The best calculators for your money!

(Disclosure: Some of the links below may be affiliate links)

If you need to compute something complicated, I have developed several calculators that you can use to simplify your life!

Second Pillar Calculator

If you want to know whether you should contribute to your second pillar or invest the money yourself, we got you covered! Our second pillar calculator will tell you which of these two options is more interesting and will even tell after how many years one option becomes better than the other.

Third Pillar Calculator

Just like the previous calculator, you may also wonder whether you should contribute to your third pillar, and we got you covered as well. Our third pillar calculator will tell you whether you should put your money into a 3a or into your free assets.

Retirement Calculator

Do you want to know how much money you need to retire? And do you want to know how long it will take you to accumulate that money?

Then, my Retirement Calculator is what you need! It will give you all the answers you need!

Once you enter all the information about your current situation, click Calculate, and you will know how much you need to retire. And you will also know how much time it will take you to get there. As a bonus, I am also showing your chances of success in retirement based on historical data.

Do not hesitate to try to play with your savings to see the impact it could have on your future! And increasing your income can also go a long way!

Pension or Lump Sum Calculator

If you hesitate between a lump sum and a pension for withdrawing your second pillar, this pension or lump sum calculator can help.

This calculator will compare both options together and tell you exactly which is financially better. This calculation can help you choose for your retirement.

Of course, this is only one part of the equation; you need to consider your financial situation and your risk capacity as well.

FI Planner

If you want to plan your financial independence like a pro, our FI Planner is what you need. This tool will help you plan your financial independence based on your exact needs.

FIRE Calculator

Do you want to know your chances of having a successful retirement? By successful, I mean not running out of money!

Then, this FIRE calculator will tell you exactly your chances of success. The results are based on more than 150 years of historical data.

Once you enter the parameters of your retirement, this calculator will tell you precisely what your chances of success were in the past. Moreover, it will also tell you how much money you would have ended up with on average after your retirement years.

Do not hesitate to try to change different portfolios to see how much difference it makes on your chances of success. But the best way to increase your chances of success is to reduce your withdrawal rate. Many people are aiming for a withdrawal of about 3.5% to improve their safety!

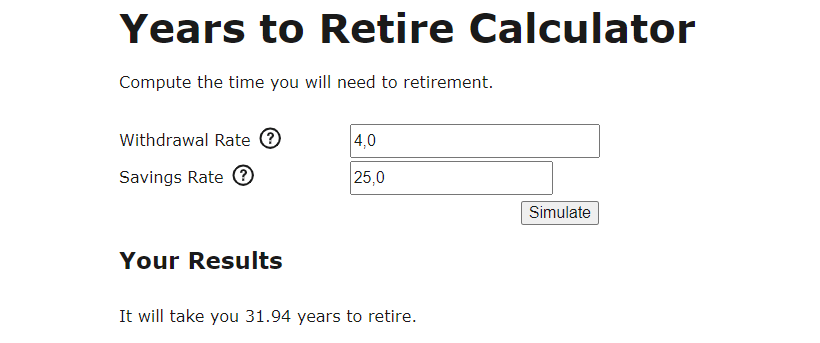

Years to Retirement Calculator

If you want to know how many years you need before you can retire, I have a calculator just for you! My Years to Retirement Calculator will answer this question for you!

Why use calculators?

Calculators such as these two will bring you a wealth of information about your situation. But most importantly, calculators allow you to simulate small changes:

- How much faster can I retire by saving 5% more?

- How much riskier is it to increase my withdrawal rate by 0.1%?

- What if I want to be able to retire for 60 years?

You can answer these questions at the press of a button by using calculators. These will save you a lot of time, and you will make you much more aware of your money!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide