Third Pillar: All you need to know to retire in Switzerland

| Updated: |(Disclosure: Some of the links below may be affiliate links)

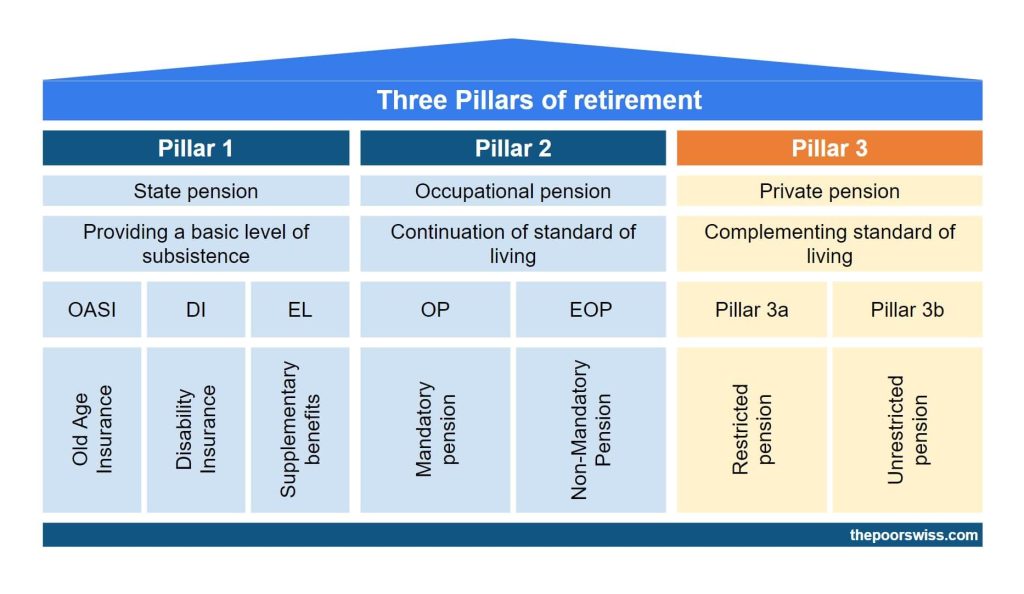

We already talked about the first and second pillars. We now have to cover the most important of the three pillars: The Third Pillar.

The third pillar is the only one that is not mandatory. Everybody is free to choose to invest in the third pillar or not. It is simpler than the second pillar. But there are many more choices that you can make. You can optimize a lot of things for your third pillar.

It is essential to optimize the investment of the third pillar as much as possible. Once you retire, your second pillar should still be larger than your third pillar. But there are not many things you can do with your second pillar.

In this article, you will find all the details you need to invest in a third pillar. And also what you can do to optimize your use of this third pillar.

Types of third pillars

The third pillar is your private pension. This time, there is no complicated name associated with it. It is known everywhere as the third pillar. There is just a slight twist. There are two different third pillars:

- Pillar 3a (restricted pension): Locked and tax-advantaged.

- Pillar 3b (unrestricted pension): Not locked but much fewer tax advantages.

In this article, I mainly discuss the first one, Pillar 3a. For information about the 3b, you can read Section Pillar 3b. Otherwise, when discussing the third pillar, I talk about Pillar 3a.

Pillar 3a

Even when we focus on Pillar 3a, there are still two ways to invest in a third pillar.

You can invest either in the form of a bank account or as insurance. We cover both of them in detail in the next two sections.

In both cases, contributions to your third pillar are tax-advantaged. Each year, you can deduct up to 7056 CHF (as of 2023) from your salary. The exact amount removed from your taxes depends on your income. You can generally save 2000 CHF per year in taxes by contributing the maximum to your third pillar.

The amount of the deduction can vary each year. If you want to keep informed about the maximum contribution, you should consult the official Swiss third pillar website.

Remember to deposit the money by the last day of the year to get a tax reduction. I would recommend investing early in your third pillar.

Since there are no tax benefits, you should never put more than 7056 CHF per year into your third pillar. It is not interesting to lock money without advantages. Most third pillars will prevent you from doing so. There are better alternatives if you do not have tax advantages. You will receive a certificate with your contributions every year. You can use this to file your taxes.

Unfortunately, not everybody can open a third pillar account. Indeed, you need to have a salary and pay for the first and second pillars. If you do not satisfy both requirements, you cannot open a third pillar account. This means that if you only have one income in your couple, only the employed person will be able to contribute.

How much you will get in retirement will depend on whether you have a third pillar in a bank or with an insurance company.

