December 2021 – Usual end of year month

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

2021 really flew by. I cannot believe it is already over! Overall, this was a weird year, with COVID and then the birth of my son. It did not look like any other year.

Nevertheless, December 2021 still felt a little like a usual end-of-year month. We had the (mostly) usual celebrations and the usual end-of-year bills.

Overall, it was a good month for us. So, let’s see the details of what happened in December 2021.

December 2021

For us, December has always been a month for the family, and this year was no exception. The parties were scaled-down but still great! One of the parties was canceled because two people had symptoms, but this will be done later in January instead. So, family time in December was quite good!

It was also the first Christmas for our son. He got plenty of presents and fun! It was not always easy going from one house to another and making him sleep, but overall, it was a good time.

As for sleep, this did not improve at all. We went from a cold into a growth spurt. And now, our son is having some pains, likely early teeth. We have realized that there is always something. We cannot wait for sleep to get better. It will not, at least not in the early years. We will have to make due. I plan to sleep entire nights again in four or five years.

But except for a few minor things, he is in good health, which is what matters most.

Financially, it was not a bad month but not a great month either. The end of the year is always a time with many yearly bills. Adding to that a few non-recurring bills, we spent more than we are used to. But in the end, we still saved 40% of our income. So, we cannot complain!

Expenses

Let’s see the details of our expenses in December 2021:

| Category | Total | Status | Details |

|---|---|---|---|

| Insurances | 1237 | Above Average | Health and legal insurance |

| Transportation | 746 | Well above average | Car insurance and taxes |

| Communications | 141 | Above average | Internet and one online subscription |

| Personal | 2359 | Well above average | Bills for the blog, some wood, replacing an electric blind motor |

| Food | 309 | Below average | Standard groceries |

| Housing | 900 | Above average | Heating, mortgage interests, and power |

| Taxes | 3802 | Average | The usual taxes |

Overall, we spent 9465 CHF. Without taxes, we spent 5694 CHF. This amount is higher than our goal. However, the end of the year always has some extra bills. So, overall, it is not too bad.

For instance, every three months, we pay the first pillar for the blog and the power bills. And at the end of each year, we pay the car insurance, car taxes, legal insurance. When everything happens together, it makes a big difference to our expenses.

Aside from this, I also bought more wood. We now have more than enough for this winter and likely the next one. And we had to fix one of our electric blinds. The motor was dead. It was a huge pain to find a new motor since the company that did them recently went bankrupt. But we found someone that could repair the motor. And we only paid about 500 CHF for the entire repaid.

So, overall, we spent more than usual this month. But as end-of-year months go, this one was not that bad.

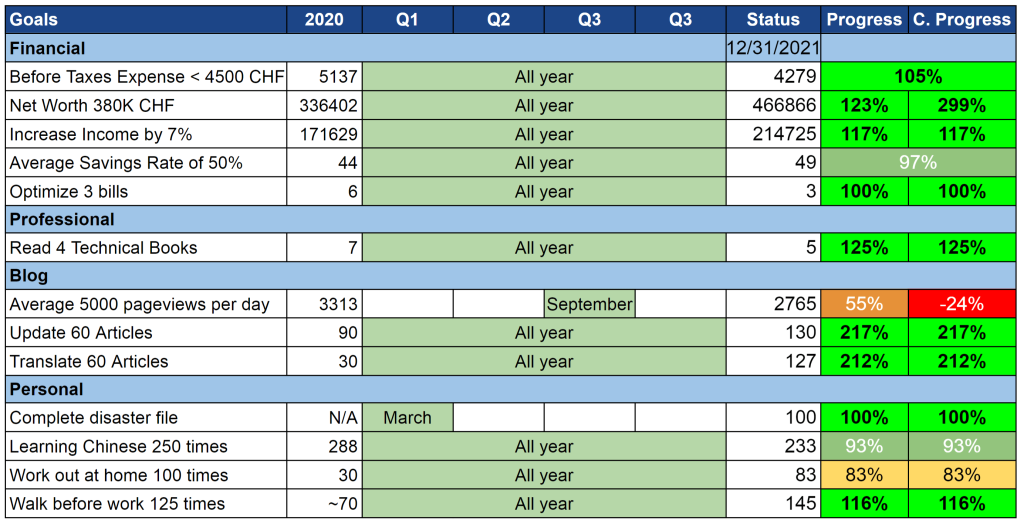

2021 Goals

Let’s take a look at our goals by the end of December 2021:

The year is over. It means that our goals are over as well.

