N26 in Switzerland Review 2026 – Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Everybody will agree that paying 1.5% of fees, or even more, on each transaction abroad really sucks! Unfortunately, this generally happens when you are on vacation or shopping online in other countries. Thanks to N26, this should never be necessary anymore!

N26 is a digital bank offering transfers in other currencies for free! Not only that. But the entire bank account is free! And they are a bank! European regulations will protect the money you have on N26. You can even withdraw cash for free several times a month! That sounds great!

In this review, I cover everything you need to know about N26. Since I have already discussed Revolut on this blog, I will compare both services, which are similar but not equivalent!

Stay tuned to find out how to save money on foreign exchange fees!

| Monthly fee | 0 CHF |

|---|---|

| Users | 8’000’000 |

| Card | Mastercard Debit |

| Currencies | EUR, GBP, USD |

| Currency exchange fee | Free |

| Top-up CHF | Not possible directly |

| Languages | English, French, German, and Italian |

| Other features | N/A |

| Depositor protection | 20’000 EUR |

| Established | 2016 |

| Headquarters | Germany |

N26

N26 is a digital bank that was founded in Germany in 2016. For a short period, it was called Number 26. Its headquarters are in Berlin, Germany.

They first started as a simple interface in front of another bank. But they soon got a German Banking License. De facto, they are now a bank in all of Europe. They got a Full Banking License. They have the same rights as any other bank in Europe.