Pillar 3a and self-employment

So far, we have covered the case of employed people, with a salary. However, self-employed people do not get a salary directly. We are talking about sole proprietorship.

If the self-employed does not contribute to a second pillar, he can contribute to a third pillar. In this case, the maximum contribution is at most 20% of the net revenue of income and at most 34’128 CHF (five times the maximum contribution of employees).

Other than the maximum contribution, the other facts are the same for self-employed and employed persons.

1. The third pillar in a bank

The simplest third pillar is a bank account.

It is a regular bank account, except that it is locked. You cannot withdraw anything until you retire. You can directly deposit money into this locked account. Pretty much every bank has one or several third pillar accounts. The only difference between these accounts is the (small) interest. The interest on the third pillar is generally higher than the interest on your savings account. But today, it is ridiculously low.

More interestingly, you can also deposit this money in Third Pillar funds. For instance, my previous bank (PostFinance) has three different retirement funds. One with 25% stocks, one with 45% stocks, and one with 75% stocks.

Since you are investing this money for the long term, it is better to invest it in stocks rather than let it grow very slowly with current interest rates.

Normally, you will withdraw the money at retirement age. But, you can also withdraw the money at most five years before retirement age. And if you continue working, you can also withdraw at most five years after retirement age. You cannot do a partial withdraw. You have to withdraw the entire amount.

How to choose a third pillar account?

Which third pillar account should I choose?

You should pay attention to the following points when you search for a third pillar account:

- Interests. If you are not using a retirement fund, you should worry about the account’s interest rate. Be aware that currently, it is pretty bad. The best interest rate I have found is 0.75%. But most banks offer much lower interest on the third pillar.

- Choice of funds. If you plan to invest in a fund, you should check the funds proposed by the bank. Some banks have a large panel, while some others have a poor choice.

- Allocation to stocks. You do not have a lot of choice in what the retirement fund will be investing in. But you can decide how much investment in stock you want. You can be very high based on the provider you choose. The highest investment in stocks is 99% (with Finpension 3a). Be careful with your asset allocation before you choose your fund.

- Total Expense Ratio (TER). When you are comparing third pillar funds, you should pay attention to the TER of the fund. This is the total amount of fees that you will pay for your money. The TER is removed from your money each year. The fees are generally high on these funds. The lowest fee I know of is 0.44% (with Finpension 3a). Even the lowest fee is still high, in my opinion.

- Diversification. Another critical point is to see how the stocks (and bonds) are invested in the fund. Many of the retirement funds are only investing in Swiss stocks and Swiss bonds. But some of them are more diversified. For instance, Finpension 3a offers one fund with 60% world stocks.

You should do your research well and think about what you want from your third pillar. And do not worry if you already have a third pillar account. You can have as many as you want.

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF*!

*(if you deposit 1000 CHF in the first 12 months)

- Invest 99% in stocks

Unfortunately, there are many bad third pillars in Switzerland. So, it is important to choose the best third pillar account for your needs. Currently, for most people, the best third pillar is Finpension 3a. I have an entire article about choosing the best third pillar for your retirement.

2. The third pillar with an insurance

The other option is to have a third pillar in the form of life insurance.

You will pay a certain monthly amount that will go into your insurance. Once you reach retirement age, you get some money (plus maybe some interest). The minimum amount of money that you will get at the end is guaranteed. But, the interest you will get is not guaranteed. And the returns are not great.

If you cannot pay anymore (if you are disabled, for instance), it is still guaranteed. This is only the case for some stated reasons in your contract. You cannot stop paying simply because you want to. If you die before the contract terms, your spouse will get the guaranteed amount.

If you break the contract or stop paying, you will lose much of the money you invested. The amount your life insurance is worth will increase faster and faster over time. In the first two years, it will not even be worth anything. If you think you may break the contract or stop paying, never contracts life insurance!

Many people will tell you not to use this kind of insurance. And many insurance people will tell you that everyone should have one. So, who tells the truth?

Should I take Life Insurance Third Pillar?

No! For most people, life insurance 3a is a bad idea.

First, you will not get back the entire amount you paid, contrary to a third pillar bank account. However, this amount is guaranteed. If your third pillar in a bank has done poorly because of a bear market, you can end up losing money.

With third pillar insurance, you will get at least the guaranteed amount. The interests will vary, of course. And generally, they are quite optimistic about the interests they are predicting. You should only care about the guaranteed amount. All the rest is a bonus.

On top of that, the returns over time are really bad. You will lose a significant amount of money in the long term.

To know more, you should read my article about life insurance 3a.

How to choose third pillar insurance?

