Health Insurance in Switzerland: The Complete Guide!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

The health insurance system in Switzerland is complicated. And since it is mandatory to have health insurance, it is imperative to understand it correctly. So, I wrote a complete health insurance guide to help you!

In these last few years, health insurance has become very expensive. But many people are paying much more than they ought to. You need to know that there are a few things we can do to pay less! So, we will see how to save money on your health insurance in Switzerland.

In this guide, I cover the details of the health insurance system in Switzerland. I cover mostly the base health insurance in great detail. You must choose wisely, and there are many options. I also cover supplemental health insurance, but it is too varied to be covered in detail.

So, here is the complete Health Insurance Guide! This guide contains all you need to know about health insurance in Switzerland!

The Health Insurance system

We start this health insurance guide by describing the health insurance system. In Switzerland, everyone must have health insurance coverage. It has been the law for many years.

There are two levels of insurance:

- The base insurance is mandatory. It covers standard health costs, such as visits to the doctor and hospital. It is compulsory for everyone, regardless of age. Even babies need health insurance.

- Supplemental insurances are not mandatory. There are many different supplemental insurances available. For instance, private hospital insurance, dental insurance, eye insurance, and so on.

Regardless of the provider, the base insurance is the same. Unfortunately, there are many different providers and many different options. It makes it more complicated than it ought to be. For instance, you can choose between different models and different deductibles. You need to know the differences between these things. We cover all this in detail in this guide.

The supplemental insurances are entirely different from one provider to the other. Even two dental insurance policies can differ from one provider to the other. It makes it very difficult to compare such insurances.

The LAMal law governs the base insurance. You often see this term on medical bills. And many people use the term LAMal to describe base insurance. But you do not need to know the details of this law.

Changing Insurances

You can switch to a new base health insurance provider every year. You must cancel your health insurance by the end of November if you want to change. Your letter must reach them before the end of November. So, you should not send it on the last day of the month.

Being able to change often is good for us since we can optimize costs. But, it is also a curse. Because at the end of the year, you will receive calls from insurance clerks that want you to change insurance. As a rule, you should completely ignore them. They are not doing that for you!

But, you must cancel supplemental insurance up to six months in advance. It makes it so that most people rarely change supplemental insurance.

You must know that an insurance provider cannot refuse your base insurance coverage! An insurance provider cannot refuse someone because it would be too expensive to cover! But they can refuse to cover you for supplemental insurance.

What is covered by the base insurance?

There are many things covered by compulsory base insurance. But, many of these things are subject to conditions that are sometimes complex. So, I cover the basics here.

Here are the main things that are covered.

- Visits to the hospital, interventions, and emergency treatments. However, you still must pay 15 CHF per day in the hospital. This coverage also includes care after serious treatments.

- General treatments by doctors. But many specialist treatments are excluded.

- Prescriptions from the doctor.

- Childbirth expenses and abortions

- Mammograms and colon cancer screenings for people over 50.

- Gynecological examinations

- Glasses and contact lenses for children up to 18. Insurance only covers up to 180 CHF per year.

- Emergency dental care. Dental care coverage is limited to severe issues.

- Psychotherapy under some conditions.

- Most common vaccinations

- Some alternative therapies, such as acupuncture and homeopathy.

However, this is only covered if an accredited specialist does it. And even then, there are some conditions. Therefore, for alternative medicine, it is better to take supplemental insurance.

These are the most important things that the base health insurance covers. If you want to know all the details, I would recommend reading the information from the Federal Office of Public Health.

How is it covered?

First, each insurance has a deductible. All the expenses below the deductible are not covered. For instance, if your deductible is 300 CHF (the smallest), you must pay the first 300 CHF of medical expenses before the insurance covers anything. The deductible will not apply to maternity fees after the third month of maternity.

But even after the deductible, there is still a part that you have to cover. This fee is called the retention fee. For everything that is reimbursed by the insurance, you will have to pay 10% of it. The retention fee is a yearly maximum of 700 CHF for adults and 350 CHF for children. This retention fee does not apply to maternity fees. The retention fee is 20% on medicine you could replace with a lower-cost drug.

Another important thing is who pays the bills. There are two models for that:

- Indirect Claim Settlement (Tiers Garant): Your doctor sends you its bills. You pay all your bills yourself. Then, you send your invoices to the insurance that will reimburse you for what is covered by your policy.

- Direct Claim Settlement (Tiers Payant): Your doctor will send the bills to your insurance. The insurance will pay what is covered. It will then send you an invoice for the deductible or the retention fee.