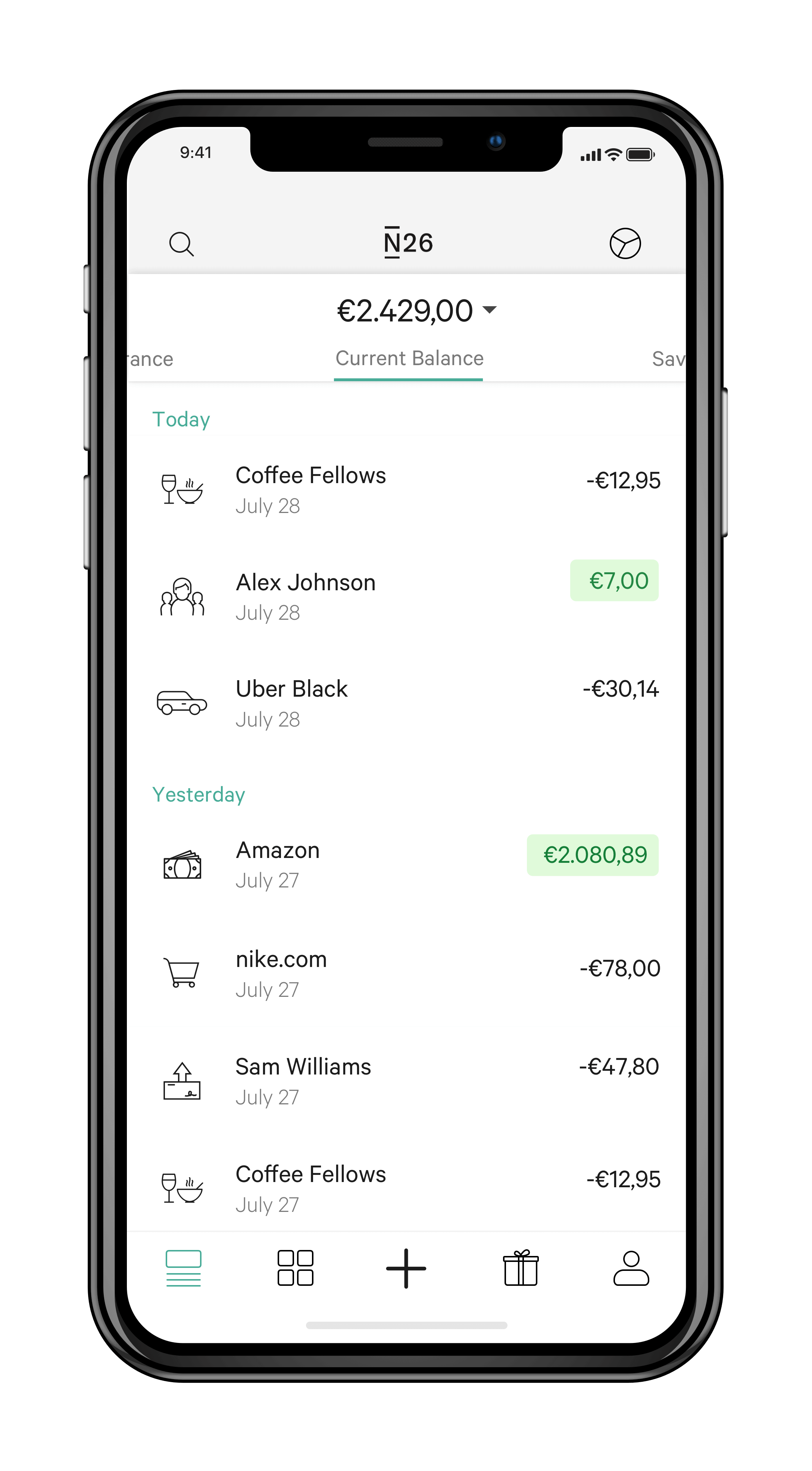

Since N26 is a digital bank, you must access it through your phone or computer. They do not have bank offices where you can do transactions. It is the main reason they can cut costs.

You can receive payments directly into your account using your personal EUR IBAN and make your payments from your account. Also, if you know people using N26, you can send them money directly!

