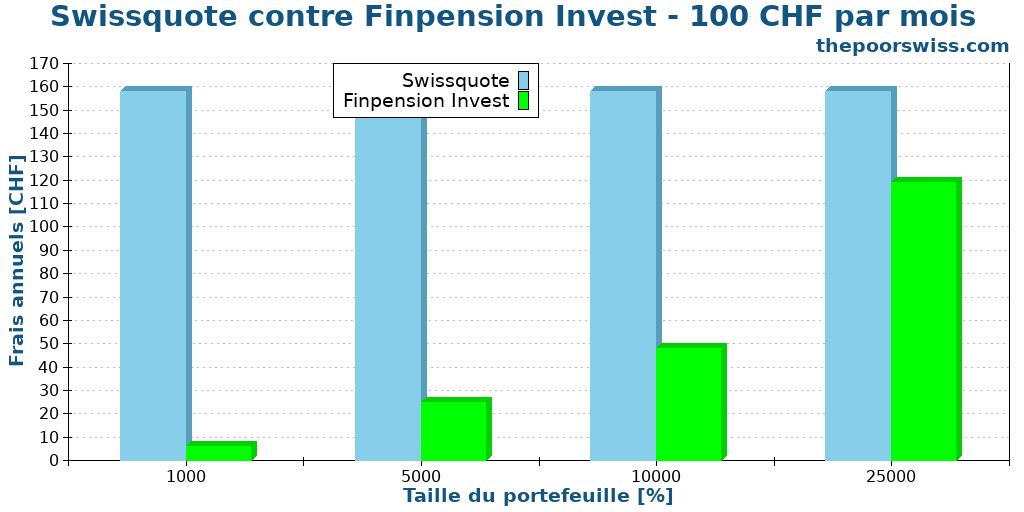

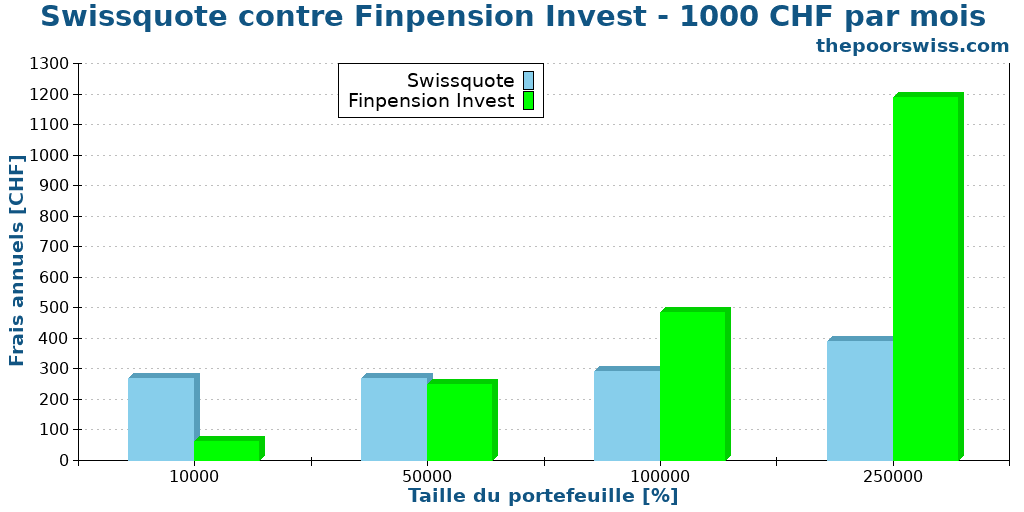

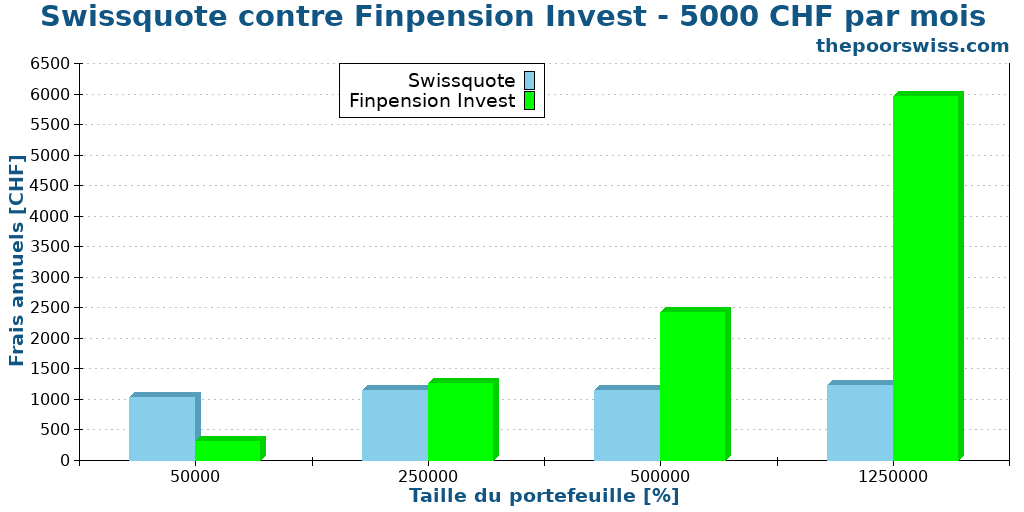

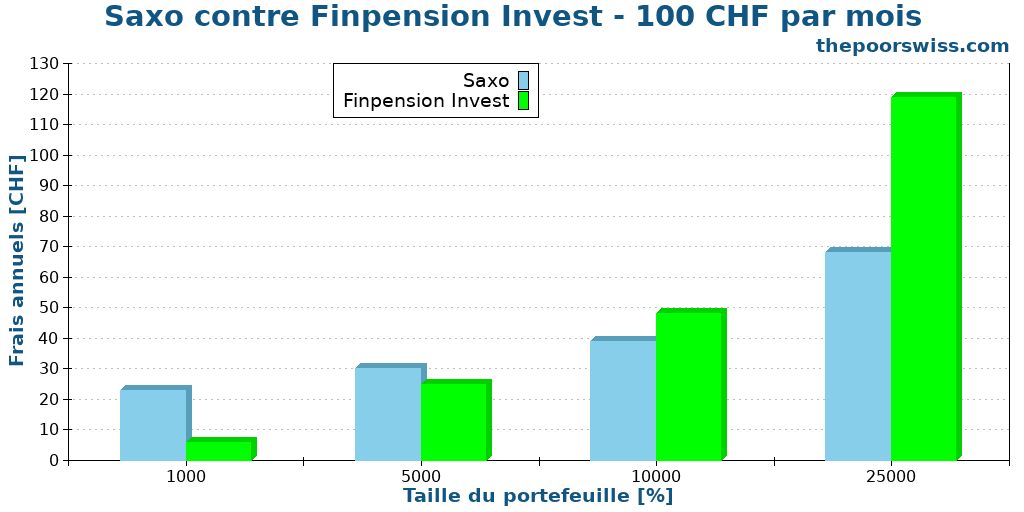

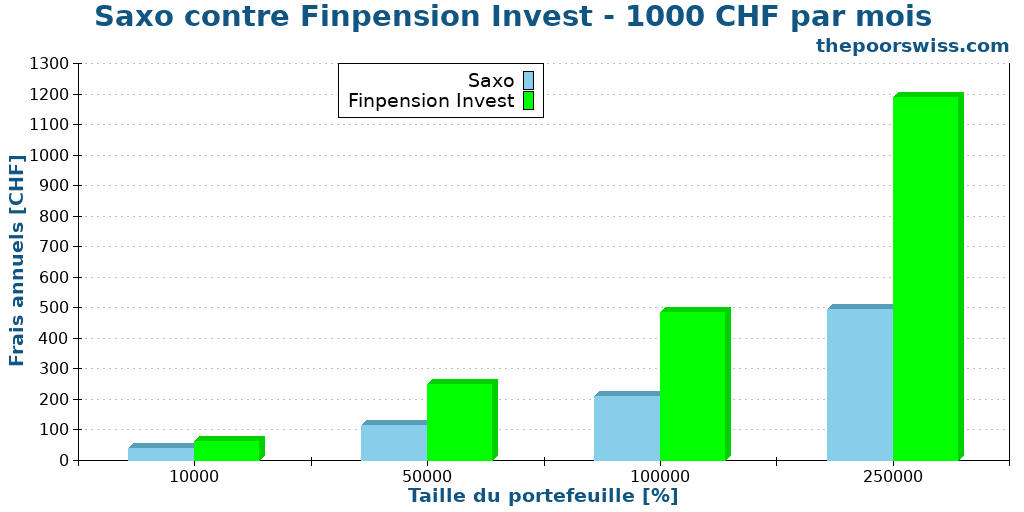

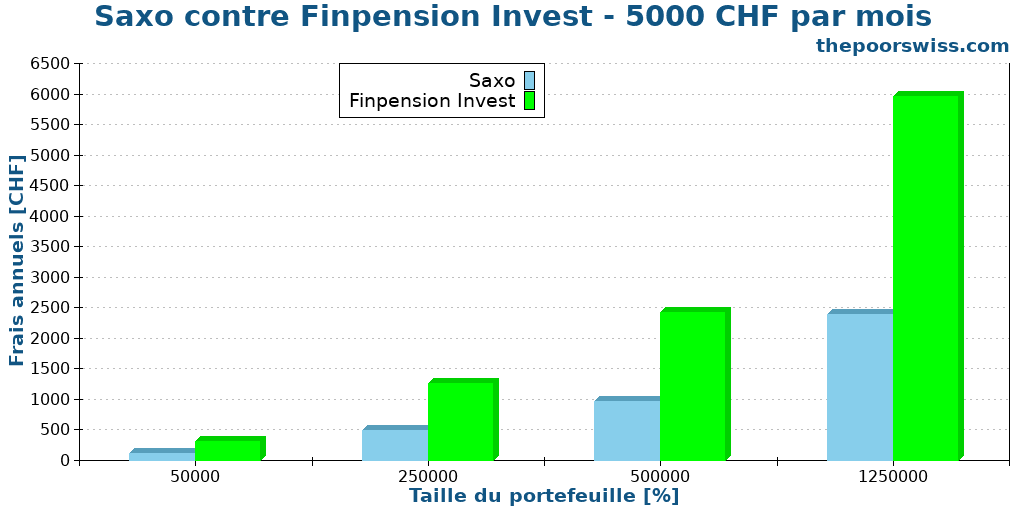

Swissquote vs Finpension Invest

Un excellent Robo-advisor, optimisé au maximum, par Finpension.

Finally, we can also compare Swissquote with Finpension Invest. Finpension Invest is the most efficient Swiss robo-advisor. It has extremely low fees, and at this point, it is the only robo-advisor that allows you to reclaim US dividend withholding. Therefore, it does not have any withholding disadvantage compared to Swissquote. With both, we will need to pay Swiss stamp duty.