Again, I do not know which life insurance is the best one. Here are some things you should pay attention to when you research life insurance:

- The amount per month: You should pay an amount that you are comfortable with. You will pay for this for many years. This will set the guaranteed amount in the end. I would not recommend more than 300 CHF. You should keep some to invest in a third pillar bank account.

- The guaranteed amount in the end: The most important number is how much you will get in the end. The insurance guy will try to make you look at projections. I would advise you to care mostly about the guaranteed amount. Nobody can predict returns over 30 years or more. You should consider the interests as a bonus.

- The investment of your funds: Each insurance will invest your money differently. They will probably propose you different asset allocation or investing strategies. You should pick the one you are the most comfortable with.

You should do your research well. Do not make any rash decisions.

Third pillar and inheritance

In the case of death, the rules are slightly different, based on which third pillar you have.

For the third pillar in a bank, the shares will be divided according to inheritance law. Generally, this will be divided between your spouse, your children, other dependent persons. If you do not have children or a spouse, this could be divided among your brothers, sisters, and parents.

If you want to change this, you can also write a will. Just be aware that there are strong limits in Switzerland regarding what you can and cannot do with inheritance. For instance, you cannot disinherit your children or your spouse.

For the third pillar insurance, inheritance is based on the policyholder. Generally, you need to indicate on your policy who is the beneficiary. For most people, it will be your spouse.

Once again, inheritance law can play a role here. For instance, under some conditions, your heirs can claim some of this money even if they are not mentioned in the policy.

Optimize your third pillar

There are a few things you can do to use the third pillar in the most optimized way.

First, always try to contribute the maximum each year into your third pillar. If you can! Do not get into a bad financial situation just to max out your third pillar. But the best advantage of the third pillar is in the tax advantages. So, maximizing it is interesting.

If you have it in a bank account, consider using a retirement fund. You should consider a fund with an asset allocation that you are comfortable with. You should consider how many years you will invest and how much risk you want to take.

Now, a slight twist. When you withdraw your third pillar, you will pay taxes on the amount. This amount is taxed at several levels, and it depends on which canton you are in. For instance, in Geneva, for up to 25’000 CHF, you will pay 250 CHF in taxes (0 CHF for a married couple). For up to 50’000 CHF, you will pay 1’500 CHF (500 CHF for a married couple).

If we take the canton I am living in (Fribourg), it is different. There is a 2% tax on the first 40’000 CHF. Then a 3% tax for the next 40’000 CHF and the tax keeps increasing until it reaches a 6% tax. You may have already seen the problem here. The more money you have, taxes get more expensive, and the more money you will pay. And it is quickly getting worse if you withdraw even more.

You can withdraw your third pillar money up to five years before and five after the official retirement age (if you still work). Thus, you can work around these taxes by having several third pillar accounts and only withdrawing one each year.

For Geneva, you should try to have less than 25’000 CHF on each account before the withdrawal. Below 50’000 CHF, the taxes are still fair. So you may keep your accounts below 50’000 as well. But you should not go higher. For Fribourg, you should stay below 40’000 CHF. You have to check the exact taxes for your current canton.

Now, there are two tricky things with this. First, there is no way to know how much will be on your third pillar account if you have a retirement fund. The returns will depend on the market. If you think your investment will double before retirement, you should stop contributing at 12’500 CHF. The difference between a 24999 and 25001 will result in 1500 CHF of taxes! This is absolutely insane, in my opinion.

Now comes the second tricky issue. Some cantons in Switzerland are considering this as tax evasion! For instance, the canton of Vaud allows you to have three different accounts. My canton (Fribourg) does not currently prevent this. But this may change.

So, you should be careful with this technique. You should check with your canton before you try to do this.

Just to be clear, it is never a problem to have several third pillars. The problem arises when you optimize the withdrawals over several years. Thus, I advise you to create several smaller third pillar accounts. But only spread out the withdrawals over several years if your canton allows it!

If you want to learn more, you can read my article about staggered withdrawals. It also explains how to combine this with your second pillar.

Third pillar and tax at source

It is important to mention that you only get tax advantages with the third pillar if you can declare it. And you can only declare it in a tax declaration.

So, if you are paying tax at source and are not filing a tax declaration, you will have no tax advantages with a third pillar. And in that case, you are likely better off saving in a broker account or robo-advisor.

Withdraw before retirement

You can withdraw money from your third pillar before retirement (early withdrawal).

The rules are the same as for early withdrawal for the second pillar. You can withdraw to buy a house, start your own company or leave Switzerland.