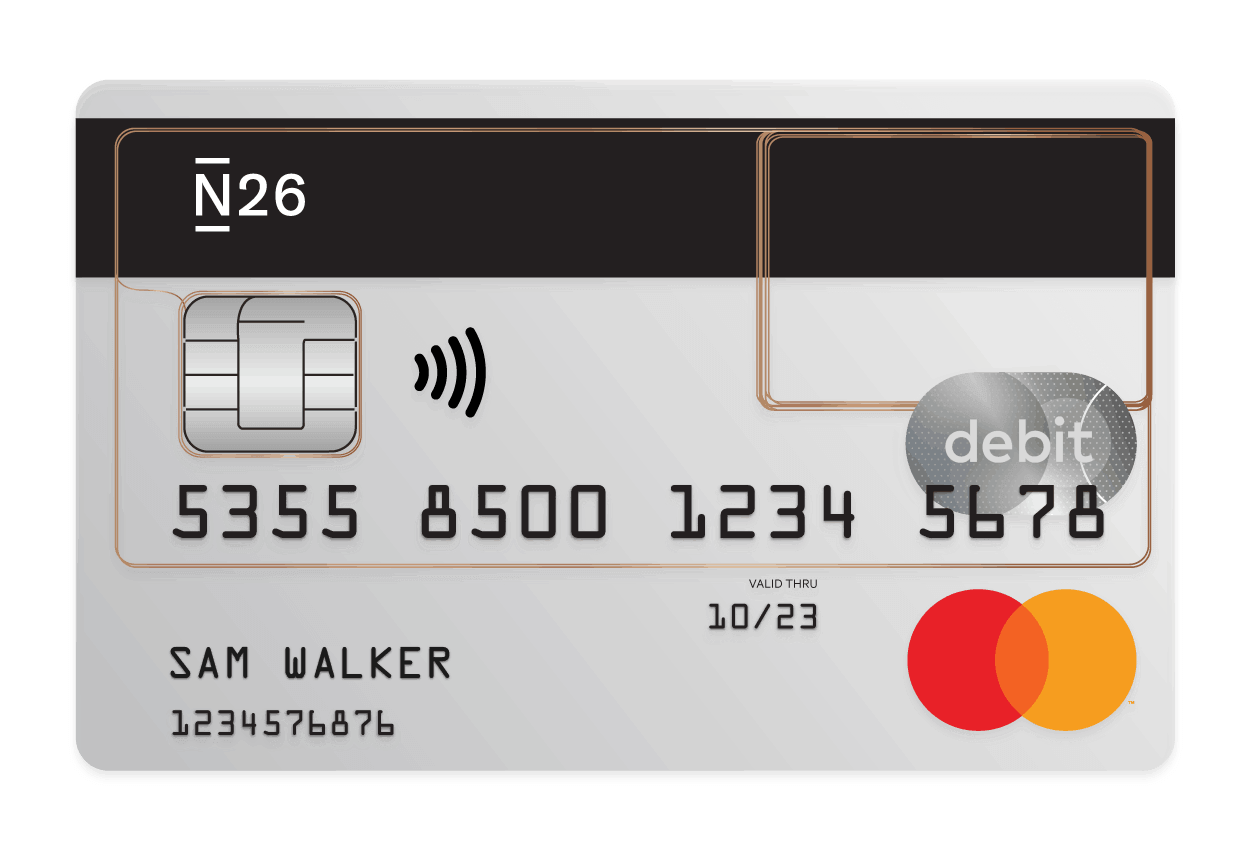

With your account, you will also receive a Mastercard Debit Card. You will be able to use it to make payments in foreign currencies for free as well! You can also use it to make free withdrawals in EUR.

Now, with this Mastercard lies the most significant caveat of N26. They do not offer any cashback on transactions!

While this card is perfect for payments in foreign currencies, you should not use it for payments in your home currency. It means you should still have a credit card with some cashback next to this one. It should be part of your credit card strategy.

N26 Fees

The most exciting thing about N26 is its very low fees! But first, we have to talk about the three different accounts that are available:

- N26: This is the standard account for most users. It is entirely free! You get some free withdrawals in EUR and all currency conversions for free!

- N26 Black: This option is in addition to the standard account and costs 9.90 EUR per month. You will also get free withdrawals abroad, which is excellent! In addition to the base features, you will also get protection from Allianz Insurance when you travel. It is useful if you travel a lot.

- N26 Metal: This is the high-end option for 16.90 EUR per month. You will get all the advantages of Black, plus dedicated customer support and exclusive partner offers. For instance, you can get 10% off on some hotels.

The only service I would need would be the basic free option. For me, 9.90 EUR monthly for a bank account is already too much. I do not see the point of the Black and Metal cards for me. So, we will discuss the fees for the standard account here.

N26 also has a business plan. But this is not something that we should be concerned about. It is a plan for self-employed people and freelancers. You may want to look at it in more detail if you are a freelancer.

With the standard account, you can make five free withdrawals in euros per month. After that, you must pay 2 EUR for each extra withdrawal. You can also withdraw euros abroad for free. However, if you withdraw cash in other currencies, you will pay a 1.7% fee!

On the other hand, payments in currencies other than EUR are free! You will not be charged if you transfer money from EUR to GBP. And the current exchange rate will be used. It is excellent, and this is the main reason I would use N26.

N26 in Switzerland

Since September 2019, N26 has been available in Switzerland. It means you can use all services of the N26 service if you are a Swiss customer. It completes the already long list of countries supported by N26. It means that N26 has excellent coverage of Europe.

However, there are some strong limitations. First, they do not offer you a Swiss IBAN, and you cannot transfer money directly from your Swiss bank account without fees.

So, you will have to transfer EUR to your N26 account. It means you will have to pay fees to top up your account. It is a significant disadvantage.

However, if you have a bank account in euros, you can transfer money to your N26 account for free. And if you get paid in EUR, you can also receive your salary directly in your N26 account.

Another issue is that they have no support for CHF. It means you cannot use your card in Switzerland without currency conversion fees. It is a pretty big limiting factor. However, since this is not the primary use for this card, you can still use it for your foreign transactions. You should not use a card like N26 or Revolut in Switzerland. It is where you should use your local credit card with some cashback.

On the plus side, they offer a personal EUR IBAN. Such an account can be pretty useful in Europe. And, of course, all the services I have discussed before are available in Switzerland.

For now, I do not think N26 is a good fit for me as a bank account. Since I get paid in CHF and most things in Swiss francs, I need an excellent CHF bank account. As for a travel card, I need an IBAN to transfer money for free to the account.

However, N26 is still a very interesting option as a travel credit card. People can still use it for free currency exchanges. And I am keeping up with this offer to see where it goes. Once we have a free way to top it up from a Swiss account, I will start using it.

Alternatives

We should compare each financial service with some alternatives. Since they are very similar, we should compare N26 and Revolut.

N26 vs. Revolut

The main competitor of N26 is Revolut. We have already talked in detail about Revolut. They both offer similar products, but there are some significant differences.