Enfin, notre робо-conseiller parvient à être moins cher que Swissquote à chaque taille de portefeuille. Pour un petit investissement mensuel, Finpension Invest est très efficace grâce à ses faibles frais de garde.

Une fois que nous augmentons l’investissement mensuel et la taille du portefeuille, Finpension Invest reste assez compétitif, jusqu’à 100 000 CHF. Par la suite, les frais de garde commenceront à peser lourdement.

With a very high monthly investment, the results are quite interesting. Even at 250,000 CHF of portfolio, Finpension Invest manages to be on the same level as Swissquote. But then, it has the same fate as other robo-advisors. In the worst case, it would be costing 3900 CHF more than Swissquote.

Finpension Invest is significantly cheaper than the other robo-advisors we have seen. However, with a considerable portfolio, the custody fees will still cost more than Swissquote. But I am positively surprised at how it can compete with Swissquote. This is an excellent example of how a robo-advisor can be cheaper than brokers.

Saxo vs robo-advisors

Investissez avec un courtier Suisse avec des prix très bas. Commencez à investir avec Saxo et recevez 200 CHF en crédits de transactions.

- Bons frais de conversions

- Courtier Suisse

Saxo is not a new broker, but they only became affordable in 2024. Most of their brokerage fees are very affordable, especially for currency exchanges.

I will note that Saxo has access to US ETFs. And since it is Swiss, you will pay Swiss stamp duty on the operations.