If you do not think you can handle the upfront fees, you should choose an insurance provider with Direct Claim Settlement. However, if you are in that case, you should improve your financial situation. Also, these insurance providers are generally more expensive.

Hospital fees generally fall in the Direct Claim Settlement regardless of your insurance. Indeed, they can be costly, and your insurance will generally reimburse these fees.

What is not covered?

Accidents are not covered by health insurance but by accident insurance. I will talk about this in more detail below.

Generally, you will need to be treated in your canton. However, if you are injured in another canton, you must be moved to your canton for treatment. That is, of course, if it is possible to move you. Supplemental insurance can cover treatments in other cantons.

Health insurance abroad

If you are often traveling abroad, it is important to know how health insurance works in other countries.

If you are traveling to the European Union (EU) or the United Kingdom (UK), health insurance will cover you in case you need medical assistance in case of illness, accident, or maternity. What will be reimbursed is based on the country you are traveling to. In most cases, everything will be reimbursed in these countries.

If you travel to a country outside of the EU and UK, your health insurance will cover up to twice the costs that would have been paid in Switzerland. Outside of hospitalization, this should be good enough. However, in the case of hospital coverage, the insurance only has to cover 90% of the costs that would have been paid in Switzerland.

If traveling to a very expensive country like the US, Canada, Australia, or Japan, complementary health insurance is generally recommended. Indeed, the coverage from the Swiss health insurance will likely be insufficient, and the remainder could be very expensive.

Which insurance deductible should you take?

Choosing the best health insurance deductible is important.

The deductible is the amount you will pay before the insurance covers anything. The deductible is per year. For instance, if your deductible is 2000 CHF and you spend 1900 CHF on health expenses, the insurance will not cover anything.

As I mentioned before, there are several deductibles that you can choose from:

- 300 CHF

- 500 CHF

- 1000 CHF

- 1500 CHF

- 2000 CHF

- 2500 CHF

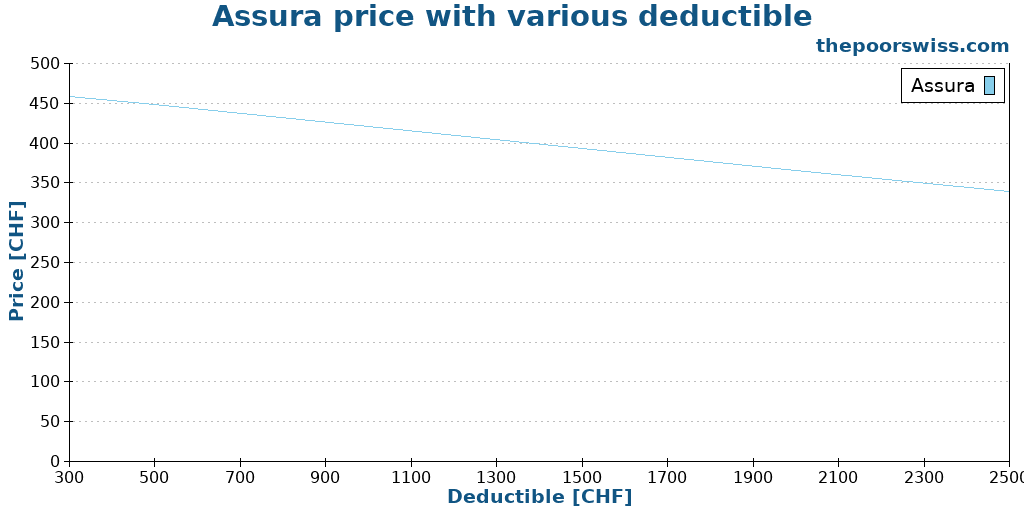

With a higher deductible, you get a lower monthly fee for your health insurance. For instance, here are the monthly prices for Assura for an adult with various deductibles.

Now, to choose, you have to estimate how much you will have in health costs. With so many deductible options, it sounds complicated to select the best one.