The most significant differences between these two services stem from the fact that N26 is entirely a bank. On the other hand, Revolut is not yet a bank.

In 2019, Revolut got a European Specialized Bank License. However, they did not yet implement anything with that. Moreover, N26 got a Full Banking License, while Revolut only got a Specialized Banking License. The difference is that Revolut cannot offer any investment services to its customers. On the other hand, N26 is free to do so. N26 got a banking license from Germany and Revolut from Lithuania.

Being a bank makes a great advantage for N26. One great thing about N26 is that your money is insured according to German law. If N26 goes bankrupt, the government ensures 100’000 euros. On the contrary, there is no guarantee for your money on Revolut! Once Revolut becomes a bank, money on Revolut would also be insured under the same conditions. But they have not announced any information about having a real bank account.

Also, the fee system of N26 is much simpler than Revolut. Everything is free! With Revolut, some currencies have higher fees. And during the weekend, fees are higher as well. It is a bit complicated to keep track of.

A small advantage of N26 is that they will deliver your card for free. With Revolut, you will have to pay 6 EUR for that service.

Both services will be reachable directly from your phone and on the web. I think this is an excellent feature for people who dislike their phones.

A slight advantage of Revolut is that you can withdraw 200 EUR for free abroad. It is not much, but this can help. N26 will charge you 1.7% for this. After the first free 200 EUR, you must pay 2% at Revolut. So, it is a bit more expensive than N26 if you withdraw more than 200 EUR a month.

The most significant advantage of Revolut over N26 is that they have much better support in Switzerland. Revolut is relatively better in its accessibility, supporting many more countries. But new countries have been announced for N26. So we will have to wait and see!

Neither company has an excellent reputation. However, N26 has a better reputation than Revolut. There have been fewer concerns about N26, even though some of their actions seem debatable.

N26 may improve its support in Switzerland. For me, a Swiss IBAN would be necessary before I use N26.

If you want more details, read my comparison of N26 vs Revolut.

Controversy

There has been quite some controversy about N26 over the years.

In 2016, there was a lot of talk about N26. First, many accounts have been terminated, and some customers could not do anything about that (Source). The reason was that they were making too many withdrawals. Since that point, the company has changed its policy on ATM withdrawals. They added a maximum of five free ATM withdrawals at this time.

Later that same year, researchers found several vulnerability issues within N26 (Source). An attacker could use these vulnerabilities to access accounts from the users. Since then, they have fixed these issues, and apparently, no account has been compromised.

However, there was also some more recent controversy about N26. In 2019, many users had issues contacting the bank after their credentials were stolen! It took up to two weeks for certain people to regain access to their accounts.

And in April 2019, German Bank Regulators ordered N26 to change its process to avoid money laundering. They did not make enough effort for that before. And they have been too slow to close money laundering accounts. Since then, they have acknowledged this and started to take action.

I think every banking startup has seen some controversy since its inception. I would not worry about it too much unless I stored much money in the account. I never had more than 1000 EUR on my Revolut account, and I would not want to keep more than 1000 EUR on N26. And given that money on N26 is insured, this should help.

N26 FAQ

Is N26 well supported in Switzerland?

No, they do not provide a CH IBAN and have no support for CHF.

Who is N26 good for?

N26 is good for people that have EUR available to send to this account and want to use it abroad.

Who is N26 not good for?

N26 is not great for Swiss residents since they do not offer a free way to send CHF to the account.

N26 Summary

N26 offers a free Euro bank account, with very low-fees foreign currency exchanges!

Product Brand: N26

3

N26 Pros

Let's summarize the main advantages of N26:

- Some free withdrawals in Europe;

- Free currency conversions;

- Personal EUR account;

- Cash in the account is insured;

- Well regulated bank account;

N26 Cons

Let's summarize the main disadvantages of N26:

- No CH IBAN means you cannot top it up for free from Switzerland;

- No support of CHF means you cannot use it for free in Switzerland;

- Some controversy in the past;

Conclusion

Overall, I think that N26 is a good product! It can save you a ton of money on foreign exchange transactions. It is good for when you are traveling and buying things online in other currencies. Compared to most standard banks that charge from 1.5% to 2.5% fees on these transactions.