There is another case when you can withdraw money from the third pillar. In fact, you can withdraw money from the third pillar to contribute to your second pillar. I am not sure there is a lot of value in doing that. You will not be able to deduct this contribution to the second pillar from your taxes, so that you will not be able to deduct it twice. And generally, the conditions of the third pillar are better than the second pillar. If you use a third pillar invested in stocks, it is better than a second pillar.

Accounting for the Third Pillar

Accounting for the third pillar in your net worth is fairly easy. For a third pillar in a bank, you can simply account for it like all your other accounts. It is money you own. It is just locked until retirement age.

For a life insurance third pillar, it is a bit more complicated. Your insurance should give you a guaranteed amount year by year. Using this, you can extrapolate the monthly values to see how much you currently have. You can have a look at how I accounted for my life insurance in my net worth.

Pillar 3b

Pillar 3b is a bit more obscure and is less known. There are many significant differences between 3b and 3a. Pillar 3b is often misunderstood.

Pillar 3b means anything outside of the three pillars. So, a bank or broker account is part of the 3b. And in most cases, there are no tax advantages.

Indeed, only two cantons have tax advantages. For instance, my canton (Fribourg) allows a married couple to deduct up to 1500 CHF yearly. Geneva is even better. You can deduct up to 2200 CHF per year. And based on your number of children, you may even be able to deduct more.

However, these tax advantages are only for 3b life insurance. And these products are generally so bad that they are undesirable for anybody. Insurance companies heavily advertise them, but they only profit from them, not you.

However, life insurance linked to a third pillar is a bad investment. It is not worth the tax advantages, so I would recommend against it.

FAQ

What is the third pillar in Switzerland?

The third pillar is a private pension system in Switzerland. Every people with a salary in Switzerland can contribute a maximum amount each year. This account is tax-advantaged.

How much will I receive from the third pillar?

How much you will receive is entirely depending on how much you contributed. It will also depend on the returns on your investment you got.

How can I optimize my third pillar?

The first thing you need to do is to contribute the maximum each year. Then, you need to find a third pillar provider with the lowest fees. Finally, you need a third pillar account with a large allocation to stocks (up to your asset allocation). Stocks will increase the returns of your third pillar.

Conclusion

The third pillar is the last part of the retirement system of Switzerland.

It will help you cover what is missing from the first and second pillars. Contrary to the previous two pillars, it is an optional part of the system. It is entirely up to you to invest in it. Since it is tax-advantaged, you should invest in the third pillar.

At retirement age, you will get the capital back and pay some taxes on it. But the amount of taxes will be greatly reduced compared to not investing!

If you have not yet read about the first pillar or the second pillar, I encourage you to do so now. In the next and final article, I summarize Switzerland’s retirement system. I also talk about early retirement in this context.

What do you think about the third pillar? What is your preferred account? Do you have tips to optimize it? Do you have any questions regarding this pillar?

Download this e-book and optimize your finances and save money by using the best financial services available in Switzerland!

Download The FREE e-bookRecommended reading

- More articles about Retire in Switzerland

- More articles about Retirement

- Free by 40 in Switzerland – Book Review

- Second Pillar: All you need to know to retire in Switzerland

- Your retirement benefits after your death

If you have tax at source, i.e. ‘Quellensteuer’, there are no tax advantages as far as I know, and therefore 3a Säule is not worth it for those.

Correct, it’s only useful if you are filling a tax declaration.

Hi – I am not clear on this point. If I have tax at source but I do a tax declaration to deduct pillar investment or medical expenses, why I can get the benefit?

Thank you.

I said that it’s only useful if you are filling out a tax declaration. If you are filling out a tax declaration, then you can deduct them. I don’t think I have said something contrary.

Hi Baptiste,

First of all, thanks a lot for your articles they are a great help to this 25 yr old intent on learning to make her own financial (smart) decisions without having to entrust someone else to do it for me.

As mentioned, I am 25 and have been living and working in CH now for two years. I have been told relentlessly to set up my third pillar but since I am still on a B permit I am hesitant. I know that I can ask for a tax recalculation but also know that this isn’t always for the better.

Is it best for me to start young putting a small amount of money in my 3a or is it not much worth it until I am on C permit (in 3 years) and should look for alternative places to put my money? I have no investing experience, but am happy to look further into it.

Thanks!

Hi Kathryn,

I am glad this is useful!

If you are below the 120K CHF income threshold for automatic tax deduction, I would recommend you invest in a broker account or robo-advisor. Once you are forced to do a tax declaration, you can start contributing to a 3a (no life insurance 3a!). That’s the safest general strategy.