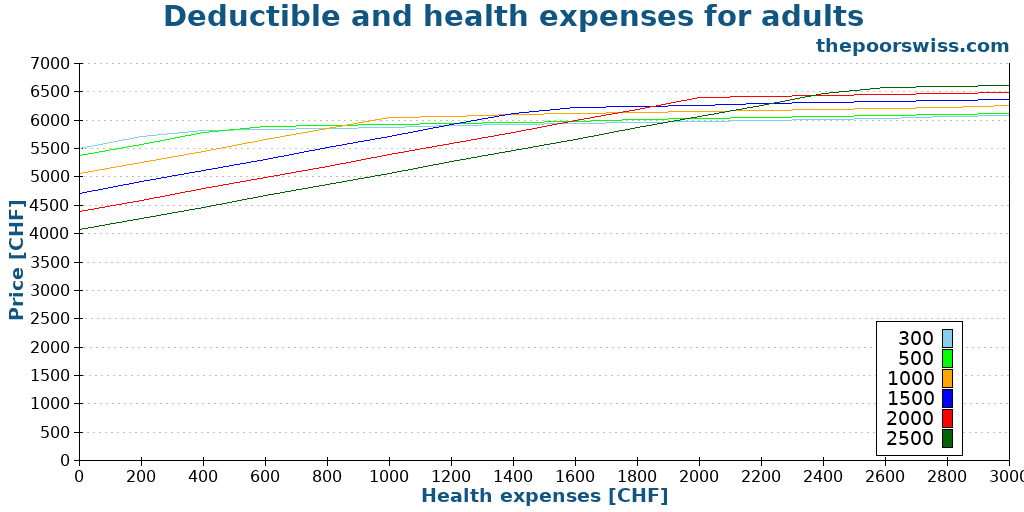

However, it is simpler than that because only 300 CHF and 2500 CHF make any sense. All the other deductibles are useless. Here is a simulation with the same Assura case and various levels of health expenses.

We can see on the graph that only two deductibles are interesting: 300 CHF and 2500 CHF. If you spend below 1900 CHF, the 2500 CHF deductible is the best. If you spend more than that, the 300 CHF deductible is the best. It is pretty simple, right?

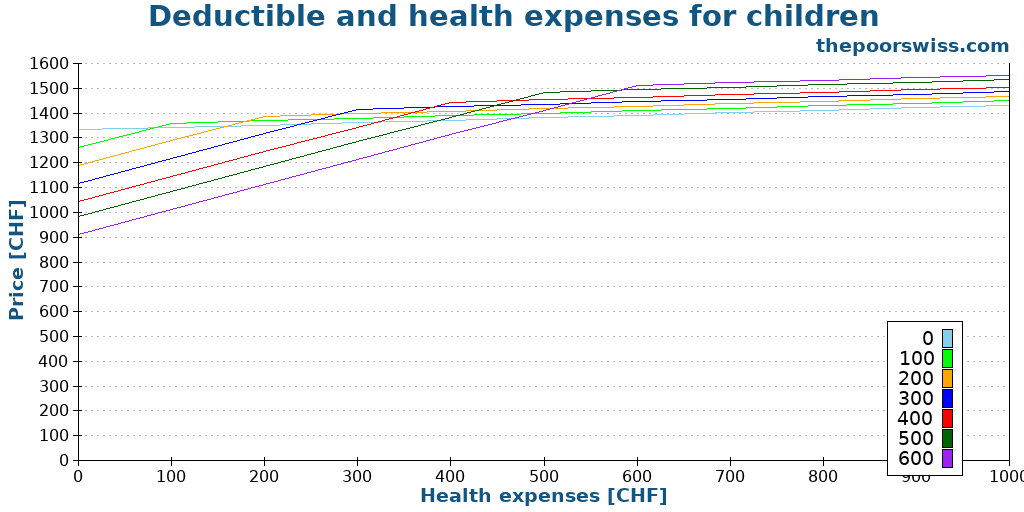

We can do the same for children (still using Assura as an example):

The logic is the same again. Only two deductibles make sense; all other deductibles are wasting money. If you spend more than 500 CHF per year, you should use the 0 CHF deductible. And if you spend less than 500 CHF per year, you should use the 600 CHF deductible for you kids.

Now, if you take the highest deductible, you must be ready to pay these fees. You could depend on an emergency fund for that. If you do not have one, you may consider starting an emergency fund.

Which insurance model should you choose?

This health insurance guide mentioned before that there are several insurance models that you can choose. Now, not all insurances offer them all. But there are four principal families of insurance models:

- Standard Model.

- Family Doctor Model.

- Telmed Model

- HMO Model.

These models will have the same coverage. The difference is what you must do when you have a health issue.

Now, of course, you can still directly go to a doctor or the hospital in emergencies. It is only in the case of usual health issues that these restrictions will apply.

If you do not respect the rule and go directly to a specialist, this will likely not be reimbursed. Additionally, you will likely be excluded from this model and will have to go back to the base model. So, it is important to follow the rules or use the standard model instead.

The Standard Health Insurance Model

With the standard model, you can go to any doctor directly. You can change doctors anytime, and you do not need to inform your insurance about that.

This model is the most expensive because the insurance has no choice on which doctor you choose.