Overall, I am satisfied with our goals this year. Not everything went well, of course. Indeed, we failed four of our goals this year. But most goals are passed, and some goals were not adequate.

I do not want to spend too much time on our goals in this article since I plan a full review and new goals for 2022.

During the month, I made some progress on several goals. I was able to walk again in the mornings and do some workouts. But the workout goal is still a big fail for this year. On the other hand, I worked out twice more (almost three times!) more than last year, so I should be happy about that. I also did not do enough Chinese.

Unfortunately, our savings rate this month was relatively low at 40%. We would have needed 56% to reach our goals of 50% average for the year. But 49% is already great!

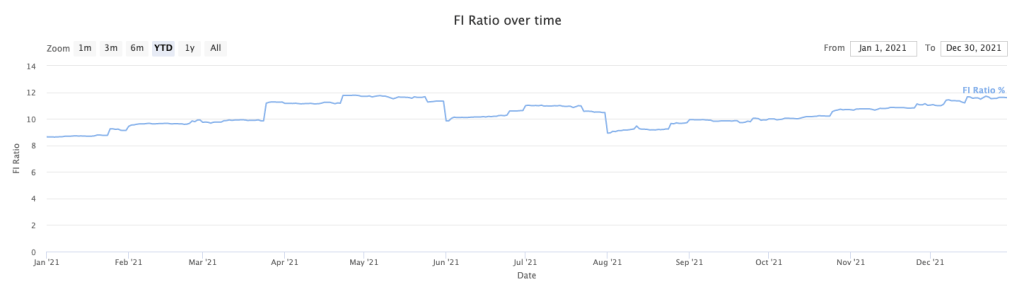

FI Ratio

Let’s take a look at our progress towards Financial Independence:

This month, we went from about 11% to about 11.5%. A 0.5% monthly increase is not too bad, but we would prefer to advance slightly faster than that.

However, when we look at the entire year, we barely made any progress in the second half of the year. The reason is that our average expenses increased significantly during the year.

One of my readers pointed out that this was not entirely accurate since I would not spend as much in retirement, especially for taxes. We currently spend about 120’000 CHF per year, including taxes. But I do not think we will spend more than 100’000 CHF per year once retired.

Once I get some quiet time, I will add fixed expenses to my graphs and show both lines in these monthly updates.

The Blog

There is not much to report on the blog during December. I managed to do a fair bit of translation, but I did very little this month aside from this. I only work on important updates and projects and delay everything else for the time being.

As for traffic, it is the usual drop. Traffic went down about 10% compared to last month again.

Next month, I will continue doing little but translations. In 2022, I want to get to where new articles are directly published in two languages.

Next Month – January 2022

January means a new year! And a new year means new goals. I am still not entirely set on our 2022 goals, but they will be simpler than the 2021 goals. I do not have enough energy to take on large projects.

Financially, January 2022 should be very standard. I do not see anything special happening next month.

More reading

April 2023 – Another expensive month

In April 2023, we saved a significant portion of our income, but it was still a very expensive April, compared to previous years.

2024 Goals and 2023 Goals Review

We review our 2023 goals and discuss our new 2024 goals. Look at everything that happened during 2023 and our plan for 2024.

May 2023 – Good month and small vacation

May 2023 was a good month, with a short vacation to Annecy and had great time with friends and family. We saved a large portion of our income.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

I’m curious about your “Disaster File”.

Would you be willing to share an outline or a template ?

Thanks and keep up the excellent work !

Gerry

Hi Gerry,

Since that was requested many times, I have added the table of contents of my disaster file in my disaster file article.

I hope this is useful :)

I’m really amazed at how you keep your grocet bill so low…

Congratulations to your 2021 achievement! And I like the home workout goal, doing much better than in 2020 haha.

Thanks, Yasi! It was not too difficult to beat 2020 on the gym goal :P

We average about 550 CHF per month in 2021. We used to do better but seems we are buying more stuff this year.