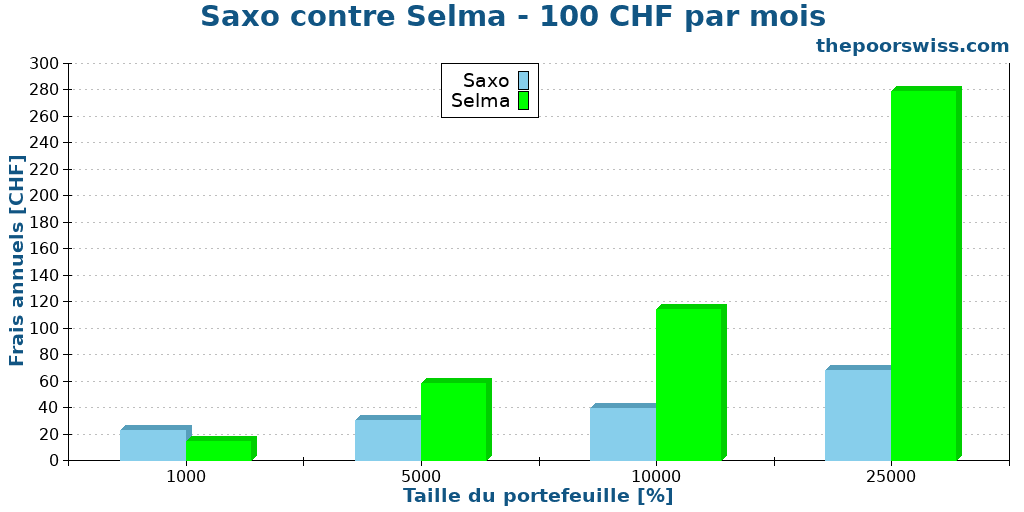

Saxo vs Selma

We will start comparing Saxo and Selma now. They both incur Swiss stamp duty. Saxo has the advantage of having access to US ETFs and having no custody fees.

Saxo is cheaper than Swissquote for transaction fees, so Selma has a hard time comparing with it. Even at a 5000 CHF portfolio, Selma is already more expensive than Saxo. And the difference grows with a higher portfolio.

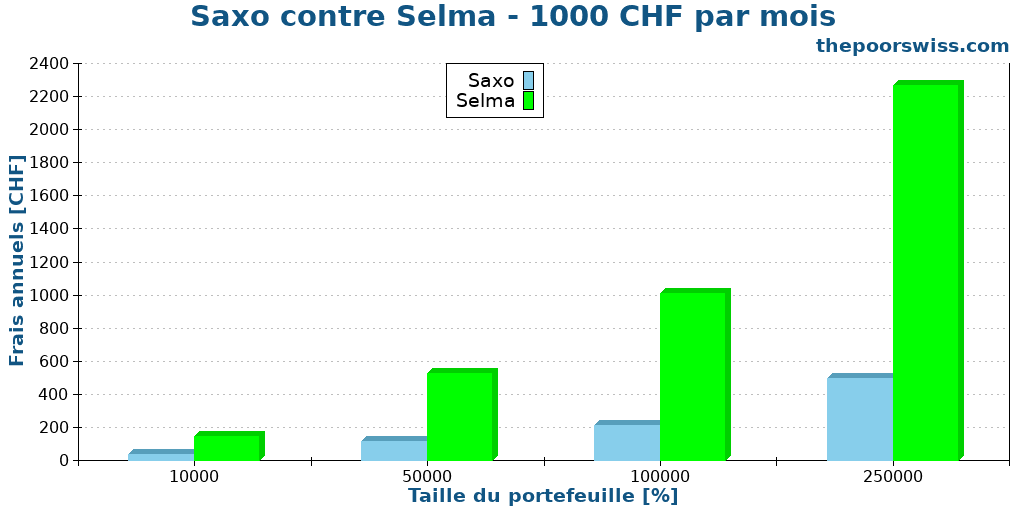

We can see what happens with a higher monthly investment.

In this case, Saxo is always cheaper than Selma. The low transaction fees of Saxo make it compare really well. And as the portfolio grows, the custody fees of Selma start to add up quickly.

Finally, we can increase again the monthly investment.

Again, Selma is always much more expensive than Saxo. The differences at high portfolios are higher than they were with Swissquote since Saxo has significantly lower fees. In the worst case, Selma is 8000 CHF pricier than Saxo.

Overall, Selma does not compare well with Saxo. Saxo is almost always cheaper than Selma. Saxo has low transaction and currency conversion fees. With massive portfolios, the lack of US ETFs for Selma makes it difficult for it to play on the same level.

Saxo vs True Wealth

We now compare Saxo and True Wealth. Both have to pay Swiss stamp duties, and True Wealth lacks US ETFs.

We can start again with 100 CHF per month.

Même avec de petits portefeuilles, True Wealth a du mal à rivaliser avec Saxo, qui a des frais très bas.

Lorsque nous utilisons un investissement mensuel plus élevé, True Wealth devient rapidement plus cher que Saxo. Le poids des frais de garde commence à augmenter à mesure que la taille du portefeuille augmente. À 250 000 CHF, True Wealth est déjà cinq fois plus cher que Saxo.

At the smallest portfolio level, True Wealth can still compare to Saxo. However, as the portfolio grows, so does the gap between the broker and the robo-advisor. In the worst case, we would pay 6200 CHF more with True Wealth than with Saxo.