The Family Doctor Health Insurance Model

With the family doctor model, you have an assigned doctor. You have to go to this doctor, and he will send you to specialists if need be. But you cannot go to another doctor even if you want to unless there is an emergency. Gynecological appointments do not need to go through the family doctor.

Some insurances are limiting which family doctors they accept. It is also worth noting that some insurance providers have different tiers of doctors, and the price will be different.

This model is between 10% and 20% cheaper than the standard model.

The Telmed Health Insurance Model

With the Telmed model, you must call a health call center before seeing any doctor. They will then choose the doctor you must go to, either a specialist or a generalist, based on your issue. Once you have been there, you do not need the call center anymore for this issue.

It is worth mentioning that you may expect to discuss the health issues on the phone already.

This model is also between 10% and 20% cheaper than the standard model.

The HMO Health Insurance Model

Finally, with the HMO model, you have to go to a particular health center. You do not have an assigned doctor but a designated health center. So, likely, you will always see different doctors.

Since there are few health centers, you may have to go farther to see a doctor. This is the main issue of this model since it depends on where you live.

This model is generally the cheapest. But not all insurance providers offer it. For instance, Assura, the most affordable health insurance in Switzerland, does not offer this model.

How to choose a model?

There is no definite rule on which model to choose. You should select the cheapest model that is still convenient for you.

For instance, if you have an HMO center close to your house, it may be great to choose an HMO model. But if the next HMO center is 40 minutes away, you may want to avoid this.

Most people should avoid the standard model. It is simply too expensive. Between the other three models, you should choose the cheapest one you are ready to accept.

We are using the family doctor model because the next HMO is too far from us.

Do you need accident insurance?

The base health insurance and accident insurance are closely tied together. Accident insurance is also mandatory in Switzerland. And you need to take your accident insurance with your health insurance.

But, if you work more than 8 hours a week, your employer is responsible for your accident insurance. So, only people working less than 8 hours a week need to get accident insurance.

If you need one, you should ask for accident insurance when you take a base health insurance. It is not very costly, and the coverage is the same for each insurance provider.

Save money on your health insurance

There is no denying that health insurance in Switzerland is costly. For us, it is about 12% of our budget. And some people spend up to 20% of their budget on health insurance coverage. And every year, the prices are increasing! So, we should do our best to spend as little as possible on it.

In this health insurance guide, I cover how to save money on the base insurance. All insurance providers have the same coverage since the law decides on the coverage. And you do not have to use the same provider for the base and the complementary insurance.

Do not hesitate to change insurance

The first thing you need to do is compare and change often. There is no reason to stay with an insurance provider if it is significantly more expensive than another.

Yes, some insurances are a bit less convenient than others. But if you can save several hundreds of francs each year, there is no reason not to change. Every year, you should check if your base insurance is still the cheapest!

Unfortunately, the premiums increase each year. Since some insurances increase more than others, it is challenging to keep the cheapest insurance.

Insurances are in for the money! There is no reason not to compare!

Choose the best model and deductible for you

We have already talked about deductibles. But I will repeat it: You need to take the best deductible for your case! If you spend less than around 1900 CHF, you want the 2500 CHF deductible. Otherwise, you want the 300 CHF deductible. There is no reason to use any other deductible!

We have already talked about the insurance model. Most people should take the model that is the cheapest. If you have access to a family doctor recognized by your insurance, choosing a family doctor model is an excellent way to save money. And if you do not mind, you can save a lot by using a call center.

Pay your fees upfront

Moreover, you can pay all your monthly fees at the beginning of the year at once. Some insurance providers will give you a small reduction if you do that. Some also will offer you a discount if you pay per quarter. For instance, Assura gives you a 2% reduction if you pay annually.

That is not a lot, but that could be a way to cut your expenses more. Do not forget to consider that you could have invested this money instead. I do not do that. But, if you do not invest aggressively, you can get 2% returns. It is a good investment without risks.

If you want further examples, you can read about whether you should be paying your bills early.

Ask for health insurance subsidies

Finally, if your income is low, you may be eligible for help from your municipality or the canton. If your income is below a certain threshold, they can pay a part or even all your insurance bills. This can be very helpful if you have several children and medium incomes. When we were young, we got support for part of my family’s health insurance.

I cannot tell you the threshold since it differs from one canton to another. For example, you can request it from the municipality administration in my canton. But in some cantons, you must request it from the state administration. If you think you would be eligible, contact your canton or municipality administration, and they will help you ask for it.

Be aware of possible reductions

Some insurance providers also have some possible extra reductions. It is not always easy to find them, but they could be interesting.