It not only provides a great travel card but also an excellent free bank account. It is an official bank, and your money will be insured for up to 100,000 EUR!

Now, while it is an excellent bank account and travel card, you should not use its credit card too much in your currency. You should opt for a credit card that gives you some cash back! If you do not know where to start, read about my credit card strategy.

Overall, I think that N26 is better than Revolut. I am impressed by the fees. For instance, there is no such thing as weekend fees. There is no limit, and foreign transactions are no longer free. It is much simpler. I have not yet compared their mobile applications. But for my little usage, I do not think it matters much.

However, it still needs a few more features in Switzerland. Before it gets a real CH IBAN, I do not plan to use it. However, once it does, it will become very competitive with services such as Revolut and Wise.

What about you? What do you think of N26? Are you waiting for its arrival?

More reading

Everon Review 2026 – Pros & Cons

Everon is a Swiss digital private bank, trying to open private banking to more people. If you want a private bank, should you use Everon?

Revolut Review in Switzerland 2026: Pros & Cons

Revolut is a digital bank account with a physical card that you can use to pay abroad without fees. Should you use Revolut? We will find out!

What is the Best Swiss Bank in 2026?

Choose the right bank. We compare the best Swiss banks for 2026, looking at fees, interest rates, and digital features for every type of user.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello, i was looking for the cheapest way to get some cash in euro currency. I see that N26 has either 3 or 5 withdraw for free then 2€ each. But i found this on the N26 switzerland website…

« Withdrawals in Switzerland in euros are free

Withdrawals in Switzerland in Swiss Francs are subject to 1,7 % foreign exchange fees

Withdrawals in the Eurozone in euros are free 5 times per month according to our Fair Use Policy. »

How can we understand this? Are they always free in switzerland or 3-5 times as for the eurozone?

Thanks for this great website 👍🏼

Hi Lemon,

The way I understand is this way:

* In Switzerland, all withdrawals in Euros are free

* In Switzerland, all withdrawals in CHF cost 1.7% fee

* In the rest of the Eurozone (but not Switzeralnd), you can withdraw 5 times per month in Euros for free.

Does that make sense?

“Another issue is that they have no support for CHF. It means you will not be able to use your card in Switzerland.”

This is not correct. You are able to use your card in Switzerland, but there will just be currency conversion EUR>CHF. On top of that, you are able to use your card at any place and in any country where MasterCard/Maestro is accepted.

Hi Miros,

I still believe it is correct. You will be able to use it in Switzerland but it will be so expensive that it is just dumb to use it in Switzerland.

Thanks for stopping by.

Hi,

Here is a little thing to do to avoid SEPA fees to put money on your N26 account. Just hold a Revolut AND a N26 account.

You can then transfer CHF from your swiss account to Revolut with no fees and then transfer from Revolut € balance to N26 without any fees either.

Just make sure you also use a bit your Revolut account and do not just transfer “blindly” the amount received on Revolut straight to N26 as it might be seen as money laundering.

Hi Gilles,

Yes, that is a good technique to transfer money for free. But if you already have a Revolut account, there are few advantages of also having a N26 account. The biggest advantage is to have money insured. Having so many accounts, in the end, makes it quite complicated.

Now, are you use about the money laundering part? This is the same as moving money between several of your accounts. I do not think this would qualify as money laundering. This is the same we used to do with TransferWise to transfer money for free to Revolut before the had a Swiss IBAN.

Thanks for stopping by!

Hi,

this is true that it is a bit complicated and I would not do this JUST for € account.

But I mainly use Revolut for other balances, like GBP or USD but I still prefer N26 for my € account.

For the balance insurance at first and I also prefer their app and Support, also the fact they have a Web interface. But these are more personal preferences than real points about the product itself.

It is also good to have a real and personal IBAN in € in order to manage crypto operations on trading plateforms.

Hi again Gilles,

Yes, having a personal IBAN in EUR can be a really convenient thing! I guess for some people it’s enough to get Revolut + N26.

I would think indeed that this comes from the “fair use” system of Revolut. Maybe it even comes from their money-laundering prevention system. But I do not think this would qualify as money laundering in front of the law. But if your money gets blocked, it is extremely inconvenient indeed!