Overall, True Wealth can meet the prices of Saxo with small portfolios. But the difference is not that significant. Indeed, robo-advisors are usually cheaper at low portfolios because we pay lower custody fees than transaction fees. But since Saxo has lower transaction fees, it makes it difficult for a robo-advisor to compete. And finally, once the portfolio grows large, the custody fees dwarf the transaction fees, and the difference is exacerbated by the lack of US ETFs for True Wealth.

Saxo vs Finpension Invest

We can now compare Saxo and Finpension Invest. They are both efficient for US dividends. Both services will have Swiss stamp duties.

Finpension Invest parvient à battre Saxo sur seulement les deux plus petites tailles de portefeuille. Les frais de garde de Finpension Invest sont vraiment bas, mais comme Saxo n’a pas de frais de garde, il est difficile de les battre.

Une fois que nous augmentons l’investissement mensuel, les différences entre les deux services diminuent. Finpension Invest ne parvient plus à battre Saxo pour les deux plus petits portefeuilles.

Even on the highest portfolio size, the difference is not as significant as I expected. In the worst case, Saxo is 3600 CHF cheaper than Finpension.

Overall, Finpension Invest, as the cheapest Swiss robo-advisor, can sometimes be a little cheaper than Saxo. However, as the portfolio grows, the advantage goes to Saxo.

Interactive Brokers vs robo-advisors

Le courtier dont vous avez besoin pour acheter des actions et ETFs avec des frais incroyablement bas! Investissez dans des compagnies américaines dès 0.50 USD!

- Très bon marché

- Exécution sans faute

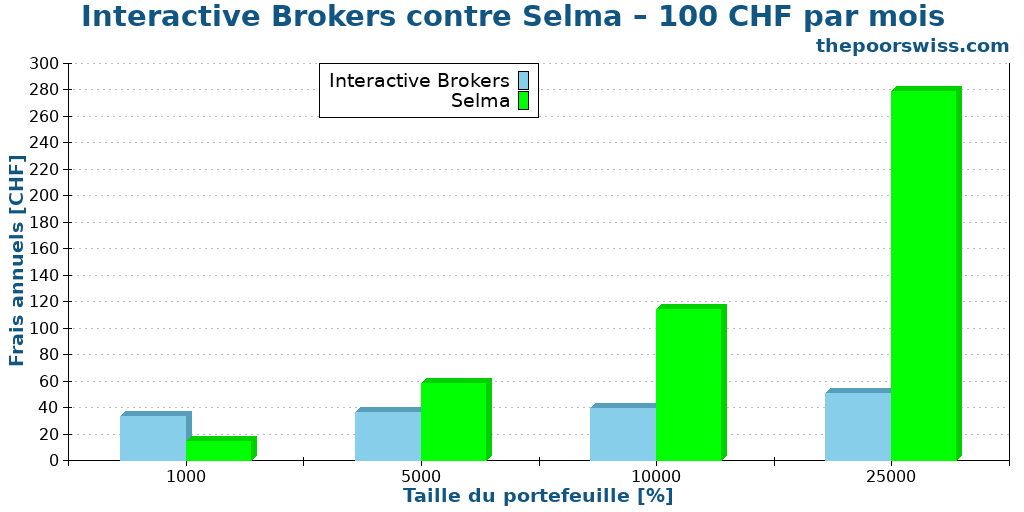

Finally, we will pit Interactive Brokers (IB) against robo-advisors. Interactive Brokers is my favorite broker for Swiss investors and the broker I use. It is a broker from the US.

Interactive Brokers has access to US ETFs. Since it is a foreign broker, Swiss stamp tax is not due, so we can save money here.

Some people may think that this is not a fair comparison, since they do not obey the same regulations. However, there are many foreign brokers available to Swiss investors. It would be inefficient to not use them if they are better (and they are) than Swiss brokers. Furthermore, I currently do not know any foreign robo-advisor. If that changes, I will definitely include a foreign robo-advisor to see how it compares.

Interactive Brokers vs Selma

We can start by comparing Interactive Brokers and Selma. IB has US ETFs and no Swiss stamp duty. Selma has no US ETFs and has to pay Swiss stamp duty.

Ce n’est qu’au niveau d’un portefeuille de 1000 CHF que Selma pourrait se comparer à IB. Par la suite, les différences deviennent considérables. Dans le pire des cas ici, Selma est déjà 5 fois plus cher qu’Interactive Brokers.