For instance, when I was with Helsana, I could save money each month if I only went to one pharmacy in particular. I did not take this offer since this pharmacy was not in my village. But if I lived in a city, I would have taken it.

With most insurance providers, you can also save money if you have several family members with the same provider. Grouping together can save a significant amount with some insurance. For instance, saving 5% to 10% is not uncommon.

You should do some research and check what your insurance can offer you!

Suspend base insurance during military service

This tip is very specific. If you serve in the army for over 60 days, military insurance will cover your health insurance. Since most men do a military service of about four months, this could mean a nice saving.

Unfortunately, this is not possible for annual repetition courses since they last less than 60 days.

Which health insurance should you choose?

Now that you know which model you want and which deductible is best, this health insurance guide will help you choose an insurance provider.

The base insurance is a legal matter, so each provider has to cover the same things. So, for me, you should simply choose the cheapest base insurance you can find. And you should change as soon as it is not the cheapest anymore.

There are a few cases where you may not want to choose the cheapest insurance. First, unless you take the standard model, some insurance will restrict you to some doctors. And they may not accept your current doctor.

If you have been with the same doctor for a very long time, you may not want to change. So, you may have to choose a provider that accepts him even though it is not the cheapest. Or you can take the most affordable standard model.

There is another case where you would not want to take the cheapest option. If you have a condition and often go to a hospital not accepted by the most affordable option. You may want to keep it with your current hospital.

Otherwise, I recommend that you take the cheapest insurance that you can find.

Be careful about health insurance comparison tools

A health insurance guide would not be complete without discussing health insurance comparison tools. Some comparison tools can help a lot in choosing health insurance in Switzerland.

You have to be very careful about these comparison tools. Many of these comparison tools have issues:

- Some comparison tools are incomplete and only show insurance they have deals with, often not the cheapest.

- Some comparison tools are run by insurance brokers.

- Some comparison tools are full of ads, showing up before the comparisons themselves, without enough transparency.

The prices of insurance vary significantly by age and also by canton. Therefore, for all comparison tools, you must enter this information to get accurate results.

The best one is the official Health Insurance comparison tool from the Swiss administration.

The priminfo comparison tool comes directly from the government. It is very fast and very complete. This comparison tool is the only one I trust. It is also straightforward to use. It is available in the three national languages of Switzerland (French, Italian, and German). Unfortunately, it is not available in English, but your browser should be able to translate it for you

The prices of insurance vary significantly by age and also by canton. Therefore, for all comparison tools, you must enter this information to get accurate results.

Comparison for my case

For instance, in my case, here are the five cheapest insurances with 2025 premiums:

- Sanitas at 323.65 CHF per month, with NetMed model (HMO)

- Concordia at 324.15 CHF per month, with HMO model or smartDoc (telemedicine)

- Sympany at 324.35 CHF per month, with FlexHelp 24 (telemedicine)

- Visana at 331.95 CHF per month, with Tel Care (telemedicine)

- Concordia at 332.05 per month, with MyDoc (family doctor)

If you have access to a good HMO close to you, the first and second options would be good. In my case, this is not the case, since the doctors in my village would mean paying a premium. And I would rather not deal with telemedicine. Therefore, the best case for me is Concordia at 332.05 CHF with my family doctor. This is a fair deal because I pay less than 100 CHF more with that deal, and I can walk to my doctor.

Looking at the details is essential when dealing with health insurance.

Should you take any supplemental insurance?

Finally, we finish this guide with the main types of supplemental insurance. There are many more, of course. But these are the ones that people use the most. If you want even more information, you can read our guide on supplemental health insurance.

There are two groups of supplemental insurance:

- supplemental hospital insurance.

- supplemental outpatient insurance.

It is essential to mention that you generally need to fill up a health questionnaire, sometimes with your doctor, to get supplemental insurance. For instance, dental insurance will require information from your dentist.

Indeed, insurance providers are free to refuse you or change the conditions for supplemental insurance. If you are in bad health, it will be complicated (or expensive) to get supplemental health insurance.

Supplemental Hospital Insurance

Base health insurance will pay for your hospital fees. However, it will only cover your expenses in the general ward, and some insurance will limit which hospital you can go to. Supplemental hospital insurance, also called supplemental inpatient insurance, can help improve the quality of your stay in the hospital.

Instead of general care, you can decide on semi-private care. Such insurance guarantees you will only end up in a room with two beds. It also means that a senior physician will take care of you. It can be expensive, but many people take this insurance.

You can also use private care supplemental insurance. These insurances will cover your expenses for a private room in a hospital. Furthermore, you will generally have a chief physician for your treatment. But this can be very expensive, so very few people use this kind of supplemental insurance.