Thanks for sharing :)

Oh and about that laundering thing, I don’t know if it would be considered as real money laundering, but there are quite a few cases where people got there Revolut access blocked for sometimes many weeks because they were just transferring money to Revolut and transferring it out straight away, even on the same holder’s name.

Maybe a matter of internal “fair use” policy of Revolut though… not sure.

What are your thoughts on N26 Business account?

I reckon combining Revolut with N26 Business (charging in Revolut and send Euro to your N26 Euro account) would bring some synergies for following reasons.

1) 0.1% cashback

2) 5 Free withdrawal in Euro Zone

3) Weekend Transactions in currencies where Revolut does not support to hold (No weekend fee with N26)

Hi Simon,

If it’s easy to get the N26 Business account, then, yes, this makes sense.

However, the eligibility requirements include “You will use the account primarily for business purposes.” and “as long as you use the Mastercard for business spending and the Maestro card for personal spending, you can continue to enjoy the many advantages of the account.” For me, this means that you will only get the cashback on the Mastercard and you are not supposed to use it for personal purposes.

And for only 0.1% cashback, it does not feel worth it. The 5 free withdrawal is nice but we almost don’t use cash already. Weekend transactions is a good thing. But I think they can be better avoided by converting the balance in advance.

What do you think?

Thanks a lot for sharing!

Hi,

as you, I don’t think N26 is “ready for swiss” yet. But comparing to revolut, N26 offers two advantages:

– even with the controversys (check revoluts community once in a while, it just doesn’t get reported so often ;) N26 seems more trustworthy than revolut (why getting a bank-license when not using it?)

– N26 offers a real DEBIT card. Revolut only prepaids. With prepaid cards, you always have the risk that it can not be used (eg. when wanting to rent a car, trying to refuel your car (happened to me both in CH and germany!), aso). Debit-Cards have the same acceptance as credit-cards, IF offered by a bank (had issues with the TW-debit, too, while another customer with the N26-card didn’t had any problems…

Also I read about a dkb.de-recommendation:

issue with DKB (or ING or any other “free” german bank): they offer a dispo-credit (if you want it or not, you get one), so you’ll have a credit-check. People with lower (or no) income can’t get an account with them. Especially when having a swiss credit-card (cumulus or supercard plus) AND a bank-account in CH… (applied with DKB, so i found out about this).

ALSO, time for a little update of the article ;-) N26 now also offers Google Pay and Apple Pay in CH, so even with “EUR only”, it’s a better altrnative for swiss users than getting an expensive (but x-Pay supported) prepaid-card (or one of the “real” but expensive credit cards) in Switzerland…

Hi Grenzgänger,

I agree that N26 seems to have a better reputation than Revolut. I would probably still not move too much money to N26 either.

I didn’t know that you could use N26 cards for things like rent a car. That’s good to know. I don’t do that often in EUR, but that could be really useful.

I didn’t know either that DKB was doing a credit check. This is a bit inconvenient. Another thing that is better to do before retirement. Thanks for letting me know.

I learned about Google Pay and Apple Pay support in CH. But I do not use any of these services and I do not think they are really useful. What do you use them for?

Thanks a lot for all this information!

For the card: i had the luck to find out, that the revolut-card, due to its prepaid-nature, can cause issues A LOT. Personally, i was lucky to have my Supercard with me, otherwhise I couldn’t have payed for the fuel at that gas station near the border to CH (they didn’t accept prepaid cards) OR the one automatic gas station in CH (also not accepting prepaid cards)…

As for Google Pay: other than Twitch, it’s very easy to use, and I often do so (thanks to revolut) when possible; one card less i need to cary around, everywhere they accept NFC-payments, you can use Google Pay, too (don’t have an iPhone ;) Thanks to revolut, I don’t even have to worry about currency exchange rates when using it abroad.

But granted: getting the card out of the briefcase and holding it to the scanner might be faster than activating the phones display or unlock (for amounts higher than the “no need to enter pin”-one), depending on your cellphone. But for not wanting to have all the cards with you, it’s great…

That’s really good to know. I never knew that gas stations were refusing prepaid cards. I always use my other credit cards for this. But I would definitely have used it if I needed gas abroad.