Si nous augmentons l’investissement mensuel, les différences deviennent très importantes. Dans le pire des cas, Selma est un ordre de grandeur plus cher qu’IB. Cela fera une énorme différence sur les rendements finaux.

At the final level of investment, the differences are all about 10 times cheaper for IB. In the worst case, you would save 9700 CHF by using IB rather than Selma.

Selma cannot compete with Interactive Brokers. The Swiss stamp duties, the high custody fees, and the lack of US ETFs really play against Selma.

Interactive Brokers vs True Wealth

We can redo the same comparison but with True Wealth, which is slightly cheaper than Selma in most cases.

Même s’il est légèrement meilleur, il ne peut pas non plus se comparer à Interactive Brokers. Le pire des scénarios est déjà quatre fois plus cher.

Avec un investissement mensuel de 1000 CHF, même le plus petit portefeuille coûte plus cher à détenir chez True Wealth qu’avec Interactive Brokers.

On the highest level of investment, IB is between 9 and 10 times cheaper than True Wealth. In the worst case, you would lose 7900 CHF per year using True Wealth.

Again, True Wealth cannot compare with Interactive Brokers.

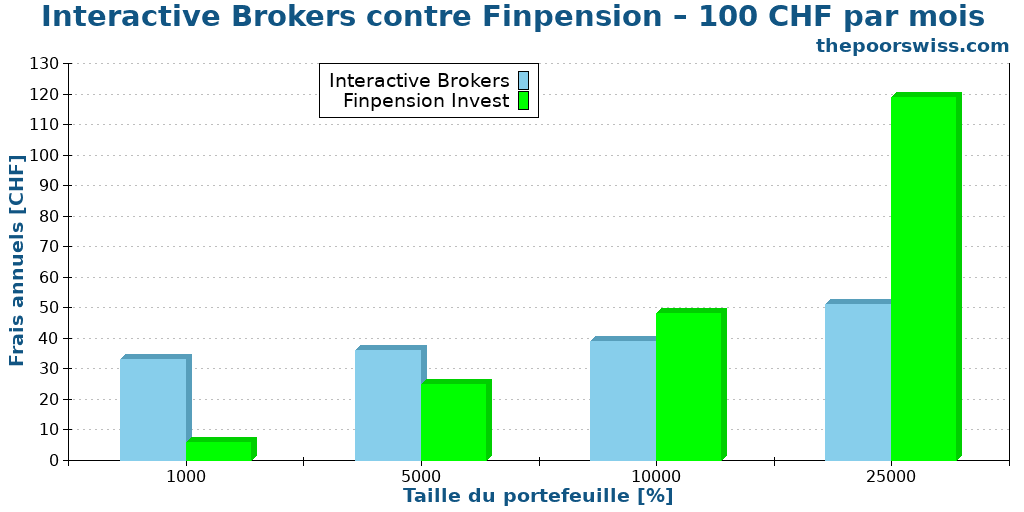

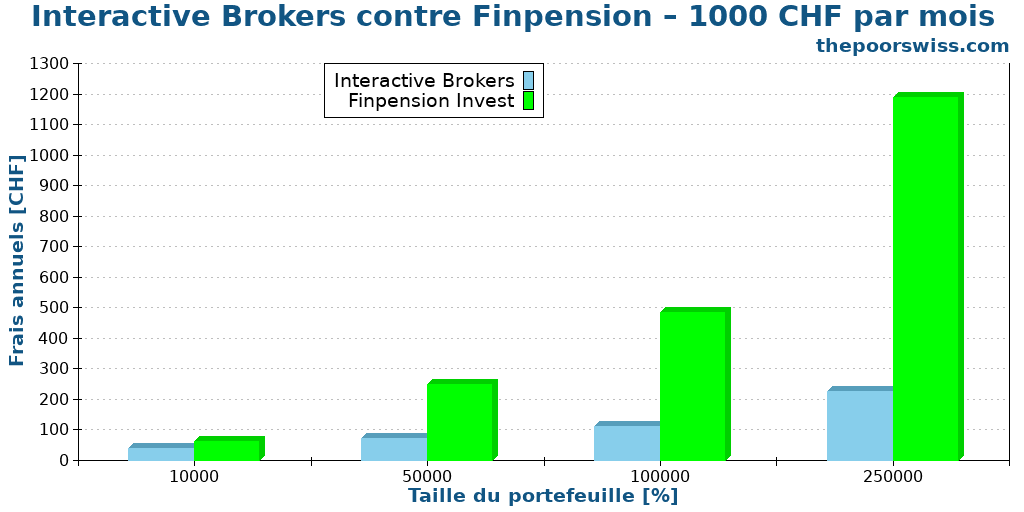

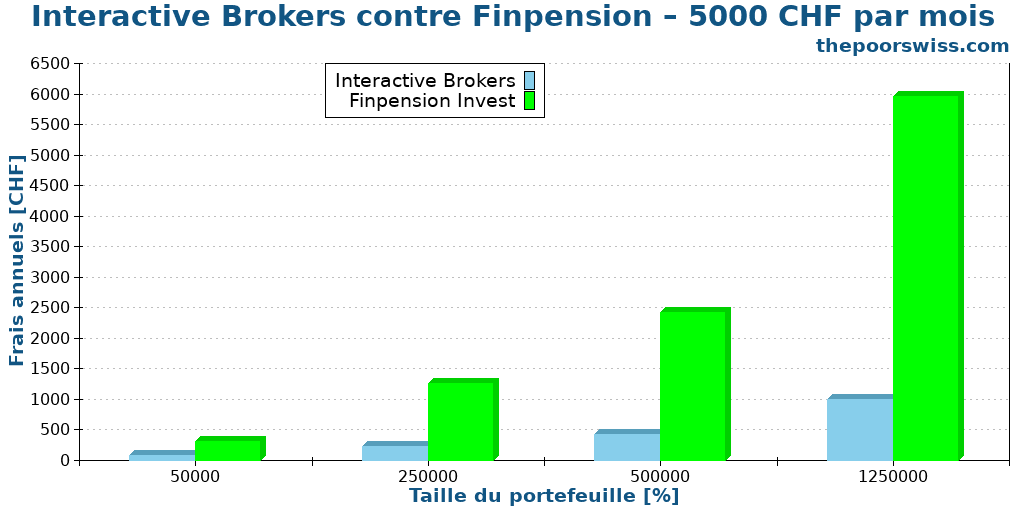

Interactive Brokers vs Finpension Invest

Finally, we can compare our best broker with our best robo-advisor, Finpension Invest.

Finpension Invest fait légèrement mieux que nos deux précédents candidats contre Interactive Brokers. Cependant, il ne parvient à bien se comparer que pour le plus petit portefeuille. Ensuite, les frais de Finpension Invest augmentent beaucoup plus rapidement que ceux d’Interactive Brokers.

Une fois que nous augmentons l’investissement mensuel, même Finpension Invest a du mal contre Interactive Brokers. Dans le pire des cas, les frais seraient déjà 1000 CHF plus élevés.