Finally, you can also opt for the free choice of hospital supplemental insurance. It will let you choose any hospital in Switzerland and cover your expenses there.

For most people, these insurances would not be necessary. However, semi-private care is a good option. Private care is simply too expensive and not worth it. But having a two-bedroom when trying to recover can be quite enjoyable. But of course, it is pure comfort. A free choice of hospital can also be a good deal.

For women who plan to have children, it is good to have semi-private care insurance. This insurance will let you choose a clinic instead of a hospital and your doctor. And you will be in a two-bedroom. So, it could make a significant difference in childbirth and the first days after giving birth. Nevertheless, some hospitals only have rooms with two beds for mothers, so semi-private will not be very interesting.

Now, for young people in good health, it is fine not to have any supplemental hospital insurance.

Supplemental Outpatient Insurances

Outpatient insurances are a bit more complicated since there are many different options. These insurances cover things outside of the hospital.

The most used ones cover some treatments not covered by the base insurance. For instance, there are dental, supplemental insurance, and glasses supplemental insurance.

There are also some supplemental insurances for travel. For example, one that many people use can cover accidents in other countries, hospital coverage in other countries, and vaccinations for traveling abroad.

There are also some more special insurances. For example, there are supplemental insurances that will pay back your costs of traveling to the doctor. And some insurances will pay for improving your health. Such insurance includes things such as medical checkups and gym memberships.

These insurances are dependent on each person. If you travel a lot outside the EU, it is great to have some travel insurance. In my case, this is even mandatory for my job.

Some supplemental insurances can also make sense if you know that you will use them a lot. For instance, dental insurance can be great if you know that you have many dental care expenses. But you must do the math to see if it is worth it. You should only take such insurance if this makes you save money.

One supplemental insurance that can also be great is preventive care insurance. For instance, this could cover checkups every few years. They can also include a gym membership, for example.

And some of these insurances come in packages. So you need to consider them entirely and not per single item.

FAQ

Who needs health insurance in Switzerland?

Everybody. Health insurance is mandatory in Switzerland for every resident, including children and infants.

Who needs accident insurance in Switzerland?

Everybody. Accident insurance is mandatory in Switzerland. But, if you are working, your company will cover your accident insurance. If you are not working, you must apply for accident insurance.

How many deductibles are available for health insurance in Switzerland?

There are six possible deductibles: 300, 500, 1000, 1500, 2000, and 2500. As a rule of thumb, you should choose a 300 CHF deductible if you spend more than 1900 CHF a year on health expenses. Otherwise, you should choose the 2500 CHF deductible.

Are supplemental insurances mandatory in Switzerland?

No. All supplemental insurances are entirely optional. Some of them will help you save a significant amount of money, while others are very rarely useful.

How often can I change health insurance in Switzerland?

You can change your base insurance every year. You need to send a letter to your insurance. Your letter must arrive at least one month before the end of the year. As for supplemental insurance, they all have different rules for cancellation, so you will need to check your contract. Generally, you will need to cancel them six months in advance.

What happens to supplemental insurance if I cancel the base health insurance?

If you cancel your base health insurance, nothing happens to your supplemental health insurance with the same provider. They are different contracts with different cancellation rules.

Conclusion

If you have read this health insurance guide entirely, you should have an excellent understanding of how the health insurance system works in Switzerland. And you should know how to save money on your Swiss insurance.

It is essential to choose the insurance policy that works best for you. Since base insurance is the same for all providers, you can generally pick the cheapest one. But make sure you pick one that is convenient. You do not want to drive 40 minutes to a doctor’s!

Unfortunately, even if you take the cheapest health insurance, it is still costly. And you will always have to pay for many things yourself. If you have a large deductible, it would be great to have at least this amount in your emergency fund.

The quality of healthcare in Switzerland is excellent. However, I do not like the health insurance system. Since each health insurance covers the same thing, it should be federal insurance instead. And the price should be fixed by law. Instead, every year it increases, and every year we need to compare them. It does not make sense! For me, the base insurance should be much cheaper and cover fewer things.

Since health insurance is so expensive, you may want to find some ways to save money in Switzerland.

Do you have any more questions? What health insurance do you have? Do you have any tips for lower health insurance coverage? Is something missing from my health insurance guide?

More reading

9 Reasons to Live in a Small Village

City or Countryside? Discover the advantages of living in a Swiss village, from lower taxes and cheaper rent to a quieter lifestyle.

Swiss Life Select will not help your finances

Warning: Read this before signing. Learn why Swiss Life Select might not be the best partner for your finances and the pitfalls of commission-based advice.