I guess it makes sense to use it as NFC indeed. But if you use it in Switzerland, won’t you use on the cashback from an actual credit card?

That’s a great solution for people who like phones. But I really don’t, so I like my cards better than my phone!

Thanks a lot for sharing!

As for Prepaids:

it does depend. Some gas stations do accept them, some don’t; some “automats” (unmanned gas stations) do, some don’t. It’s a lottery.

That’s why I’m disappointed with neon – the maestro was accepted everywhere. With the Prepaid Mastercard, I face the same issues as with revolut. And there’d been the possibility to be the first swiss bank issueing a real debit-mastercard (solving the prepaid-issue, while “no dispo needed”)…

As for GPAY: depends on the cards conditions; as the only card i (was given) can use with google pay is the one from revolut, i don’t have any cashback anyway; but if online-shopping does not exclude you from getting the cashback-option, then you don’t have an issue – a google pay-payment shoes up on the invoice as “online payment”…

Yes, it’s a bit sad that they do not provide a real Maestro.

Thanks for all the details :)

Hi,

I’ve been using N26 for a while and works very well, just some tips..

I used a personal (my sister) address in Europe and I had to give a TIN from the country… already 2 “lies”..

N26 close the account from one day to other without giving you any reason.. just be careful about where you use your card, where are you doing mainly your bank activity, etc… they always return your money but they had booked accounts for months ..

Hi Tino,

Thanks for your review :) That’s awesome.

That’s very good to know. And that’s a bit alarming. At least they return the money. But I would not feel comfortable holding a lot of money on this account knowing that.

Thanks for stopping by :)

Happy N26 user here as well. The app is extremely intuitive and you can manage every aspect of your account from there (temporary block, withdrawal limits, e-commerce access etc.). Bank transfers are also quicker than with regular banks.

I would stick with the basic (free) plan however, since I’ve heard about quite a few issues with the travel insurance coverage provided by the premium plans – you’re not covered unless you have paid for the full travel with the card itself (flight tickets, accomodation etc.)

Hi The Young Investor,

Thanks for your review! It’s very helpful!

Yes, I have also heard a lot of complaints about their travel insurance. If you buy a single thing on the travel with another credit card, they will simply cancel the whole insurance package for this trip. It seems a bit more extreme.

Thanks for stopping by :)

Hello, thanks for the great blog overall. I live in Switzerland and I’m thinking of switching my extremely expensive zkb account for a free one. Would you say N26 compares to Neon? Neon would be my preferred choice at the moment but i was also considering to wait for n26..

Thanks for the help

Hi Trippi,

Yes, as a bank, they are both equivalents. I would not wait for N26. I would use Neon. You can always get an N26 card later on when they become available in Switzerland!

If I had to choose a bank right now, I would use Neon.

Thanks for stopping by :)

DKB.de is instead availabe in Switzerland too!

Hi Mauro,

That’s a good point! I didn’t know people were using DKB in Switzerland. I will have to take a deeper look!

Thanks for letting me know!

I dont think it is possible to have a swiss IBAN with DKB.de . At least I could not read it out from the FAQ. It means you have to send EUR only with sepa to your account, and that is not good = unnecessary costs

That’s a good point! We need a real CH IBAN to transfer money into it!

take a look at transferwise it has iban in CHF and in Eur. In USD is a bit more complicated

Hi Ste,

I used to have Transferwise to transferring money. But now I am only using Revolut because the fees are lower unless you exchange a lot of money :)

Thanks for sharing!

Actually, you can already have N26, you just need to provide a German address, like a delivery address in Konstanz would do it, where they can send your Master card (this is how I did it). After transferring at least 150 EUR you can also ask for an EC card, for free of charge. As n26 is already available in the UK, they use there GBP as a base currency with UK IBAN so I suppose CH will get also a local IBAN and CHF as a default currency.

Hi Andras!

Thanks a lot for the tip!

That’s a nice idea indeed. I am not desperate to get a N26 card yet. But this would be a great way to go to have it.

How is your experience with N26?

Thanks for sharing!

can i deposit swiss franc currency via cash26 in my account?

Since you cannot hold CHF in your N26 account, I would be surprised if you could deposit Swiss Francs.