The same conclusion stands for the highest level of investment. Even though Finpension Invest is more efficient than other robo-advisors, it cannot compare with Interactive Brokers. In the worst case, you would still pay 5000 CHF more per year at Finpension Invest.

Overall, Finpension Invest is significantly more expensive than Interactive Brokers. At small levels of investments and portfolio sizes, it does a good job, but then it becomes significantly more expensive. We saw that Finpension Invest could be cheaper than brokers before, but that seems to be only the case for Swiss brokers.

Are robo-advisors cheaper than brokers?

We can try to summarize the results to answer the question of this article: Can robo-advisors be cheaper than brokers?

Yes. As we have seen in this article, there are many cases where robo-advisors can be cheaper than brokers. Before doing the computations, I was not expecting that many cases where this would be the case.

Of course, robo-advisors are not always cheaper than brokers. In fact, they have the potential of being much more expensive than brokers. The main reason for these differences is custody fees. Indeed, robo-advisors have custody fees without a maximum (all good brokers have maximums). So, as your portfolio increases, your custody fees increase significantly. With a broker, only the fees of the ETFs increase after some point.

So, when you have a small portfolio, you have an advantage because you will pay low fees with a robo-advisor. On the other hand, a broker will be based mostly on transaction fees, which can be expensive.

The second difference is about tax efficiency. Currently, I only know one robo-advisor that can be tax-efficient regarding US dividends. This can weigh heavily on the total costs.

Finally, when we add a foreign broker to the mix, Swiss robo-advisors cannot be cheaper than brokers. As we have seen in these results, no robo-advisor comes really close to Interactive Brokers once the portfolio grows beyond a certain level.

So, yes, robo-advisors can be cheaper than brokers, but only for small to medium portfolio sizes. And there are significant differences between robo-advisors and brokers.