Buy or Rent – Which is Right for You?

The eternal debate. Buy or Rent in Switzerland? We analyze the costs, benefits, and hidden factors to help you decide which is financially better.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste ,

Good article, however, I’m confused with the explanation for how to calculate the threshold amount in your provided example.

Your formula of: (1.1*(A – B + 300)), where A = 4308 and B = 1874.76 does not result in the stated threshold amount of 1904.76.

Using your formula and the variables, I arrive at 3006.56.

Can you please provide a further explanation as to how you arrive at 1904.76, clarify if there is a mistake in the stated formula, or whether there is an additional step required?

Thank you,

Charlie

Hi Charlie,

Thanks for pointing that out. B should be 2874.76 (the first digit was wrong!). With that, you end with the proper result :)

Ah! Ok, now it works. I ended up with 1906.56 rather than 1904.76, but I’m assuming the negligible difference is due to rounding, and this is just for estimation purposes anyways.

Thanks!

Charlie

I would not worry about 2 CHF there indeed :)

And you have to update it every year based on the premiums and for each insurance, this is only one example.

Thanks so much Baptiste for writing this guide! I’ve been reading you for 3 years now. Last month I moved to Zurich and I instantly knew you would have something written on insurance and that you would be able to help me find the right one. Thanks so much, this is way more clear now!

I am glad this was useful! Thanks for following me for so long :)

Hello,

Are there providers giving reductions if you combine supplemental with basic insurance with them?

thanks for the article!

Hi Jan,

Normally not. However, sometimes if you move several people together to them, you can negotiate a deal, generally for the first year only.

Hello,

Thanks for the excellent article.

I wanted to follow your advice and just take the cheapest one for the chosen model. However, I learned from the comments that there are “not recommended” providers (e.g. Assura)

All other things being equal, are there more providers that you would (not) recommended? Generally I would prefer to spend a little more to avoid irritations.

Hi Jan,

I don’t really agree with that. I have Assura and never had an issue. They reimburse quickly and without issues.

I would still recommend using Assura. I had Helsana before that was much more expensive and had not a better experience with either.

Hi! Great article. I just arrived in Zurich and this is extremely helpful.

I had two people from Zurich facebook groups contacting me saying they can get me cheap offers. From what I understood, in Zurich everyone is paying almost 300 CHF/month or more, and they say they can bring it down to ~220 CHF, which I find strange. One of them told me about a package for 220 CHF which doesn’t include dentist, medicines, ambulance transportation, hospital care, or abroad care. Isn’t that the basic care that any package should include? These two people say they work for Afsana GmbH and Godeni versicherungen GmbH. I’m quite suspicious of this.

Another question is regarding simulations I did on Assura and Sanitas.

Sanitas has a package called “Network model – Medbase MultiAccess”. Which model is this? In case it’s the HMO, they have a medical centre very close to where I live, so I guess that’s a good option for me?

As for Assura they give me 3 packages very close to each other on price. One is “Qualimed” based on telemedicine, then there’s the “Family Doctor” , and then the “Pharmamed” which also sounds like a HMO.

The article is amazing but I am still quite confused by looking at these different offers. Any extra help?

Thank you!

Hi Tomas,

In general, I would be careful about any strangers providing offers like this…

I don’t know any of these two companies but I would avoid dealing with anybody cold contacting you like this.

The base insurance is indeed without dentist, not necessary all hospitals, … But you don’t need anybody to get the best offer. Just use a comparator, choose the cheapest and be done with it.

Unfortunately, each insurance has different models that don’t necessarily match the standard models. It sounds like an HMO for Sanitas. You need to make sure that you can use the center close to where you live.

Telemedecines means you need to call first before you go anywhere but can generally choose your doctor. Pharmed is a combination of medicin de famille and pharmacy, you can only go to the pharmacy that they allow. In our case, our local pharmacy was not included, so we did not take it, but it is a good deal if you have a pharmacy in the list close by.

Thank you so much for your reply! I’ll follow that first piece of advice.

1) The package from Sanitas is 288 CHF, it’s an HMO with both a pharmacy and a medical center close to where I live (it seems like I can use this center).

From Assura I have:

2) Qualimed, telemedicine, for 263 CHF

3) Medicin de Famille, for 270 CHF

4) Pharmed (medicine de famille + pharmacy), for 270 CHF

Is this assessment correct?

#1 looks great but it’s the most expensive one.

#2 I would rather exclude since I’d prefer not having to call and since it is not much cheaper than the remaining options.