Hi Baptiste,

Thank you for your continuous great articles and breakdown. Wanted to see if you could help with the following questions:

Your housing cost is only 900 a month. Please could you help show a breakdown of how this is calculated?

The numbers you show are very helpful and I use as a review for my personal situation, although I struggle to get close to your number. Mine is: 1’673.

– Principle: CHF 758

– Interest: CHF 221

– Building rates: CHF 583

– TV licence: CHF 28

– Electricity: CHF 43

– Internet: CHF 40

Also, this excludes a “maintenance” budget, recommended at 1% of the property value each year.

Would love to hear your thoughts and see where I can optimise.

Thank you

Tyrone

Hi Tyrone,

In December my housing costs were:

* 350 CHF power bill

* 305 CHF for my mortgage (interests only)

* 245 CHF heating

If by principle you mean amortization, I don’t count that as an expense. I am just moving money from cash into real estate. And even indirect amortization is just moving cash into a third pillar.

Removing that, it seems we are quite close together.

What are “building rates”?

TV and Internet, I count in my communications category.

Hi Baptiste

Thank you for your help and details.

The building rates are the fees paid to the community (I live in a flat) – shared insurance, electricity, heating, cleaning, garden etc. Yes it looks similar.

How do you count/report, budget the amortisation? Reading your articles I believe you don’t track increases in “property value”. Would be great to understand you’re thinking around this.

I see paying back the amortisation as an expense because:

– although it does improve my “net worth”

– I have to budget it and pay it out

– to realise this money from the property it would need to be sold or mortgage

Mapping

– Principle: CHF 758 (amortisation)

– Interest: CHF 221 (305)

– Building rates: CHF 583 (245)

– Electricity: CHF 43 (350)

– TV licence: CHF 28 (communication)

– Internet: CHF 40 (communication)

Thanks for your help.

Tyrone.

Hi Tyrone,

Thanks for the explanation :)

I don’t increase the property value, but at the end of the year, I will reduce the debt in my net worth. This will increase my net worth.

I just wait for the bank report and use the current value of the mortgage to update my assets. I could do it month after month, but it does not make such a difference.

For me, it’s just like moving money to my 3a, it’s not present in my budget, but only in my net worth.

Hi Baptiste,

Thank you, this has been helpful :)

– It makes sense the Net-worth calculation approach (reducing debt)

– I do include my pension, amortisation in my budgets expenses as its “money” that is going out. This helps me to plan for it in the coming year.

Thanks for your help and discussion, keep up the great articles, the are excellent.

Have a good week.

Tyrone.

Hi Tyrone,

The important thing with your budget is that it works for you :) It does not have to be the same as mine indeed.

Actually, I don’t really have a budget anymore, just tracking expenses and earnings in different categories.

Happy New Year Baptiste!

Guess (I know I’m repeating myself ;-) that once you’ll find a way for us to follow-up on comments on this forum we’ll return more often…

Regarding yearly budget/spend guess it’ll also depend on whether you’ll have more kids (and the sports or activities they’ll take part in) and your holiday travel tastes…

As to spending less when retired, I’ve read numerous warnings about not underestimating the needed budgets as a lot of deductions possible during an active life also disappear…

Happy New Year Pedro,

Yes, I know this is a wanted feature :) Unfortunately, there is no good way to implement that on WordPress :( I will keep looking.

Yes, my future budget will change a lot until retirement, no doubt. And it’s a good point that many deductions are not possible anymore in retirement. However, I will not spend 40K on taxes in retirement per year :) But retirees in Switzerland still pay taxes and sometimes more than we think!

Hi Baptiste,

your YTD performance is great, I ended year with +31,77 % (not complaining here LOL). Just curious do you post your portfolio composition on a blog somewhere?

All the best in 2022!

Hi,

Congraulations!

My portfolio is explained in detail in this article.

On top of that, we have our house (no appreciation), some cash (no appreciation), the second pillar (minor contributions), and our third pillars (good appreciation this year).

Salut Baptiste,

In my opinion it would be more detailed if you could say the YTD Performance without your cash deposit. Just the performance of your portfolio.

Best,

Thomas

Hi,

It makes sense. It’s just that my deposits are dwarfing my returns currently.

My current 1Y performance is about 21%.