Conclusion

In this article, I compared the total fees of robo-advisors against brokers. And there are some interesting results.

When we compare Swiss brokers against Swiss robo-advisors, we can see that robo-advisors can be cheaper than brokers. If you are investing small amounts each month and are not targeting a large portfolio size, robo-advisors can be cheaper than brokers, and the difference can be quite significant. The best robo-advisor can even be competitive at relatively high portfolio levels. For instance, I am quite surprised by how well Finpension can be cheaper than brokers.

However, when we compare our Swiss robo-advisors against foreign brokers, the comparison falls short. Robo-advisors simply cannot compare with Interactive Brokers. The differences are very significant.

If these comparisons interest you, I was thinking of writing an online calculator to compare these scenarios with multiple brokers. Please let me know in the comments below if you are interested.

These results should not discourage you from using robo-advisors because they are not cheaper than brokers. In practice, not everybody wants to or can invest by themselves in ETFs. In these cases, robo-advisors are perfectly fine as long as you are aware of the differences.

If you want to run more scenarios, you can use our comparison tools:

In these comparisons, I have focused solely on the costs to see if robo-advisors can be cheaper than brokers. But the choice also boils down to the level of control between brokers and robo-advisors.

What do you think about these results?

Prochains articles

Cornèrtrader Review 2026 – Courtier suisse bon marché

Cornèrtrader, un courtier suisse très abordable : quelle est sa valeur réelle ? Est-il vraiment abordable ? Nous le découvrirons !

Relevés fiscaux électroniques maintenant disponibles pour Interactive Brokers

Grâce à Datalevel AG, les relevés fiscaux électroniques sont désormais disponibles pour Interactive Brokers, éliminant ainsi l'un de ses rares inconvénients par rapport aux courtiers suisses.

Guide étape par étape : Comment acheter facilement un ETF sur Interactive Brokers

Étapes détaillées sur la façon d'acheter un ETF à partir de la gestion de compte d'Interactive Brokers. Apprenez comment transférer de l'argent, échanger des devises et acheter des parts de FNB.

Apprenez des moyens faciles d'optimiser vos finances et d'économiser des milliers de francs en Suisse avec notre e-book exclusif. Découvrez les services financiers les plus rentables adaptés aux résidents avisés et aux expatriés!

Obtenez votre guide suisse d'économies GRATUIT

Bonjour et merci pour cette super comparaison. Un robot comme Finpension offre concrètement quoi par rapport à un courtier comme Néon ? Disons que je veux investir à 100% dans un ETF FTSE World. Je le fais avec les deux. Quel avantage j’ai à part avoir 0.39% de frais avec Finpension ? Parce qu’en soit ils sont aussi simples l’un que l’autre. Merci.

Bonjour Eliot,

Un robot va vous faire un portefeuille assez adapté à votre situation et faire tous les achats et ventes nécessaires pour le maintenir balancé.

Si vous êtes capable de choisir vous-mêmes un ETF et de gérer votre investissement, alors il y a peu d’avantage

Encore une remarque pour le comparatif Swissquote vs Finpension: Swissquote charge des commissions de change indécentes (0.95%) ce qui fait des frais de près de 2% aller-retour…, ce qui revient à environ 15bp p.a. de frais en sus pour le portefeuille type…

Bonjour Christian,

Les frais de change sont pris en compte dans mon analyse.

Par contre, les frais de vente ne le sont pas. Et du coup, vous avez raison qu’à la vente, on aura encore des frais supplémentaires.

Merci Baptiste pour toutes ces études toujours aussi intéressantes.

Quelques remarques:

IAB et les ETFs US sont clairement imbattables, au prix toutefois de démêlés avec le fisc US (estate tax) pour la descendance

L’étude porte sur un portefeuille comportant une seule classe d’actifs, ce qui est à mon sens non-représentatif pour des tailles de portefeuilles plus importants

Le robot advisor (ou rule based investment) permet de profiter de rebalancements automatiques permettant de « cliquer » les gains. Le faire soit même requiert de la discipline + occasionne des coûts

Tes remarques sont tout à fait correctes. J’ai pris un seul portefeuille parce que sinon cet article serait beaucoup trop long. Et les résultats ne changeraient pas vraiment.

Le but n’est pas de montrer que les robo-advisors sont mauvais. Le but est de montrer la différence en terme de coût. La décision d’utiliser un robot-conseiller au lieu d’apprendre à investir soi-même se doit de prendre en compte les coûts.