Between #3 and #4, why would I choose #4? #4 I can only go to a few pharmacies (I see the closest one I have would be 20 min away by public transportation). What about #3, does it mean I will be able to go to any pharmacy? If so, why would anyone select #4 if #3 is the same price?

Thank you!

Hi,

Your assessment looks correct to me! I would personally go with #3. It seems indeed weird to get #4 if it is not cheaper. Normally, with #3, you should be able to go to any pharmacy indeed.

For me, #3 has all the advantages. #1 is okay, but I would not do pay the premium.

Sorry, I promise this will be the last question!

I found a deal by CSS (Assana) with the same price as #3 (a few cents cheaper) that is a mixed model including family doctor and telemedicine, with a medical center that is quite close to where I live (~10 min walking distance).

#3 allows me to select a family doctor from a big list in my district, so I guess I would be able to select a doctor that may be even closer to my home.

What are the differences between them? WIth #3 I can go without calling and with the new one by CSS I have to call beforehand – is this a disadvantage, or not? Which one would you recommend? I’m guessing #3 would be best as long as I can get a doctor closer to me than the CSS one? And if not, maybe the new one by CSS is better?

Hi,

If you have to call the center and then the doctor, I would take the deal with only calling your family doctor.

Keep in mind that many doctors are full, so if you have not yet a family doctor, make sure you can have one spot in one of the supported ones.

In any case, you will have to call once, to the doctor directly. I did telemedicine for a few years, it’s not that bad, but I prefer direct access to my family doctor.

Hello, there,

and what about accident cover for the supplementary insurance?

When I am employed I do not need the accident cover on my basic insurance (covered by the employer), but does this also apply for the supplementary?

With Helsana, I do, currently, pay 5chf/mo of accident cover for all my supplementary insurance (no coverage for basic ofc), and I am looking if I can optimise that too.

Thanks in advance!

Hi,

I am not sure, I would ask Helsana. But I think this does not cover it if you are employed. This is extra coverage that would not be covered by mandatory health insurance.

Thank you very much for the comperhensive explanation on the swiss health insurance system!

One question: in NL there is a suplementary insurance specifically for dental. All most all health insurance offers this and it is very popular.

Is there such offers/sistem in CH? Or is this included in the basis insurance in CH?

Hi LearningFI,

Yes, there are some supplementary dental insurances. Almost nothing is included in the base insurance. Dental supplementary insurances can be a good deal.

Here, also, most health insurance providers offer such insurance as well.

Thanks for stopping by!

Hi!

I’d never ever go back to Assura, no matter how cheap they may be. They will simply not pay in cases when they have to. Will you take them to court? Whether you win or loose, you’ll be losing both money and time in the end. It is not by accident that satisfaction ratings with assura are very low (see comparis).

Hi Daniel,

Yes, with Assura, you get what you pay for, basically nothing. I also was with them for a few years. I almost never use my health insurance, so I was not an issue for me. But I get that it could have been on if something happened.

Nobody likes Assura. But health insurances are really too expensive for many people. So it makes sense that they have a lot of clients.

Thanks for stopping by!

Thank you for the fantastic article. I do have an additional question.

Since I registered in Switzerland last August and I have contracted my health insurance this month, I got a bill for the first months I “wasn’t “ insured. The problem is that I cannot pay all at once. Is there a way to avoid these first months, in which I was insured in another country? Is there a way to postpone the payment or break it into two payments?

Thank you in advance,

Javier

Hi Javier,

Unfortunately, no. We had the same case for my wife where we had to pay several months backward since the day of arrival. This is the Swiss law for people that get residency.

As for postponing or breaking it down, this should be possible depending on your health insurance provider, you will have to contact them.

Even as a Swiss born I learned some new things here!

I just wanted to point out the government owned insurance comparison service Priminfo:

https://www.priminfo.ch/

Unfortunately it’s not available in English, but as a gov owned service I’d say it’s probably a lot less biased than other services. Also gets you the results much quicker, as they have no ads and don’t ask unnecessary details. :)

Hi Julian,

I am glad you learned some new things!

I always forget about this one. You are right, it’s a great one. I am so used to comparis that I have a tunnel vision on that. I will add it to the article.

If people speak a national language, it’s much better than comparis as you said.

What insurance are you currently using?

Thanks for stopping by!

You made an interesting comparison of different levels of deductibles. I came to the same conclusion when choosing my health insurance for the first time ever, two months ago.

It is very comprehensive article with a lot of research made beforehand, but worth it! Thanks for the work!

Hi Miro,

I am really glad you like it!

As you said, most deductibles are useless and it is pretty easy to do the computation. I still do not understand people that do not use 2500 or 300.

Is there something missing from my post?

Thanks for stopping by!